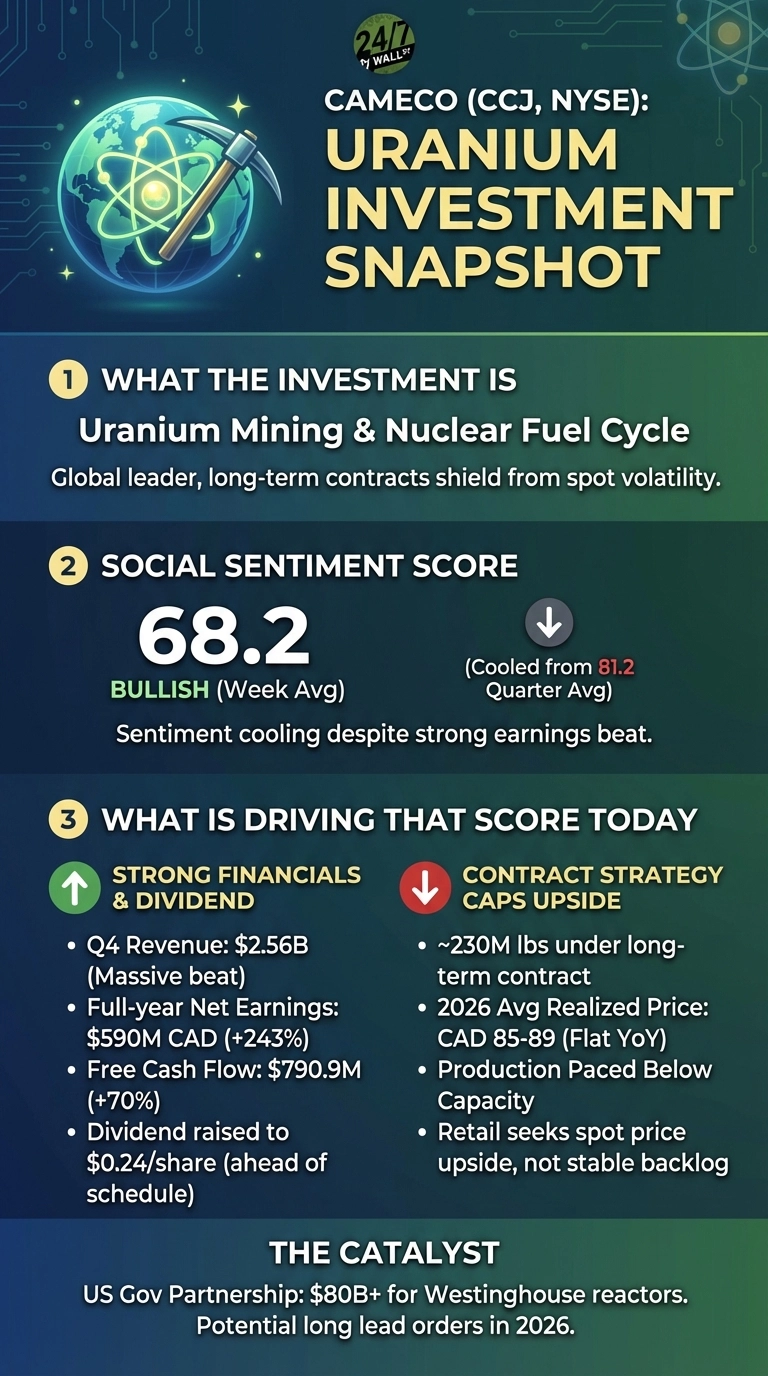

Cameco just reported a roughly 240% jump in annual earnings and raised its dividend a year early, and retail investors are cooling on the stock anyway. That gap is worth understanding. Cameco (NYSE:CCJ | CCJ Price Prediction) is trading near $118 after a strong earnings report filed on February 15, yet retail sentiment has cooled. The proprietary Reddit sentiment score dropped from 81.2 (very bullish) at the quarterly average to 68.2 (bullish) this week. That 13-point gap between financial performance and sentiment tells a specific story: Cameco’s long-term contract strategy is working as designed, and retail investors are asking whether that’s good enough.

What the Q4 Numbers Show

Looking more closely at results, full-year net earnings reached $590 million CAD, up 243% from $172 million CAD in 2024. Revenue of $2.56 billion USD definitely surpassed the $1.13 billion estimate, and free cash flow hit $790.9 million, up 70% year-over-year, leaving things looking fairly positive overall. Westinghouse contributed $780 million CAD in adjusted EBITDA, up 61%, which helped make the case for a dividend raise to $0.24 per share, one year ahead of schedule.

The contract structure enabling these results also caps upside if uranium prices accelerate. Cameco holds roughly 230 million pounds under long-term contracts, with 2026 average realized price guidance of CAD 85-89 per pound, described as “flattish” year-over-year. McArthur River, the second-largest uranium mine in the world, is being operated well below its 25 million-pound licensed capacity, with 2026 production guided to 19.5-21.5 million pounds. CEO Tim Gitzel called it discipline: “This discipline stems from our commitment to our long-term strategy, allowing us to look past the distractions posed by short-term volatility.”

Where Retail and Management Diverge

The most active Reddit thread, “Volume IV: The Atomic Bits Thesis – Why Atoms are the New Software”, drew 117 upvotes and 77 comments. The thesis: “By holding CCJ and UUUU, I am investing in the ‘fuel’ for the AI era.” (UUUU refers to Energy Fuels (NYSE:UUUU).)

Volume IV: The Atomic Bits Thesis – Why Atoms are the New Software

by u/[OP] in wallstreetbets

Retail is betting on spot price upside. Cameco is rationing supply to preserve pricing leverage for future contracts.

- 2026 realized uranium price guidance is flat year-over-year at CAD 85-89/lb

- Long-term contracting volumes in 2025 reached only 116 million pounds, well below the 150+ million pounds per year that utilities need to replace depleting contracts, meaning the market is not locking in supply fast enough to drive Cameco’s next pricing step-up

- 2026 CapEx guidance of $490-540 million, which is higher than 2025 levels, compressing near-term free cash flow

The Catalyst That Changes the Picture

For investors taking a closer look at Cameco, the balance sheet is not a concern, with $1.2 billion in cash against $1.0 billion in total debt, all while analysts hold an average price target of $125.59. Of course, the real watch item is whether the U.S. government partnership targeting at least $80 billion in Westinghouse reactor deployment moves from a term sheet to a signed agreement. CFO Grant Isaac on the earnings call: “We do believe there’s a good chance that we will see a long lead item order as part of this program in 2026… 2026 is set to be a pretty transformative year where announcements turn into action on the gigawatt scale.” If that materializes, the contracted backlog no longer looks like a ceiling.