Another giant in the oil world, ConocoPhillips (NYSE:COP | COP Price Prediction) has climbed 25% year-to-date and 29% over the past year. The question driving skepticism among investors: did the Marathon Oil integration actually create value, or did ConocoPhillips buy growth it could have built cheaper?

What the Marathon Numbers Actually Show

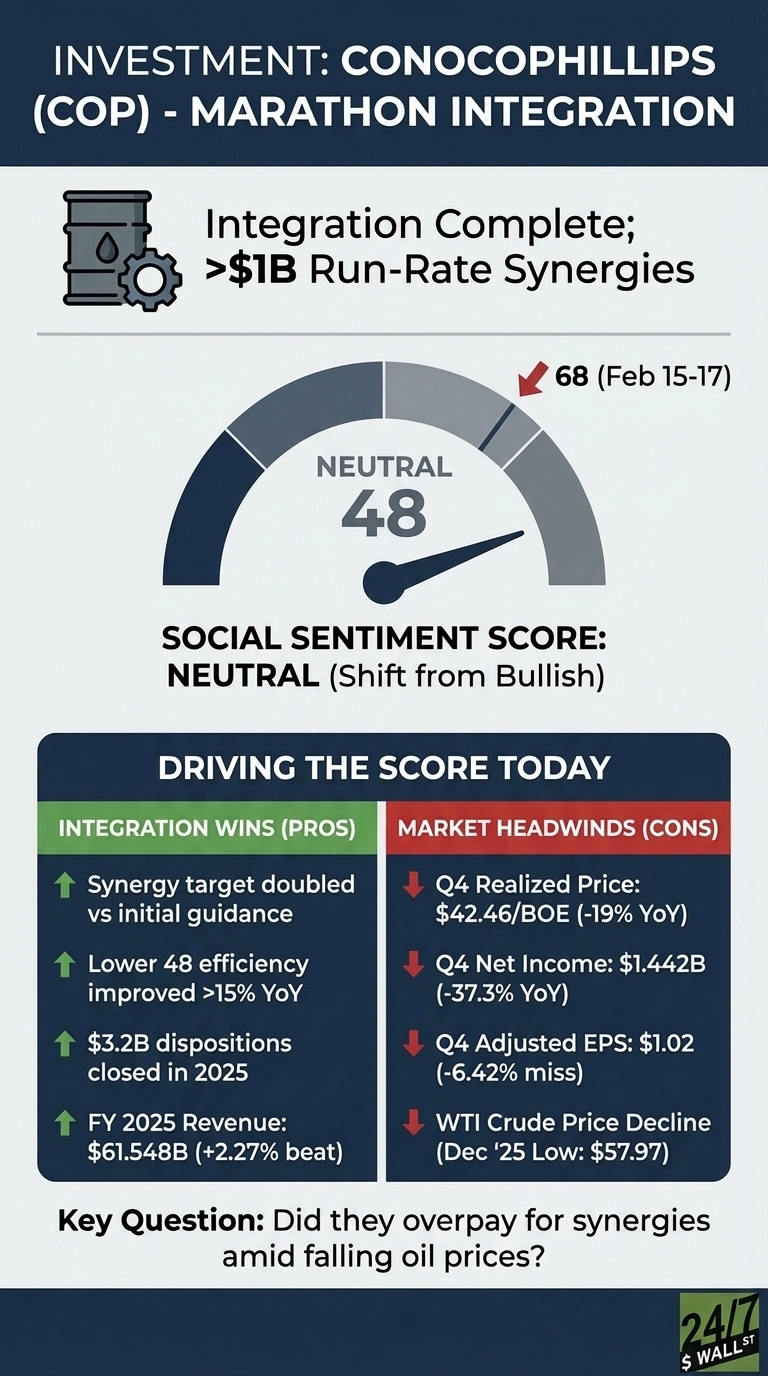

The good news is that management’s case is concrete: ConocoPhillips says it doubled synergy capture from the Marathon deal, realized a further $1 billion in one-time benefits, and completely eliminated the Marathon capital program, while still delivering pro forma production growth. Lower 48 drilling and completion efficiency improved more than 15% year-over-year, and the company returned $9 billion to shareholders in 2025, representing 45% of cash flow from operations.

The harder question is whether those wins hold up amid falling oil prices. WTI averaged $57.97 per barrel in December 2025, the lowest point of the year, and ConocoPhillips’ average realized price fell 19% year-over-year to $42.46 per BOE in Q4. Net income dropped 38.09% year-over-year in the quarter, and the synergies are real, but commodity headwinds are doing their best to obscure them.

ConocoPhillips’ $7 Billion Bet and What Could Break It

Goldman Sachs added ConocoPhillips to its US Conviction List on March 2, 2026, citing the company’s pivot from heavy investment into “harvesting” mode. Goldman projects cash flow per share growth at a 24% CAGR between 2025 and 2030. Management’s own target calls for $7 billion in incremental free cash flow by 2029, including $1 billion per year from 2026 through 2028. The projections assume Brent crude averaging around $70 per barrel, a level that geopolitical disruption or sustained OPEC supply could swing sharply. Analyst price targets sit near current levels at $117.63, suggesting integration value is largely priced in. The 2029 FCF inflection is the next real test.