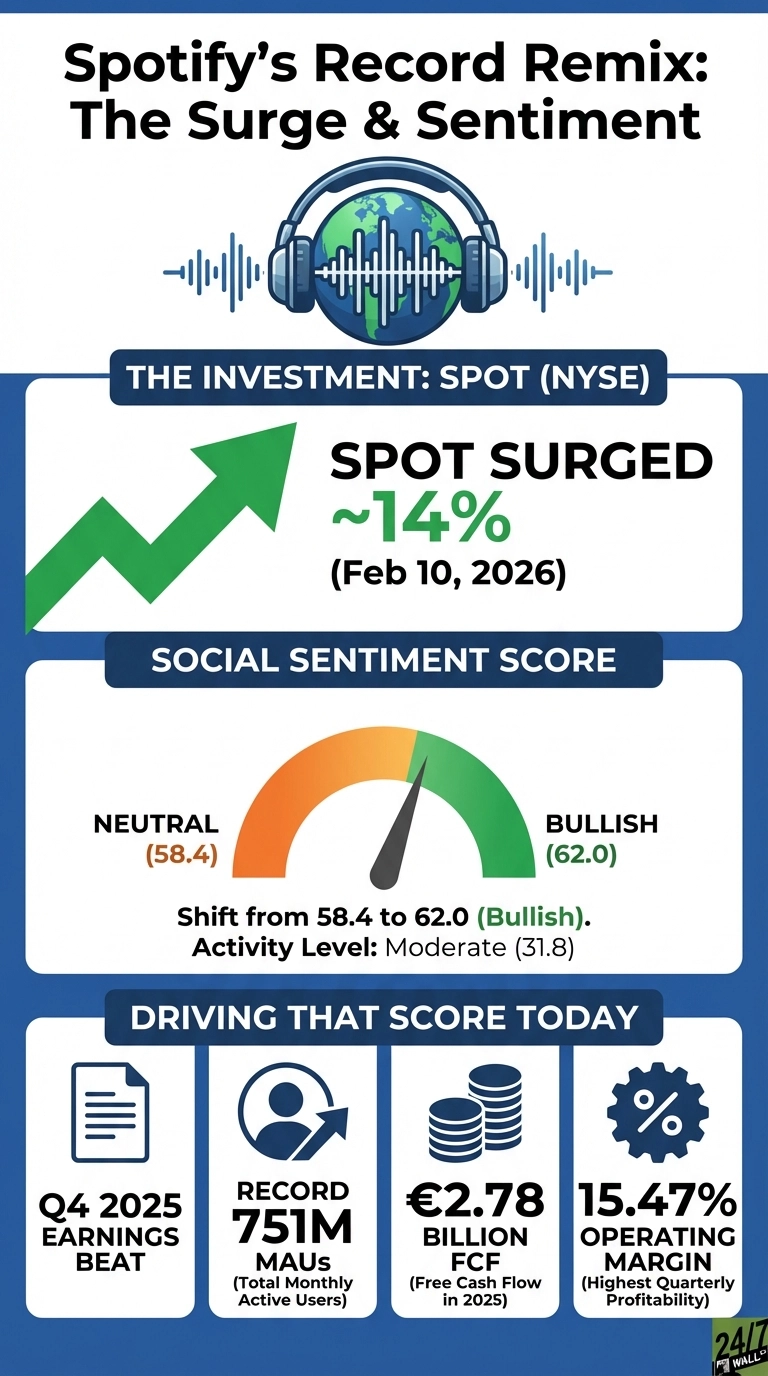

Spotify Technology (NYSE:SPOT | SPOT Price Prediction) surged 14% after delivering Q4 2025 earnings that validated its transformation from cash-burning disruptor to profitable streaming giant, as investors rewarded the company’s ability to expand margins while growing users, a combination that eluded the platform for years as it battled music licensing costs and competition from Apple and Amazon. Even skeptical Reddit traders shifted sentiment from 58.4 to 62.0 as the company demonstrated it can grow users while expanding margins.

Spotify crushed earnings expectations by 60% with $5.16 in earnings per share versus $3.21 expected, but the real story is how it added 38 million monthly active users in Q4 while expanding operating margins to record levels, solving the puzzle that plagued streaming economics for years, as it turns out, you can grow the audience AND make money at the same time. The platform now reaches 751 million total monthly active users, with 290 million premium subscribers, while operating income reached €701 million (~$835 million) and the margin was 15.47%, the highest quarterly profitability in company history.

Reddit Traders Flip From Skeptics to Believers

Discussion volume on Reddit jumped from low (20.5) to moderate (31.8) during the earnings window. The most engaged post on r/wallstreetbets accumulated 5,742 upvotes and 802 comments.

The final bell

by [USERNAME] in wallstreetbets

Three developments support the bullish case:

- Free cash flow exploded from €21 million in 2022 to €2.9 billion in 2025 as Spotify cracked the code on streaming economics – negotiating better licensing deals while algorithmic personalization kept users engaged without proportional cost increases

- The company paid $11 billion to music rights holders in 2025, demonstrating sustainable economics that keep labels at the negotiating table

- Management’s €422 million share buyback program in 2025 signals confidence in sustainable profitability, a stark contrast to years of capital raises when the company burned cash to build market share

From Losses to Margins: The Numbers Behind the Narrative

The margin expansion story reveals why Wall Street is reassessing Spotify’s competitive position. Operating margin expanded from -3% in 2023 to 12% in 2025, a massive swing of over 1,600 basis points in two years that proves the company can negotiate better licensing terms as it scales. Gross margin reached 31%, up from 11% a decade ago, as the company gained leverage in licensing negotiations and operational efficiency – a structural advantage that compounds as the user base grows.

Goldman Sachs upgraded Spotify to Buy with a $700 price target, citing pricing power and AI-driven personalization as durable advantages. The consensus of 27 analysts is $735.74, implying 57% upside despite the recent surge.

What Investors Should Watch Next

Spotify’s co-CEOs framed 2026 as “the year of raising ambition”, with AI features like Prompted Playlists and expanding audiobooks as growth levers. The company’s ability to sustain 12.9% profit margins while investing in product innovation will determine whether this rally extends. Sentiment on r/wallstreetbets turned bearish again by February 16, suggesting profit-taking after the post-earnings euphoria.

Data Sources

- Screenshot 2026-02-17 at 12.01.36 PM: Used to confirm analyst consensus price targets ($735.74 average across 27 analysts) and validate the 56.88% upside potential cited in the article’s forward-looking section.