Strategy Live: Complete Coverage Of MSTR’s Q4 Earnings

Quick Read

-

MicroStrategy (MSTR) stock crashed 67% over the past year as Bitcoin dropped 17% to $72,725.

-

MicroStrategy holds 640,808 Bitcoin below its $74,032 cost basis with $24.3B in implied unrealized losses.

-

Multiple class action lawsuits allege MicroStrategy overstated Bitcoin strategy profitability and understated volatility risks.

Live Updates

What You Need to Know About Strategy Earnings

This quarter perfectly captures the MSTR paradox:

-

GAAP results look catastrophic

-

Bitcoin strategy remains intact

-

Capital access remains wide open

For investors, the takeaway is simple:

MSTR is not an earnings stock. It is a levered bitcoin vehicle with an increasingly sophisticated capital structure.

As long as bitcoin remains volatile, reported losses will dominate headlines. As long as capital markets remain open, Strategy will keep buying BTC — and that, not EPS, is what ultimately drives the stock.

Why the Loss Looks So Bad (But Isn’t Operational)

-

$17.4B unrealized digital asset loss recorded in Q4

-

Caused by bitcoin price decline near quarter-end

-

This is non-cash and reversible if BTC prices recover

Importantly, these losses say nothing about liquidity or solvency — they are purely accounting artifacts under the new fair-value regime.

Bitcoin Holdings Continue to Expand Aggressively

-

713,502 BTC held as of Feb. 1, 2026

-

Average cost: $76,052 per BTC

-

Market value: ~$59.8B

-

BTC Yield: 22.8% for FY2025 (within target range)

Despite the headline loss, Strategy added more than 225,000 BTC during 2025, reinforcing its position as the dominant corporate bitcoin holder.

Management Commentary

EO Phong Le framed 2025 as a capital-formation milestone:

“We raised $25.3 billion of capital in 2025 to advance our Bitcoin treasury strategy… Our capital structure is stronger and more resilient today than ever before.”

Executive Chairman Michael Saylor emphasized the long-term vision:

“Strategy has built a digital fortress anchored by 713,502 bitcoins… aligned with our indefinite bitcoin horizon.”

The tone was unapologetically long-term and dismissive of short-term earnings optics.

Guidance & Outlook

Strategy does not provide traditional revenue or EPS guidance, instead emphasizing bitcoin-centric KPIs:

-

BTC Yield target framework remains intact

-

Continued focus on Bitcoin Per Share (BPS) accretion

-

Ongoing expansion of Digital Credit (preferred equity) instruments

Management reiterated its intention to grow bitcoin exposure per share over time, regardless of short-term GAAP volatility.

After Brutal Day For MSTR, Earnings Are In

| Metric | Actual | Street Expectation | Result |

|---|---|---|---|

| Revenue | $123.0M | ~$125M | 🔴 Miss |

| EPS (GAAP, Diluted) | –$42.93 | ~–$21.00 | 🔴 Miss |

| Operating Income | –$17.4B | N/A | 🔴 Large Loss |

trategy reported a massive GAAP loss, driven almost entirely by unrealized bitcoin fair-value losses, obscuring otherwise stable operating performance and continued bitcoin accumulation. This was the fourth quarter under fair-value accounting, making reported earnings extremely sensitive to quarter-end BTC prices.

Key Takeaways From Last Quarter

- Now holds 640,808 Bitcoin ($71B value, 3.1% of total supply) after raising $19.8B capital YTD, shifting strategy from convertible debt (10% of raises) to preferred equity (30%) which offers permanent capital without refinancing risk. Achieved 26% BTC yield YTD toward 30% target.

- Launched four preferred securities (STRF, STRK, STRD, STRC) providing 10-16% tax-deferred “ROC dividend” yields versus 4% money markets—expecting this tax treatment to continue 10+ years. Received first-ever S&P credit rating (B-) for Bitcoin treasury company, opening access to $8.4T rated credit market.

- Emphasizing “digital credit” model with 7 innovations over traditional credit: Bitcoin-backed (appreciating vs depreciating collateral), transparent/continuous risk monitoring, perpetual preferred equity (no refinance risk), public/liquid instruments, and tax-deferred dividends. Planning international expansion with native currency instruments in Canada, Europe, Asia to access broader capital pools.

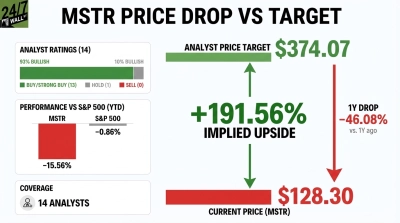

Strategy Inc (NASDAQ: MSTR | MSTR Price Prediction) reports fourth-quarter 2025 results on February 3, 2026, with investors bracing for the company’s first earnings call since Bitcoin plunged and the stock shed 67% over the past year. The company’s unconventional Bitcoin treasury strategy faces its toughest test yet.

Bitcoin Volatility Drives Stock Collapse

MSTR shares have crashed 27.5% year-to-date and 30% over the past month. The culprit: Bitcoin’s decline from $87,498 on January 1 to $72,725 on February 5, a 17% drop that hammered the company’s 640,808 BTC holdings valued at $70.9 billion.

The stock now trades at $110.11, far below its 52-week high of $457.22. Multiple class action lawsuits allege the company overstated the profitability of its Bitcoin strategy and understated volatility risks, adding legal pressure to market headwinds.

Consensus Estimates

| Metric | Q4 2025 Est. |

|---|---|

| EPS | -$20.99 |

| Revenue | $ 118.47M |

Analysts expect negative earnings, a sharp reversal from Q3’s $8.42 EPS that missed estimates.

Mark-to-Market Accounting Creates Extreme Volatility

I’ll be watching how management frames the impact of fair value accounting adopted in 2025. Last quarter’s guidance projected net income ranging from -$5.5 billion to +$6.3 billion depending on Bitcoin prices between $85,000 and $110,000. With Bitcoin now at $72,725, expect substantial unrealized losses.

Reddit sentiment has turned very bearish, with retail investors fixated on liquidation thresholds. One popular thread warned Saylor is “3% away from negative Bitcoin position” based on the company’s $74,032 per BTC cost basis.

Capital Structure Under Scrutiny

The company established a $1.44 billion USD reserve to cover dividend payments and debt interest without selling Bitcoin. Management continues aggressive accumulation, acquiring 855 BTC for $75.3 million as recently as February 2. Investors will be watching whether this strategy remains credible given the stock now trades at 0.74x book value.

This Quarter Decides Strategy Viability

After two quarters of extreme earnings misses and mounting legal challenges, management needs to prove the Bitcoin treasury model works during crypto downturns. If guidance suggests forced liquidations or capital raises at depressed prices, institutional holders may reassess their positions.

Joel South covers large-cap stocks, dividend investing, and major market trends, with a focus on earnings analysis, valuation, and turning complex data into actionable insights for investors.

He brings more than 15 years of experience as an investor and financial journalist, including 12 years at The Motley Fool, where he served as an investment analyst, Bureau Chief, and later led the Fool.com investing news desk. He has also co-hosted an investing podcast and appeared across TV and radio discussing market trends.

© 24/7 Wall St.