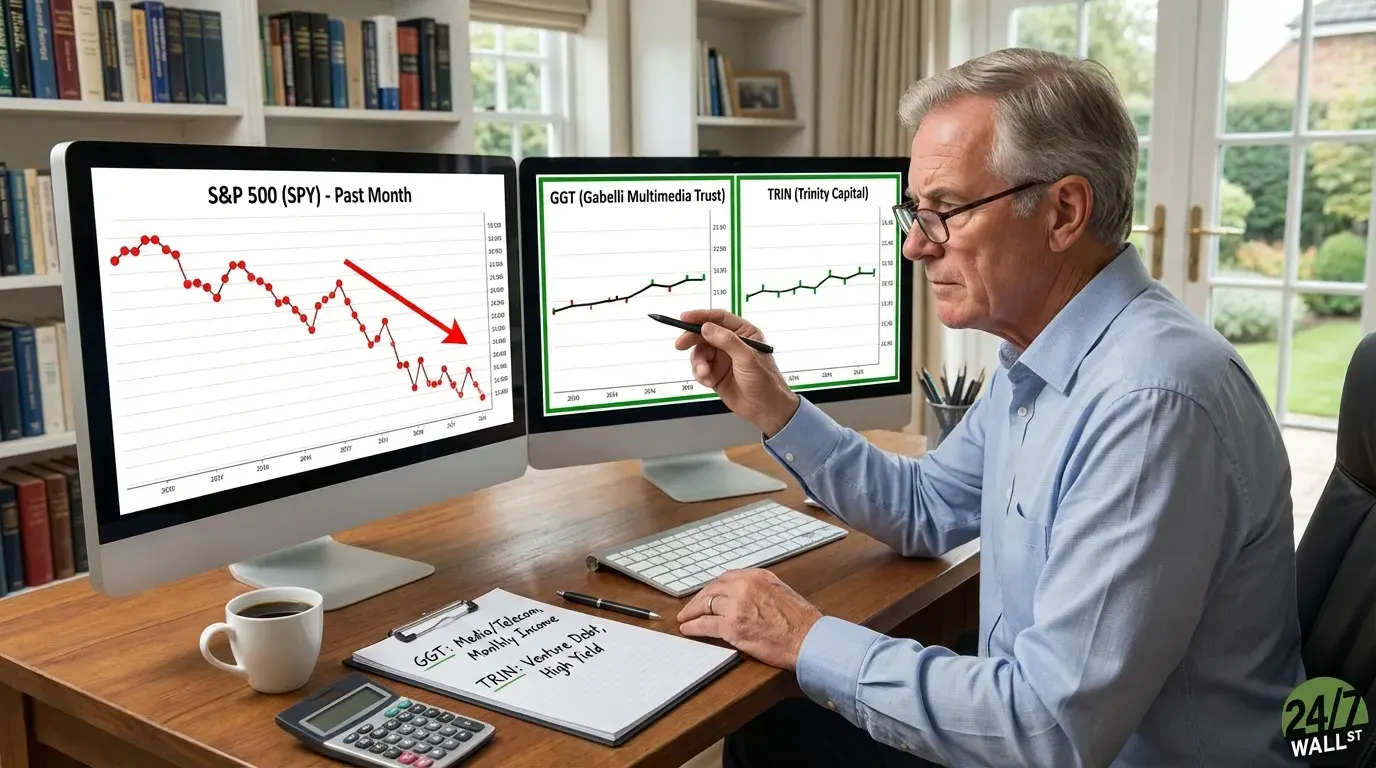

The S&P 500 has dropped roughly 2.5% over the past month, with the VIX fear gauge sitting at 27.29 as of mid-March, reflecting the kind of elevated uncertainty that rattles growth-heavy portfolios. For income-focused investors, two names worth understanding in this context are Gabelli Multimedia Trust (NYSE:GGT) and Trinity Capital (NASDAQ:TRIN), both of which have held their ground while the broader market retreated.

What These Two Funds Actually Do

GGT is a closed-end fund managed by Gabelli Funds that invests in media and telecommunications companies. Closed-end funds trade on exchanges like stocks, but unlike mutual funds they have a fixed share count and can trade at a discount or premium to the value of their underlying holdings. GGT’s return engine is the appreciation of its media-sector holdings combined with a steady distribution to shareholders. It has paid distributions without interruption for over 26 years, recently transitioning from a quarterly structure to monthly payments of $0.07 to $0.08 per share.

Trinity Capital operates differently. It is a Business Development Company, or BDC, which functions similarly to a closed-end fund but lends money to growth-stage companies rather than buying public equities. Trinity specializes in venture debt, providing equipment financing and secured loans to startups that need capital but aren’t ready for traditional bank lending. By law, BDCs must distribute most of their taxable income to shareholders, which is why they tend to carry high yields. Trinity’s effective yield on its debt portfolio was 15.2% in Q4 2025, and it recently shifted to monthly dividend payments of $0.17 per share starting in January 2026.

The Resilience Case During the Selloff

Over the past month, GGT is up 0.48% and TRIN is up 0.10% while SPY has fallen roughly 4.3%. That relative stability matters to retirement investors because it reflects how income-generating structures behave differently from growth equities during risk-off periods. When investors flee equities, funds with predictable cash flows and high current income can act as ballast.

Trinity’s income story is supported by real fundamentals. Full-year 2025 revenue grew 24% year-over-year to $293.7 million, and the company covered its quarterly dividend at 102% of net investment income in Q4 — meaning distributions were fully earned, not borrowed from capital. CEO Kyle Brown described 2025 as a “milestone year” with record originations and earnings growth, citing record originations and earnings growth as evidence that the venture lending model is scaling.

That operational momentum is reflected in how the market prices the stock. Trinity trades near $14.42, a modest premium to its NAV of $13.42 per share, and analysts have set a consensus price target of $16.61 — suggesting the premium is seen as justified by the quality of the portfolio and its earnings trajectory.

The Tradeoffs Retirement Investors Should Understand

Neither fund is without risk. Trinity’s share count grew from 59.4 million to 77 million year-over-year, which dilutes existing shareholders and is part of why net investment income per share declined even as total earnings grew. The company also recorded $64.3 million in net realized losses for the full year, a figure that deserves attention from anyone relying on capital preservation alongside income.

GGT’s media-sector concentration means it is exposed to structural headwinds in legacy telecommunications and traditional media, industries under sustained pressure from streaming and cord-cutting trends. Its five-year total return of -12% reflects that reality. The income has been consistent, but the price has not kept up.

GGT has historically appealed to investors seeking steady monthly distributions, while Trinity’s high yield reflects the credit risk profile of its venture lending portfolio. Lending to pre-profitable startups carries real default risk, and the spread over the 10-year Treasury at 4.27% is compensation for that risk, not a free lunch. Retirement investors weighing these two structures should consider whether they are prioritizing sector-concentrated equity income with a long distribution track record, or floating-rate venture debt income with higher yield and higher credit exposure.