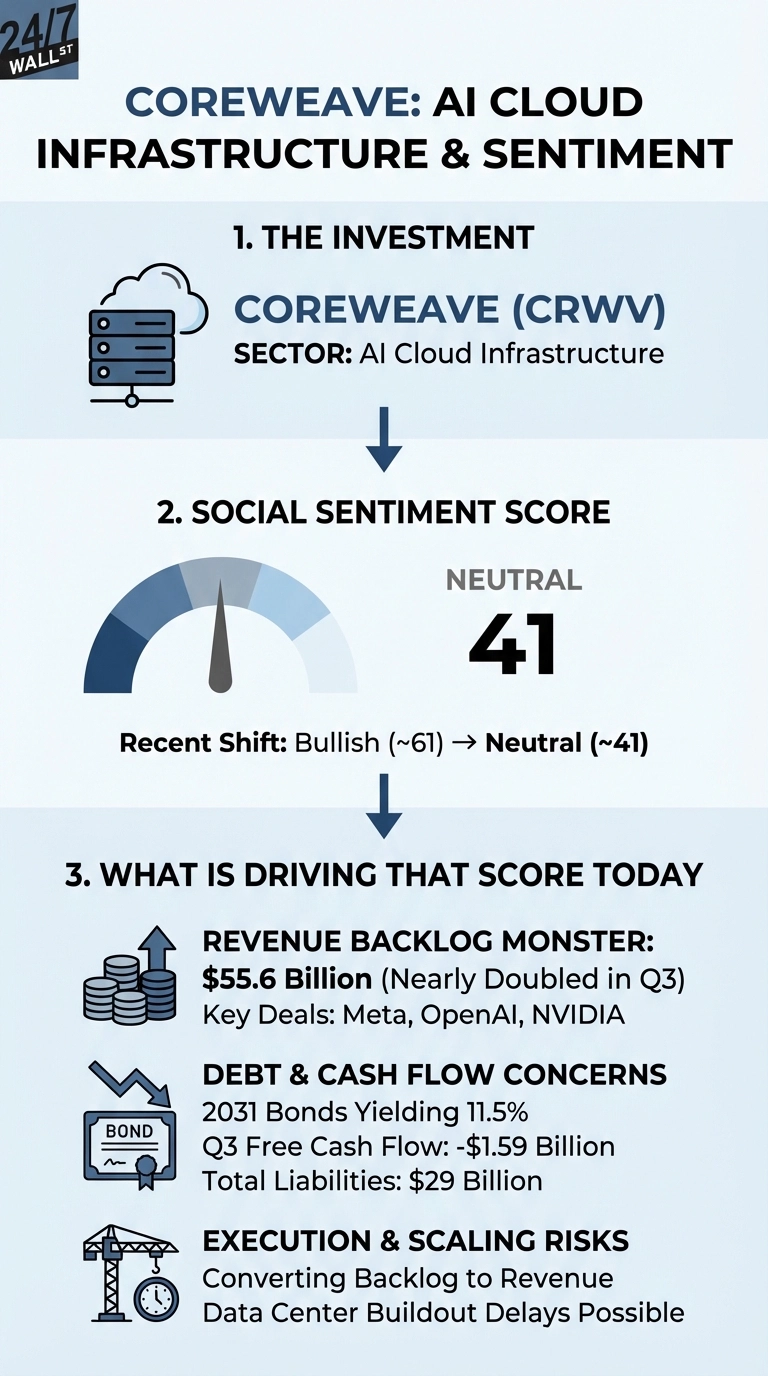

A now-staple name in the AI world, CoreWeave (NASDAQ:CRWV) is sitting on a massive $55.6 billion revenue backlog, nearly double what it had just one quarter earlier. This figure alone makes it one of the most talked-about AI infrastructure plays among retail investors. But the conversation on Reddit has shifted from excitement to caution over the past month, with sentiment cooling from bullish (~61) to neutral (~41) as traders weigh the company’s execution risks against its massive growth potential.

The result is that Reddit sentiment for CRWV has shifted notably, dropping from approximately 61 (bullish) to 41 (neutral) over the past month.

Shares are trading at $95.45, up 33% year-to-date but down 5.7% over the past month, which is worth noting. Analysts maintain a consensus price target of $126, implying roughly 30% upside, with 18 of 30 analysts rating the stock a Buy or Strong Buy. The bull case is straightforward: CoreWeave added over $25 billion in revenue backlog in Q3 alone, driven by expanded deals with Meta ($14.2 billion), OpenAI ($22.4 billion total), and NVIDIA ($6.3 billion).

Reddit Turns Cautious on Debt and Execution

Recent discussions on r/StockMarket reflect growing skepticism about whether CoreWeave can deliver on its promises. One post on r/StockMarket titled “Coreweave 2031 bonds paying 11.5%” highlighting the company’s 2031 bonds paying 11.5% drew significant attention, with 114 upvotes and 44 comments. The post prompted readers to consider what a high-yield bond rate signals about the market’s confidence in CoreWeave’s ability to service its debt load.

Coreweave 2031 bonds paying 11.5%

by u/StockMarket_OP in StockMarket

High-yield debt at that level indicates that the market is pricing in material risk, despite the company’s explosive revenue growth of 134% year-over-year in Q3.

The concerns boil down to three issues:

- CoreWeave burned $1.59 billion in free cash flow in Q3 as it races to build out data center capacity

- The company carries $29 billion in total liabilities against just $3.9 billion in equity

- Customer concentration is extreme, with no single customer representing more than 35% of backlog, but Meta and OpenAI still dominate the revenue base

The Path Forward Depends on Execution

CoreWeave’s valuation hinges on whether it can convert backlog into revenue without hitting infrastructure bottlenecks. The company expanded active power capacity to 590 megawatts in Q3 and has 2.9 gigawatts of contracted capacity, but data center buildouts are prone to delays. CEO Michael Intrator acknowledged temporary delays from a third-party provider during the Q3 call, though he emphasized that the affected customer agreed to extend the delivery schedule.

Whether CoreWeave can convert that backlog into revenue on schedule is the only question that matters right now. The 11.5% yield on the company’s 2031 bonds is the market’s honest answer about how confident it is in that outcome.