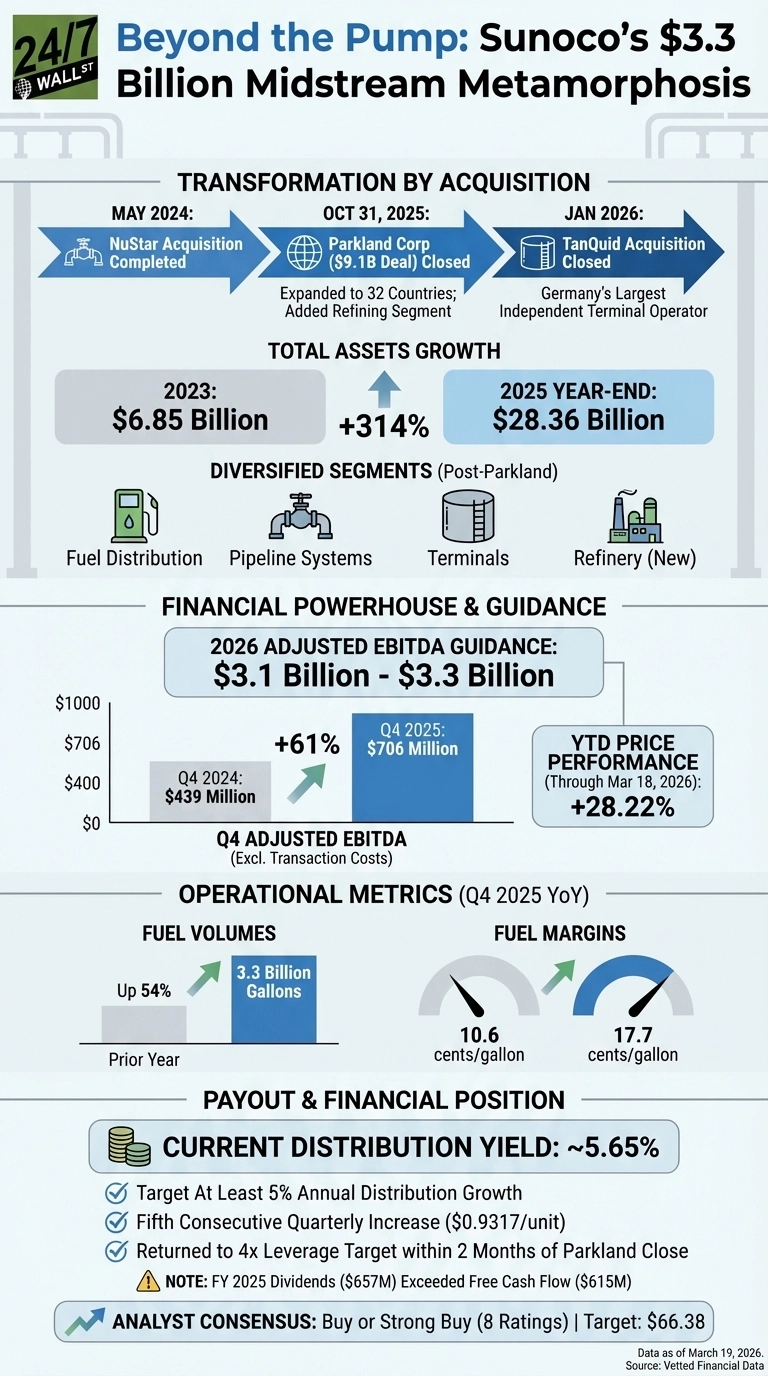

Sunoco LP (NYSE:SUN | SUN Price Prediction) has spent the past 18 months executing one of the most aggressive transformation strategies in the midstream MLP space, and the numbers now demand a serious look. The partnership is guiding for $3.1 billion to $3.3 billion in Adjusted EBITDA for 2026, roughly triple what the legacy fuel distribution business generated just a few years ago. Units are up 28.22% year-to-date through March 18, 2026.

A Company Rebuilt by Acquisition

The catalyst was a rapid-fire series of deals. The $9.1 billion Parkland Corporation acquisition closed October 31, 2025 instantly expanded Sunoco’s footprint to 32 countries and added a refining segment. TanQuid, Germany’s largest independent terminal operator, closed in January 2026. The NuStar deal, completed in May 2024, drove the Pipeline Systems segment from zero to a meaningful contributor. The balance sheet reflects the scale: total assets grew from $6.85 billion in 2023 to $28.36 billion by year-end 2025, while long-term debt reached $13.37 billion.

Q4 2025 illustrated the new earnings power. Adjusted EBITDA hit $706 million for the quarter, excluding $60 million in one-time transaction costs. Fuel volumes reached 3.3 billion gallons, up 54% year-over-year, with margins expanding to 17.7 cents per gallon from 10.6 cents in the prior year period.

The Payout Math That Confuses Investors

The Q4 GAAP EPS of $0.09 missed the $1.44 estimate by 93.75% missed the $1.44 estimate by a wide margin, which looks alarming until you understand the structure. Acquisition-related D&A surged to $219 million from $152 million, and interest expense climbed to $166 million from $117 million. For MLPs, Distributable Cash Flow is the relevant coverage metric, and the trailing twelve-month coverage ratio stood at 1.9 times at year-end.

The FCF picture deserves scrutiny. Full-year 2025 dividends of $657 million exceeded free cash flow of $615 million exceeded free cash flow of $615 million. FY 2024 was worse, with FCF of just $205 million against $566 million in distributions. Management targets at least 5% annual distribution growth, and the most recent quarterly distribution of $0.9317 per unit marks the fifth consecutive quarterly increase.

CEO Joseph Kim framed the financial position confidently on the Q4 call: “Our financial position continues to be stronger than at any time in Sunoco’s history.” He also noted the partnership returned to its 4x leverage target within two months of the Parkland close, well ahead of the original 12-to-18-month timeline.

What Investors Should Watch

The 2026 EBITDA guide assumes $125 million of the $250 million total Parkland synergy target realized this year, with management expecting to exit 2026 “well north” of that run-rate. Sunoco committed to at least $500 million annually in bolt-on acquisitions as a floor. With $2.5 billion in revolving credit availability and leverage already at target, the balance sheet has room. The current distribution yield sits at approximately 5.65%, and all eight analyst ratings are Buy or Strong Buy with a consensus target of $66.38. The transformation thesis is intact; execution on synergies and FCF improvement will determine whether the distribution growth story holds through the integration cycle.