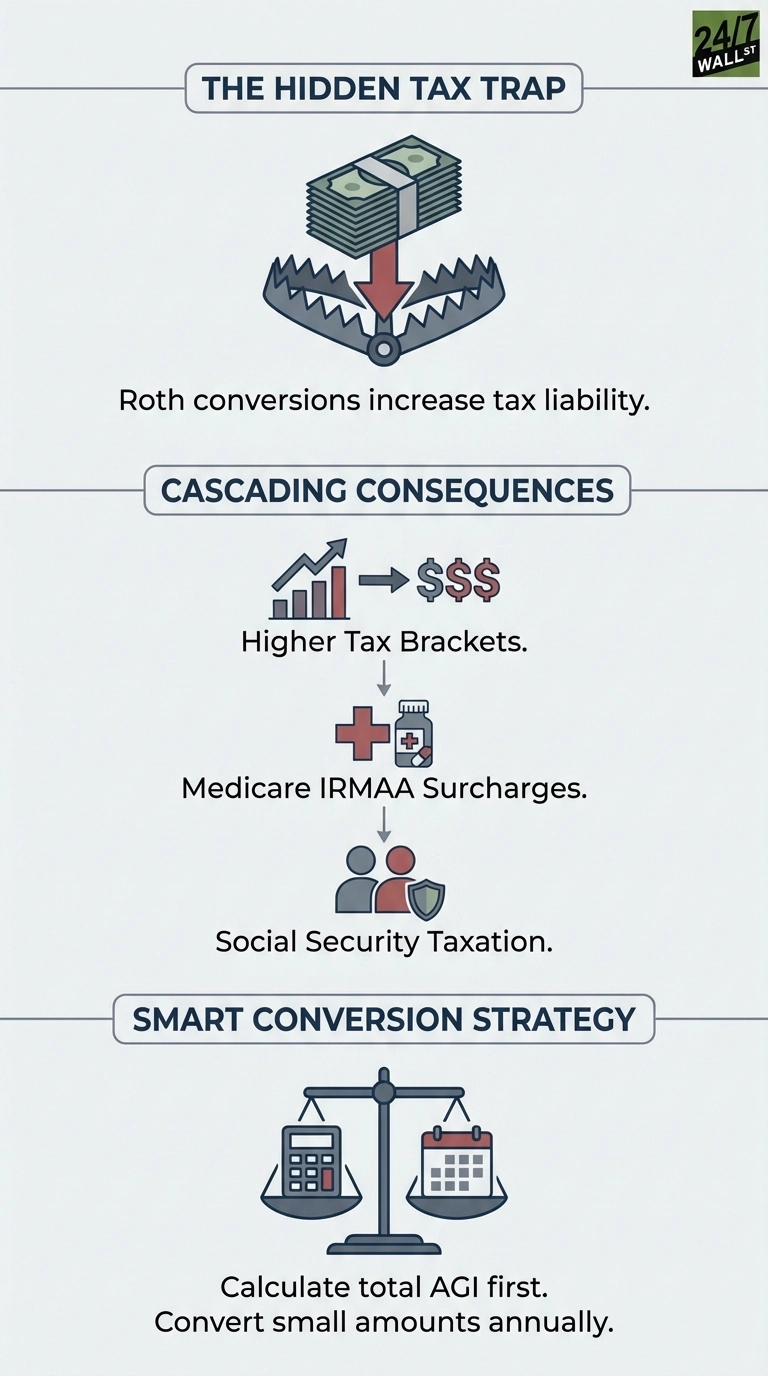

Converting a traditional IRA to a Roth IRA sounds straightforward: pay taxes now, enjoy tax-free growth later. But the conversion creates income that ripples through the tax code in unexpected ways. That converted amount increases your adjusted gross income for the year, potentially triggering higher tax brackets, Medicare surcharges, and taxation of Social Security benefits that would otherwise remain untaxed.

The Hidden Tax Cascade

When you convert funds from a traditional IRA to a Roth, that amount gets added to your adjusted gross income. That higher AGI can push you into a higher marginal tax bracket, reduce or eliminate tax deductions that phase out at certain income levels, and trigger stealth taxes.

A single filer converting a large IRA balance could jump from the 22% bracket into the 24% bracket, effectively paying an extra 2% on tens of thousands of dollars—not just on the converted amount, but on other income that gets pushed into the higher bracket, creating a compounding tax cost that erodes the conversion’s long-term benefit.

Medicare IRMAA: The Two-Year Lookback Trap

For anyone on Medicare or approaching eligibility, Roth conversions carry an additional penalty. Medicare Part B and Part D premiums include Income-Related Monthly Adjustment Amounts (IRMAA) for higher earners. The Social Security Administration determines IRMAA based on your modified adjusted gross income from two years prior.

A conversion affects your Medicare premiums two years later due to the lookback period. Medicare premium surcharges kick in at income thresholds that create cliff effects—where a modest conversion can trigger substantial additional annual healthcare costs that persist for a full year. This makes conversion timing critical for anyone within two years of Medicare eligibility, as the lookback period means today’s conversion affects premiums years later.

The IRMAA surcharge structure creates multiple income cliffs where small conversion amounts can trigger disproportionate premium increases, making it essential to model conversions against these thresholds rather than converting arbitrary amounts.

These thresholds operate on a cliff basis. One dollar over the limit triggers the full surcharge, creating a hidden cost that can erase much of the conversion’s benefit for retirees on fixed incomes.

Social Security Taxation Thresholds

Roth conversions also increase taxation of Social Security benefits. Conversions can push retirees over the income thresholds where Social Security benefits become taxable—transforming what would be tax-free retirement income into taxable dollars. For many retirees, this creates a compounding tax hit where the conversion itself generates tax liability while simultaneously making previously untaxed benefits subject to federal income tax.

Benefits become taxable when provisional income exceeds $25,000 for single filers or $32,000 for married couples filing jointly. Provisional income includes half of your Social Security benefits plus all other income, including Roth conversions. Up to 85% of benefits can become subject to federal tax once your income crosses certain levels—effectively creating a double tax on the same retirement dollars.

What to Evaluate First

Before converting, calculate your total AGI with the conversion included. Check where that lands relative to tax bracket thresholds, IRMAA tiers, and Social Security taxation limits. Converting smaller amounts over multiple years often reduces the total tax cost compared to a single large conversion that crosses multiple thresholds at once. For Medicare enrollees or those within two years of eligibility, IRMAA lookback timing matters as much as the conversion amount itself.