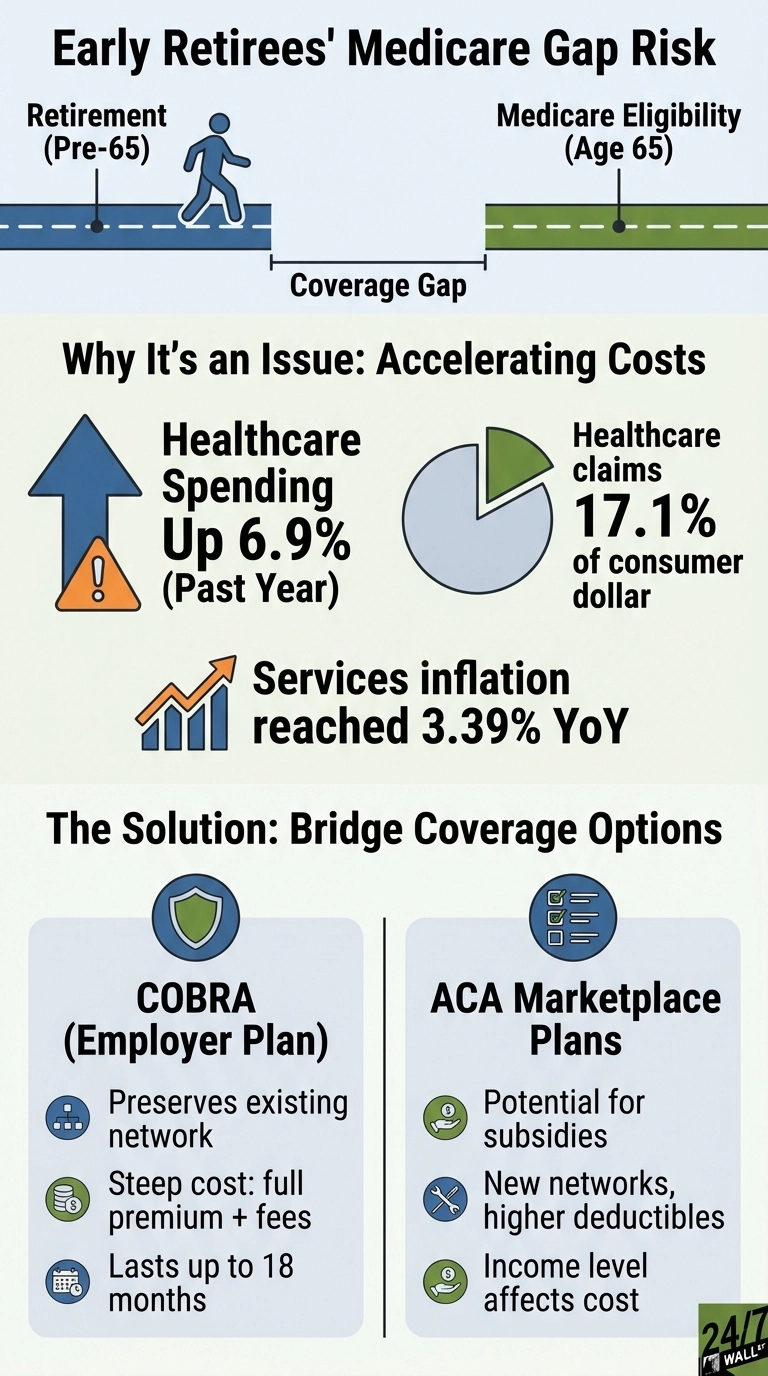

Retiring before age 65 means losing employer health coverage before you qualify for Medicare. That gap creates one of the biggest financial risks in early retirement. Healthcare costs have accelerated sharply in recent months, creating a more expensive environment for early retirees. Medical services are outpacing general inflation, with overall healthcare spending up 6.9% over the past year. This acceleration means healthcare now claims 17.1% of every consumer dollar—a growing burden that makes the coverage gap between retirement and Medicare eligibility increasingly costly to bridge.

Medicare eligibility begins at age 65, but employer coverage typically ends the day you retire. If you leave work at 62, you face three years without your workplace plan. Understanding your bridge coverage options makes the difference between a secure transition and a financial crisis.

The Two Main Bridge Options

Most early retirees choose between COBRA continuation coverage and Affordable Care Act marketplace plans. COBRA preserves your existing employer plan for up to 18 months after leaving, but at a steep cost—you’ll pay the full premium your employer previously subsidized, plus administrative fees. This typically means several hundred dollars monthly for individual coverage, making it one of the most expensive bridge options despite its continuity benefits.

ACA marketplace plans offer an alternative, especially if your retirement income qualifies you for subsidies. Both COBRA and marketplace plans face cost pressures from broader inflation trends. Services inflation reached 3.39% year-over-year through November 2025, pushing premiums higher across all coverage types. This makes ACA marketplace subsidies increasingly valuable for eligible enrollees, as tax credits can offset rising costs based on your retirement income level.

What Matters Most in Your Decision

The key factor is whether continuity of care outweighs cost savings. COBRA preserves your existing network and coverage terms, which matters if you have ongoing treatments or prefer your current doctors. Marketplace plans may cost less with subsidies but require new networks and potentially higher deductibles.

Your retirement income level fundamentally shapes marketplace affordability through the subsidy structure. Tax credits phase out as income rises, and the calculation captures all sources—wages, investment returns, retirement account withdrawals, and Social Security benefits. Strategic income planning becomes essential for early retirees, as higher-income couples may face substantial yearly premiums without enhanced tax credits to offset the cost burden.

Planning for the Full Gap

Since COBRA only lasts 18 months, retiring more than a year and a half before 65 means you’ll eventually need marketplace coverage. Some retirees use COBRA initially while researching marketplace options, then switch during the next open enrollment. Others go straight to marketplace plans to avoid paying COBRA’s full costs.

Medicare enrollment begins three months before your 65th birthday month and extends three months after, creating a seven-month window. This timing exists because Medicare needs processing time to activate coverage by your birthday month. Missing this window triggers late enrollment penalties that compound monthly and last as long as you have coverage, potentially adding thousands to lifetime Medicare costs.

Making the Choice Work

Calculate your total healthcare costs under both scenarios, including premiums, deductibles, and out-of-pocket maximums. Factor in prescription drug coverage, which may differ significantly between your employer plan and marketplace options. Consider whether you can time retirement to minimize the coverage gap or whether working part-time might maintain employer benefits longer.

The hardest mistake to undo is letting coverage lapse entirely. Pre-existing conditions complicate future enrollment, and unexpected medical events during a gap period can devastate retirement savings. Bridge coverage protects the retirement you’ve built while you wait for Medicare eligibility.