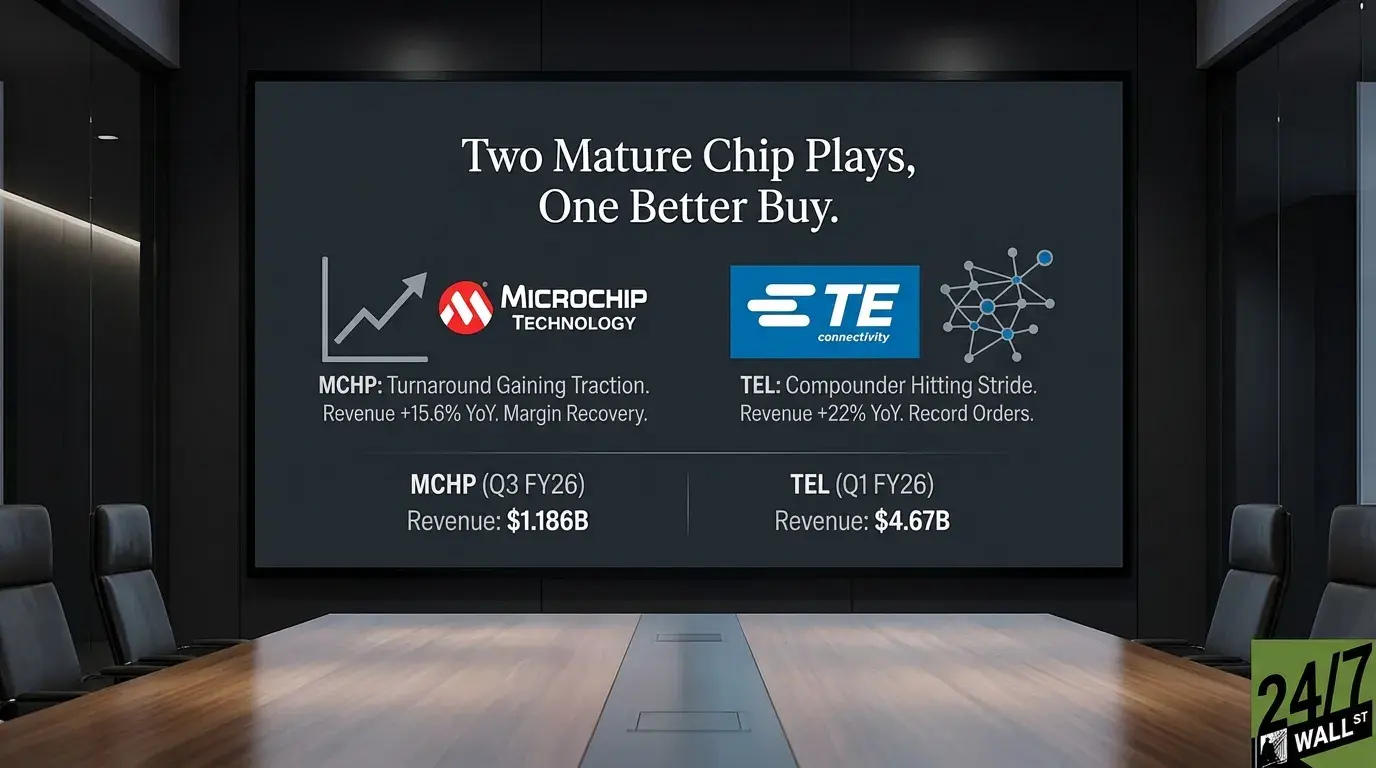

Microchip Technology (NASDAQ:MCHP | MCHP Price Prediction) just posted a third consecutive quarter of sequential revenue recovery, while TE Connectivity (NYSE:TEL) delivered record orders and double-digit growth across both segments. Two mature industrial-facing names, two very different stories.

A Turnaround Gaining Traction vs. a Compounder Hitting Its Stride

Microchip’s recovery is accelerating. Revenue came in at $1.186 billion, up 4% sequentially and 15.6% year over year. Non-GAAP gross margins expanded to 60.5%, up from 52% just a year ago. CEO Steve Sanghi has been methodical: close underperforming fabs, normalize inventory, rebuild customer relationships. The nine-point recovery plan is producing visible results.

TE Connectivity is operating in a different gear. Q1 FY2026 revenue hit $4.67 billion, up 22% year over year, with record orders of $5.1 billion, up 28%. The Industrial Solutions segment grew 38% year over year, fueled by AI data center connectivity and grid hardening. CEO Terrence Curtin put it directly: “Our teams delivered strongly against our strategy, resulting in first quarter earnings growth over 30% and sales growth of more than 20%, both of which were above our guidance.”

| Metric | MCHP (Q3 FY26) | TEL (Q1 FY26) |

|---|---|---|

| Revenue | $1.186B | $4.67B |

| YoY Revenue Growth | +15.6% | +22% |

| Adj. Operating Margin | 28.5% | 22.2% |

| Free Cash Flow | $318.9M | $608M |

| Forward P/E | 24x | 18x |

Microcontrollers vs. Connectors: The Secular Bets Underneath

Microchip sells microcontrollers and analog chips into roughly 120,000 customers across industrial, automotive, and aerospace markets. Its moat is breadth and deep customer integration. The risk: inventory normalization still has room to run, and macro softness could slow the recovery.

TE makes the connectors, cables, and sensors that move power and data through machines, vehicles, and data centers. Its AI data center revenue tripled from $300 million in FY2024 to over $900 million in FY2025. Hyperscaler capex is expected to grow roughly 20% in FY2026, and TE has design wins in place to capture that spend.

The Next Test Is Margin Durability

For Microchip, the question is whether gross margins can keep climbing toward 65% long-term target as factory utilization improves. Guidance for the March quarter calls for net sales of $1.260 billion at the midpoint, representing nearly 30% year-over-year growth. Tariffs and macro softness remain key variables.

For TE, the watch item is whether the Transportation segment stabilizes in Western markets while the AI-driven Industrial segment holds momentum. Analyst consensus sits at target price of $275 against a current price of $199.41, suggesting meaningful upside if execution holds.

Comparing the Two Profiles

Microchip is a legitimate turnaround, and Sanghi has earned credibility executing his plan. MCHP at a forward P/E of roughly 24x with a 2.9% dividend yield. The stock is down about 23% over the past month, representing a significant pullback from recent highs.

But TE is already in growth mode, not recovery mode. It is capturing AI infrastructure spend today, growing content per vehicle independent of EV adoption rates, and generating over $600 million in quarterly free cash flow. At a forward P/E closer to 18x, the valuation reflects a business with more near-term earnings visibility. Analysts tracking AI infrastructure exposure may find TE’s near-term earnings visibility worth examining alongside Microchip’s ongoing margin recovery story.