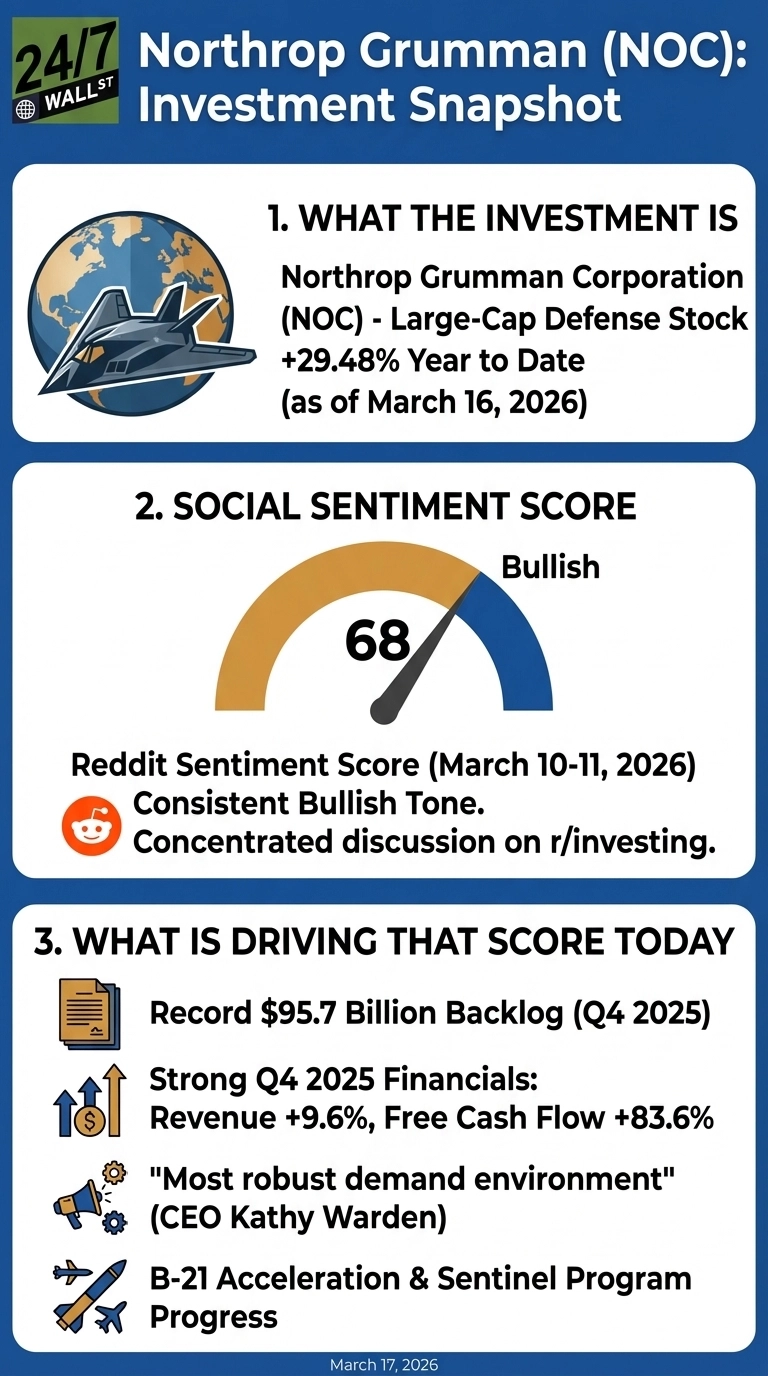

One of the world’s foremost defense and aerospace names, Northrop Grumman (NYSE:NOC | NOC Price Prediction) has been one of the strongest-performing large-cap defense stocks of 2026, with shares up 29.07% year to date to around $735. That run is built on a real foundation: a record $95.7 billion backlog, a Q4 earnings beat, and a CEO who described the current environment as “the most robust demand environment I’ve seen in my career.” But the stock now trades above analyst consensus targets, and the Sentinel ICBM program is still in restructuring. The tension between a record backlog and unresolved program costs is what investors are watching.

A $96 Billion Backlog With a Conversion Problem

Northrop Grumman closed FY2025 with over $46 billion in net awards and a full-year book-to-bill ratio of 1.10x. Free cash flow for the year rose 26% to $3.3 billion, marking the third consecutive year of 25%+ growth. Q4 revenue grew 9.6% year over year to $11.71 billion. CEO Kathy Warden described the 2026 outlook as a “balanced approach,” noting that while production is ramping up, major revenue impacts from B-21 acceleration, Collaborative Combat Aircraft (CCA), and munitions expansion will be more pronounced in 2027 and 2028.

The Sentinel ICBM remains a focal point of the restructuring, which is expected to conclude in late 2026. With a test launch planned for 2027 and operational capability targeted for the early 2030s, the program is moving from digital design to physical reality; notably, the company broke ground on a prototype silo in Utah this February. Defense Systems revenue grew 14% in Q4, bolstered significantly by the ongoing Sentinel development.

Reddit’s r/investing Is Quietly Bullish

Discussion on Northrop across Reddit is low but consistently bullish, concentrated in r/investing, with sentiment scores holding between 64 and 68 through early March. The crowd skews toward longer-horizon investors focused on the defense spending cycle and backlog conversion. A recent r/investing thread on NOC reflected the prevailing view, with participants focused on backlog conversion and the potential for B-21 ramp and Sentinel resolution to serve as catalysts into 2027.

NOC backlog conversion thread

by [username] in investing

The bullish case rests on three pillars:

- Northrop’s record $95.7 billion backlog provides multi-year revenue visibility, with management guiding for $43.5 to $44 billion in 2026 sales and stronger growth in 2027.

- The B-21 Raider acceleration deal, which closed in late February 2026, involved a $2 to $3 billion investment over a multiyear period with improved return potential.

- International momentum is building, with 20 countries having formally requested IBCS and international sales expected to grow 20% in 2025.

Valuation Is Where Bulls and Bears Split

However, valuation remains a point of contention. While peer Lockheed Martin (NYSE:LMT) trades at roughly 19x trailing earnings, Northrop’s current 25x multiple has pushed shares to $736, already above the analyst consensus target of $724. With a DCF-based fair value estimate sitting closer to $513, much of the B-21 and Sentinel optimism appears priced in. The next catalyst will be Q1 2026 volume trends and whether Sentinel’s restructuring can maintain its 2027 test flight schedule without further cost creep.