Microchip Technology Live: Complete Coverage Of MCHP’s Q3 Earnings

Quick Read

-

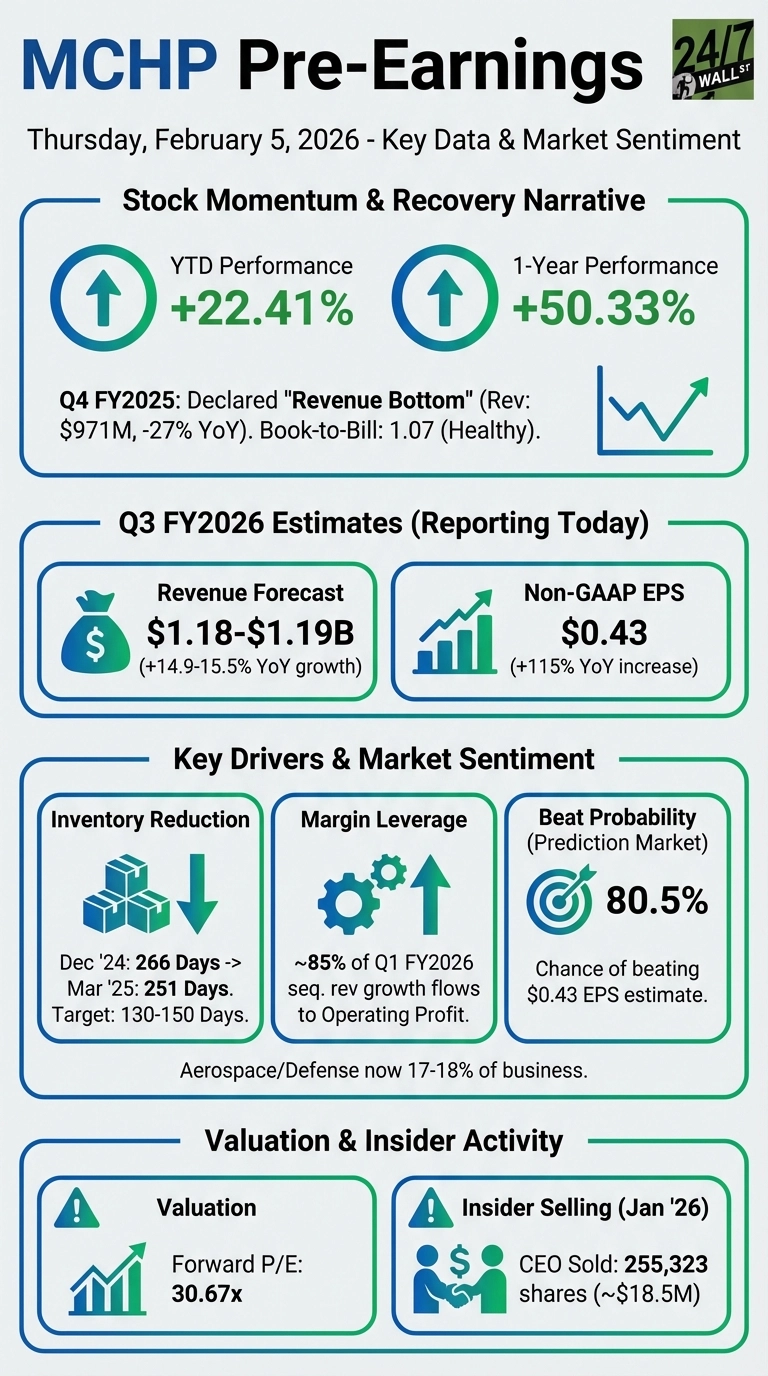

Microchip Technology (MCHP) declared March quarter a revenue bottom after three years of declining sales. Shares surged 50% over the past year.

-

Microchip projects 85% of sequential revenue growth will flow to operating profit as the company exits its inventory correction.

-

Book-to-bill ratio hit 1.07 in March. September backlog runs higher than June did at the same point.

Live Updates

Final Reaction

Microchip did exactly what it needed to do — and nothing more.

-

Results confirmed the recovery

-

Margins expanded as expected

-

Guidance pointed to continued improvement

-

No negative surprises, but no upside shock

With the stock already pricing in a normalization cycle, this quarter serves as validation, not re-rating fuel. Investors will likely need either:

-

faster-than-expected margin expansion toward 65%, or

-

a sharper demand inflection

Margins Are the Real Story

-

Non-GAAP gross margin expanded to 60.5%

-

Up sharply from ~52% in March 2025

-

Long-term target remains ~65%

Margin improvement continues to be driven by inventory normalization and better factory utilization. However, this trajectory was already well telegraphed, limiting incremental upside for the stock.

Management Commentary

CEO Steve Sanghi emphasized execution and recovery momentum:

“Our fiscal third quarter results exceeded our expectations… We believe the broad-based recovery across our end markets, combined with significant margin expansion, demonstrates the tangible impact of our nine-point recovery plan.”

The tone was confident but measured — focused on steady normalization rather than acceleration.

Guidance Update

March 2026 Quarter Outlook

-

Revenue midpoint: $1.260B

-

+6.2% sequential

-

+29.8% year over year

-

-

Non-GAAP EPS: $0.48–$0.52

-

Gross margin outlook: 60.5%–61.5%

Guidance was constructive but expected, reinforcing the recovery narrative without introducing upside surprise. Management reiterated confidence in sequential growth and further margin expansion as utilization improves.

Earnings Are In

Microchip delivered a clean execution quarter, beating EPS expectations on both a GAAP and non-GAAP basis while landing revenue essentially right on the company’s updated guide. Results confirmed that the business is recovering — but did not materially exceed what investors were already positioned for.

| Metric | Actual | Company Guide | Result |

|---|---|---|---|

| Revenue | $1.186B | ~$1.185B | 🟢 In Line / Slight Beat |

| EPS (GAAP) | $0.06 | $0.02 | 🟢 Beat |

| EPS (Non-GAAP) | $0.44 | $0.40 | 🟢 Beat |

Key Takeaways From Last Quarter

- Revenue grew 6% sequentially to $1.14B with improving margins—non-GAAP gross margin reached 56.7% despite $122.8M in underutilization and inventory charges. Product gross margin remains healthy at 67.4%, with data center business showing recovery as customer inventory corrections complete.

- Announced industry-first 3-nanometer PCIe Gen 6 switch for AI infrastructure, sampling to hyperscalers now with production expected June 2026. Device offers 15-20% power advantage over competitors, with TAM exceeding $2B annually growing 10%+ through 2035.

- Inventory decreased $73.8M to 199 days (down from 266 days) with plans to continue factory ramp-up. Guiding December quarter down 1% (better than typical seasonal -3% to -5%), expecting strong recovery in following three quarters as customer inventories normalize and backlog strengthens.

Microchip Technology (NASDAQ: MCHP | MCHP Price Prediction) reports earnings today after the bell, testing whether management’s recovery narrative can translate into sustained momentum. Shares have surged 50% over the past year and 22% year to date, pricing in optimism that the semiconductor supplier’s inventory correction is ending.

What Changed Last Quarter

Management declared the March quarter a revenue bottom, the first such call after nearly three years of declining sales. Revenue came in at $971 million, down 27% year over year but with encouraging demand signals. The book-to-bill ratio reached 1.07, the first healthy reading in years, and CEO Steve Sanghi noted April bookings exceeded any month in the March quarter.

The company reduced inventory to 251 days from 266 days in December. Management expects to liberate over $350 million from inventory this fiscal year, targeting 130 to 150 days long term. June quarter guidance of $1.045 billion in revenue represented a $74.5 million sequential increase, with 85% of that flowing to operating profit.

Consensus Estimates

| Metric | Q3 FY2026 |

|---|---|

| Revenue | $1.18-$1.19B |

| Non-GAAP EPS | $0.43 |

| YoY Growth | 14.9-15.5% revenue, 115% EPS |

All Eyes on Margin Recovery and Backlog Strength

Watch whether management can deliver on the margin leverage story. Last quarter’s gross margin of 52% included $54.2 million in underutilization charges, and CFO Eric Bjornholt said those costs would remain elevated this quarter. The key question is whether revenue growth can offset these headwinds enough to show meaningful operating profit expansion.

Look at the September quarter guidance. Sanghi said September backlog is higher than where June was at the same point, suggesting momentum is building. The company’s prediction market shows traders pricing in an 80.5% probability of beating the $0.43 EPS estimate, reflecting strong conviction in the recovery narrative.

Aerospace and defense strength should continue, with that segment now representing 17-18% of business, up from 11% a year ago. Broader industrial and automotive markets are showing signs of life after extended inventory corrections.

Why This Quarter Matters

If Microchip can confirm the recovery is accelerating and provide confident September guidance, the stock’s recent run could have further to go. But with shares trading at 30x forward earnings and CEO Sanghi selling 255,000 shares worth $18.5 million in January, execution needs to be flawless to justify current valuation.

Joel South covers large-cap stocks, dividend investing, and major market trends, with a focus on earnings analysis, valuation, and turning complex data into actionable insights for investors.

He brings more than 15 years of experience as an investor and financial journalist, including 12 years at The Motley Fool, where he served as an investment analyst, Bureau Chief, and later led the Fool.com investing news desk. He has also co-hosted an investing podcast and appeared across TV and radio discussing market trends.

© 24/7 Wall St.