Chip stocks get all the applause in an AI rally, but the quiet money often hides in the plumbing. Corning (NYSE:GLW | GLW Price Prediction) is a clean example of that, with the stock up roughly 200 percent over the past year, a run that has surprised people who still think of it as “just glass.”

This company does make lots of glass, ceramics, and the like, but do you know what else needs glass? Fiber AI. Data centers now need tremendous amounts of switches, racks, and clusters, and no matter how fancy all that silicon is, you need something to connect them. Meta (NASDAQ:META) has even committed to pay Corning up to $6 billion through 2030 for fiber optic cable for its AI data centers, which tells you this is no longer a niche upgrade.

The reputation of Corning as just a glass company has kept it hidden. Hence, I’d like to call this a “stealth AI company,” since most investors just skim over and don’t come to realize how excellent a pick-and-shovel play this is.

Why I see Corning surging much higher from here

Data centers that run AI models need five times more optical connectivity than they have today. The demand is enormous, and companies are willing to pay for multiple years of supply. AI companies don’t spend significant amounts on optical fiber, but without it, the data center buildout would be paralyzed.

Corning is also seeing demand from data centers that need to replace their copper wiring with optical fibers. Bloomberg sees up to 2.4 million tons of copper usage in North American data centers alone by 2030. Copper is fine for small-scale nodes, but once you start working with hundreds of GPUs per node, it begins to make optical fiber much more cost-effective.

Speaking of cost-effectiveness, copper prices have been soaring.

Corning is set to be among the biggest beneficiaries because of this.

Recent reports have pointed out that a looming copper shortage could put the data center buildout in danger. If that happens, optical fiber will start being a necessity.

Are you paying the right price for GLW stock?

Corning is trading quite expensively right now, and it’s worth looking into how much you’re paying for the stock before you put any money here. The earnings ratios are truly rich, with the forward P/E ratio at over 51 times. For a small AI startup that just turned profitable, this is not that expensive.

The equation is different for GLW stock since Corning is a mature business that already generates cash.

The historical forward PE ratio hovered around 20-25x during rallies and near 12x during downturns. What we’re seeing now is worth being a little cautious about. The market has been slapping higher and higher premiums these past few months.

I believe the market is set to pay more for GLW stock as the momentum is there, and it’s still accelerating. There has never been such an aggressive data center buildout, and by the time it’s done, the company’s $135.4 billion market cap today could look like a steal.

So, what’s warranting this higher premium?

The Meta deal is the biggest factor here. Wall Street likely expects other hyperscalers to join in to secure their optical cable supply. Moreover, even before the Meta deal, Corning had built a convincing track record. The company posted four consecutive earnings beats throughout 2025, with full-year core EPS climbing 26% and operating margins expanding to 20.2%, which they hit a full year ahead of their own internal schedule. In Q4 specifically, net sales grew 20% to $4.22 billion. The Optical Communications segment alone grew 24% year-over-year in Q4, with enterprise sales growth at 58% in Q3 from Gen-AI product adoption.

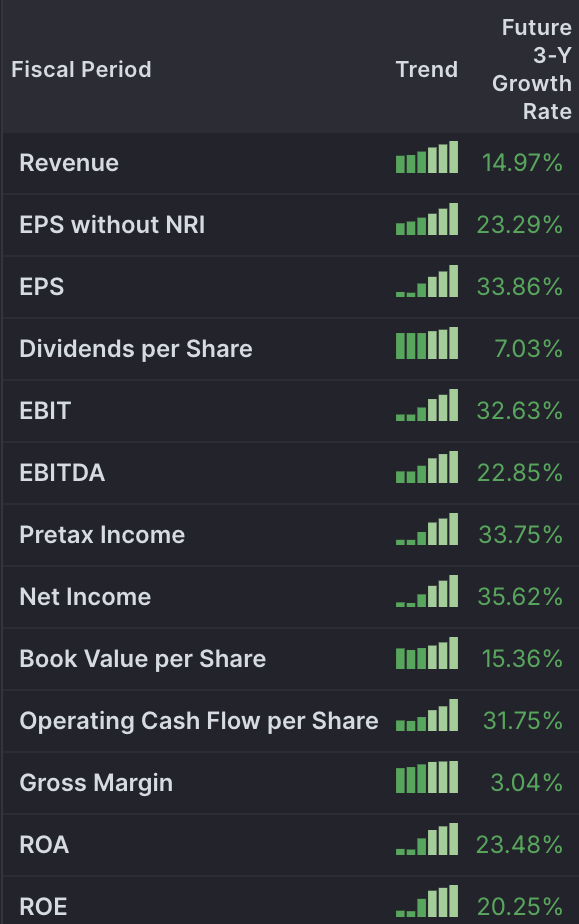

The future likewise looks bright. Note that the growth rates below reflect average annual growth rates.

Corning’s internal growth roadmap, which they call the “Springboard” plan, has been revised upward multiple times. It originally targeted $3 billion in additional annualized sales. Management has since raised the goal to $11 billion in incremental annualized sales by 2028. They see $20.7 billion in sales and earnings of $2.6 billion by 2028. That’s about 13.4% annual revenue growth from here. Wall Street is buying what they’re selling, with analysts now expecting EPS to nearly triple to $7.01 by 2030.

You’ll be right to point out that even if that $2.6 billion in earnings gets a 50x premium, GLW stock is going to go down and trade at a $130 billion market cap. However, I believe the projections are set to keep going up. Soaring copper prices will make fiber more cost-effective, and the data center buildout remains unrelenting. I wouldn’t touch GLW stock if you’re worried about valuations. This is not a value trade and is purely meant for your growth portfolio. I’d argue this mature copper business has more staying power than chip stocks that are always fighting for market leadership.