Short interest in Strategy (NASDAQ: MSTR | MSTR Price Prediction) is climbing, and the bears building positions aren’t simply fading a Bitcoin trade. They’re identifying a structural mismatch between what the stock represents and what it actually delivers to common shareholders.

The Bull Case (That Deserves Respect)

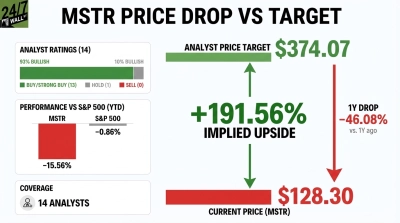

The bull thesis is straightforward: Strategy holds 738,731 BTC, making it the largest corporate Bitcoin holder in the world. CEO Phong Le has repeatedly demonstrated capital markets execution, raising $25.3 billion in 2025 alone—the largest U.S. equity issuer for two consecutive years. Analysts remain overwhelmingly bullish, with 14 Buy ratings and a consensus price target of $378.71 against a current price of $138.46. During Bitcoin bull runs, this model works spectacularly.

Why the Short Thesis Is Compelling Now

The $150,000 Bitcoin assumption collapsed. Strategy’s FY2025 guidance was built on Bitcoin reaching $150,000 by year-end. It didn’t come close. Bitcoin is currently trading around $69,498, or down 20.12% year-to-date. That miss produced a $17.44 billion unrealized loss in Q4 2025 and a net loss of $12.44 billion for the quarter. EPS came in at −$42.93 versus the consensus estimate of −$15.66, which is a miss of over 174%.

Dilution is relentless. Authorized shares were expanded from 330 million to 10.33 billion class A common shares. As of early February 2026, over $29 billion remained available across preferred ATM programs. Every Bitcoin purchase is funded by issuing equity above book—which works until sentiment turns.

Preferred shareholders eat first. Strategy (NASDAQ: STRC) dividends are now running at 11.5% annualized, escalating from 9% just months earlier. These perpetual obligations rank above common equity, creating a structural drag that compounds as the preferred stack grows.

The software business is hollowing out. Product support revenue fell 16.9% year-over-year in Q4 2025, consistent erosion across all four quarters of 2025. Total annual software revenue of $477 million provides almost no cushion if Bitcoin deteriorates further.

What Could Break the Bear Case

A sharp Bitcoin rally toward six figures would reverse the narrative quickly. Prediction markets currently assign only 38% probability to Bitcoin reaching $100,000 by year-end, but that scenario would generate massive unrealized gains and potentially reignite equity issuance at favorable premiums. A short squeeze is also a real possibility: with a beta of 3.633, Strategy stock moves violently in both directions.

The Bottom Line

Strategy has fallen 42.13% over the past year and is 69.7% below its 52-week high of $457.22. For retirement-focused investors, the combination of extreme Bitcoin dependency, accelerating dilution, and growing preferred obligations above common equity makes this a stock to avoid at current levels—regardless of conviction on Bitcoin itself.