PayPal, the beloved payment system spread across the internet far and wide (NASDAQ:PYPL | PYPL Price Prediction) has seen its shares collapse 45% over the past year to $42.06, erasing nearly half the stock’s value and leaving retail investors asking whether this is a generational buying opportunity or a value trap with no escape route. The answer depends on whether you believe new CEO Alex Chriss’s successor can fix what the previous leadership could not, and there is no question there is a very big “if.”

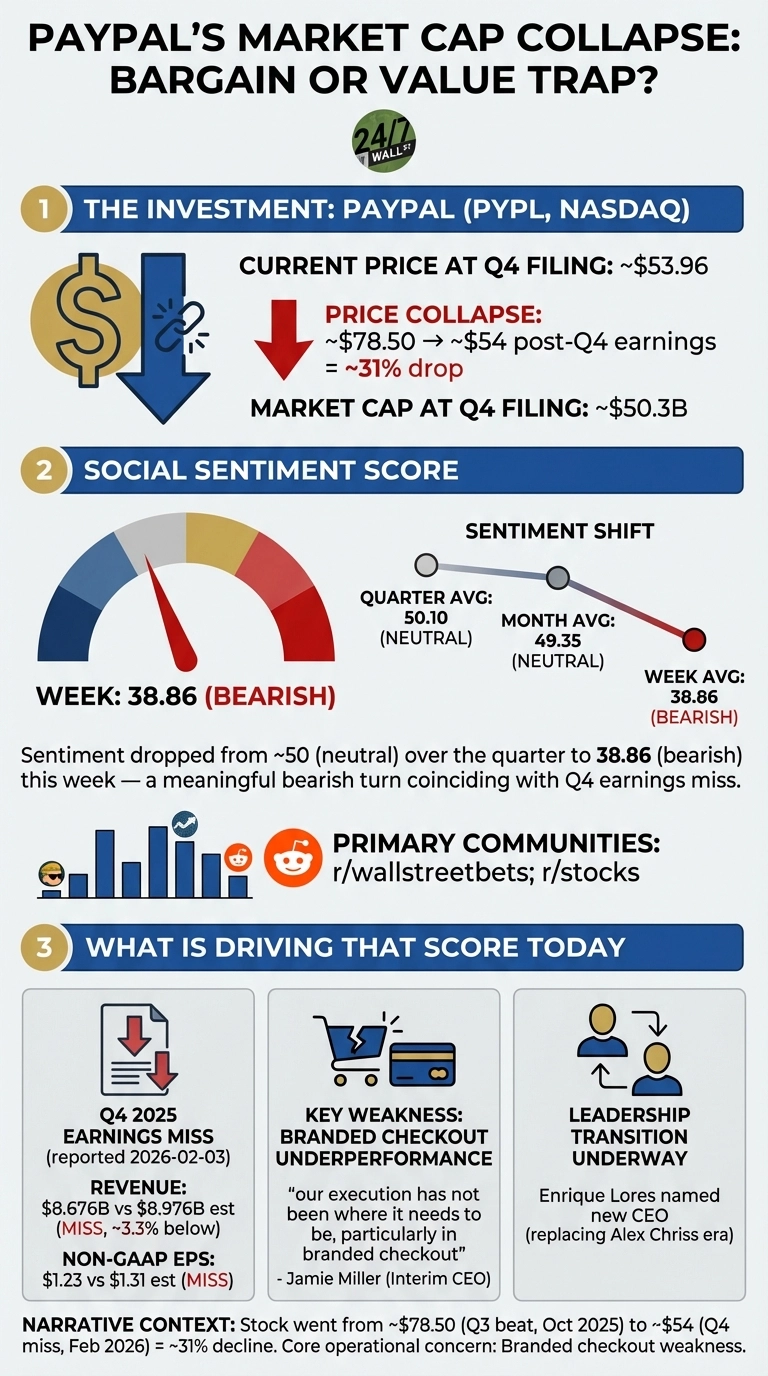

The damage accelerated after PayPal’s Q4 2025 earnings miss on February 3, 2026, when it reported revenue of $8.676 billion, missing estimates by a whopping $304 million, while non-GAAP EPS of $1.23 fell short of the consensus. The real concern is branded checkout, PayPal’s core business, which grew just 1% in Q4, down from 5% in Q3. Interim CEO Jamie Miller admitted “our execution has not been where it needs to be, particularly in branded checkout,” which sends the right signals, if he can effect the right kind of change.

Reddit Sentiment: Divided Between Bargain Hunters and Burned Bulls

On r/wallstreetbets, sentiment has turned sharply bearish, dropping to 38.86 this week from 50.10 over the quarter. The community is split between those who see and believe in the stock’s deep value and those who warn of a value trap. One post titled “PayPal shares CLOBBERED in premarket. wow!” – which garnered 5,919 upvotes – captured the immediate reaction: “wow!” as traders watched the stock crater following the Q4 miss.

PayPal shares CLOBBERED in premarket. wow!

by u/[post_author] in wallstreetbets

One post titled “Is anyone considering PayPal?” captured the longer-term tension: “The concern with buying PayPal is that it’s a value trap, i.e. it seems like a bargain, but the company has no growth potential.”

Is anyone considering PayPal?

by u/samuel_morton_trader in wallstreetbets

The bearish case is straightforward: PayPal faces intense competition, slowing growth in branded checkout, and uncertainty around leadership transition. The bullish case rests on valuation. At a forward P/E of 7.6x and a PEG ratio of 0.5, the stock trades like a company in terminal decline, even though it still generates $5 billion in annual free cash flow. Analysts have slashed price targets to the $45–$50 range, and with 60% rating it a Hold, Wall Street is clearly in “wait and see” mode.

Bargain or Trap: What the Numbers Actually Say

For now, the question is whether PayPal at $42 is either a deep value play or a falling knife? The fundamentals show a profitable company with $38.9 billion market cap trading at a steep discount, but growth has stalled where it matters most. Whether incoming leadership can execute a turnaround starting March 1, 2026, will determine if this is a bargain or a trap.