After Strategy Inc. (NASDAQ:MSTR | MSTR Price Prediction) (formerly MicroStrategy) stock cratered 18.4% in the past week and sat 62.5% below where it traded a year ago, the stock saw a sharp reversal on Friday. At $125.75, is this still a buying opportunity, or is it a value trap?

The Bitcoin Accounting Nightmare

After adopting fair value accounting for crypto assets in Q1 2025, MSTR reported a $17.44 billion unrealized loss on digital assets in Q4 2025. This drove EPS to negative $42.93, versus expectations of positive $2.97.

This is an accounting artifact, not an operational failure. MSTR holds 713,502 bitcoins with a cost basis of $76,052 per coin. Bitcoin currently trades at approximately $83,800, meaning the company holds an unrealized gain of roughly 10% above its cost basis. But CEO Phong Le continues to accumulate. He said:

We raised $25.3 billion of capital in 2025 to advance our Bitcoin treasury strategy […] We increased our holdings to 713,502 bitcoins, including 41,002 bitcoins acquired in January 2026 alone.

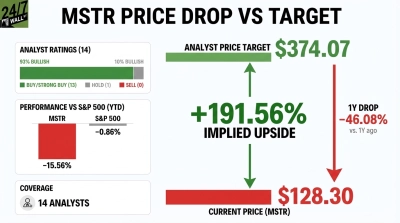

The Bull Case: Analysts Still Believe

Thirteen of fourteen analysts rate MSTR as Buy or Strong Buy, with an average price target of $452, or 270% upside from current levels. The stock trades at a trailing P/E of just 5.3 with 25.6% return on equity.

The RSI hit 24.27 on February 5, deep into oversold territory. MSTR historically bounces from these levels within 10 to 15 trading days. Insiders are buying: CEO Le purchased preferred shares on January 8, while director Carl Rickertsen bought 5,000 common shares at $155.88 on January 12.

If Bitcoin recovers to $100,000 or higher, MSTR offers leveraged exposure without self-custody hassles. The company’s $2.30 billion cash position and $2.25 billion USD reserve cover dividends and interest for years without forced Bitcoin sales.

The Bear Case: This Could Get Worse

Bitcoin’s recent volatility remains a concern. While the company currently holds an unrealized gain on its Bitcoin position, prediction markets show only a 15.5% probability Bitcoin reaches $85,000 this month. If Bitcoin falls below the company’s $76,052 cost basis, MSTR’s unrealized losses would compound rapidly.

The stock’s beta of 3.5 amplifies every Bitcoin move. MSTR raised $25.3 billion last year by issuing shares, diluting existing shareholders, and plans to continue this strategy indefinitely.

EVP Wei-Ming Shao sold over 20,000 shares at $200 to $250 in November 2025, just before the collapse.

The Verdict

MSTR represents a leveraged Bitcoin bet wrapped in a software company. The stock’s performance will largely depend on Bitcoin’s trajectory. With analyst price targets averaging $452 (270% above current levels) but Bitcoin prediction markets showing only 15.5% probability of reaching $85,000 this month, the stock faces significant uncertainty. The company’s 3.5 beta means it amplifies Bitcoin moves threefold in both directions. Those considering the stock should evaluate their Bitcoin outlook and risk tolerance accordingly.