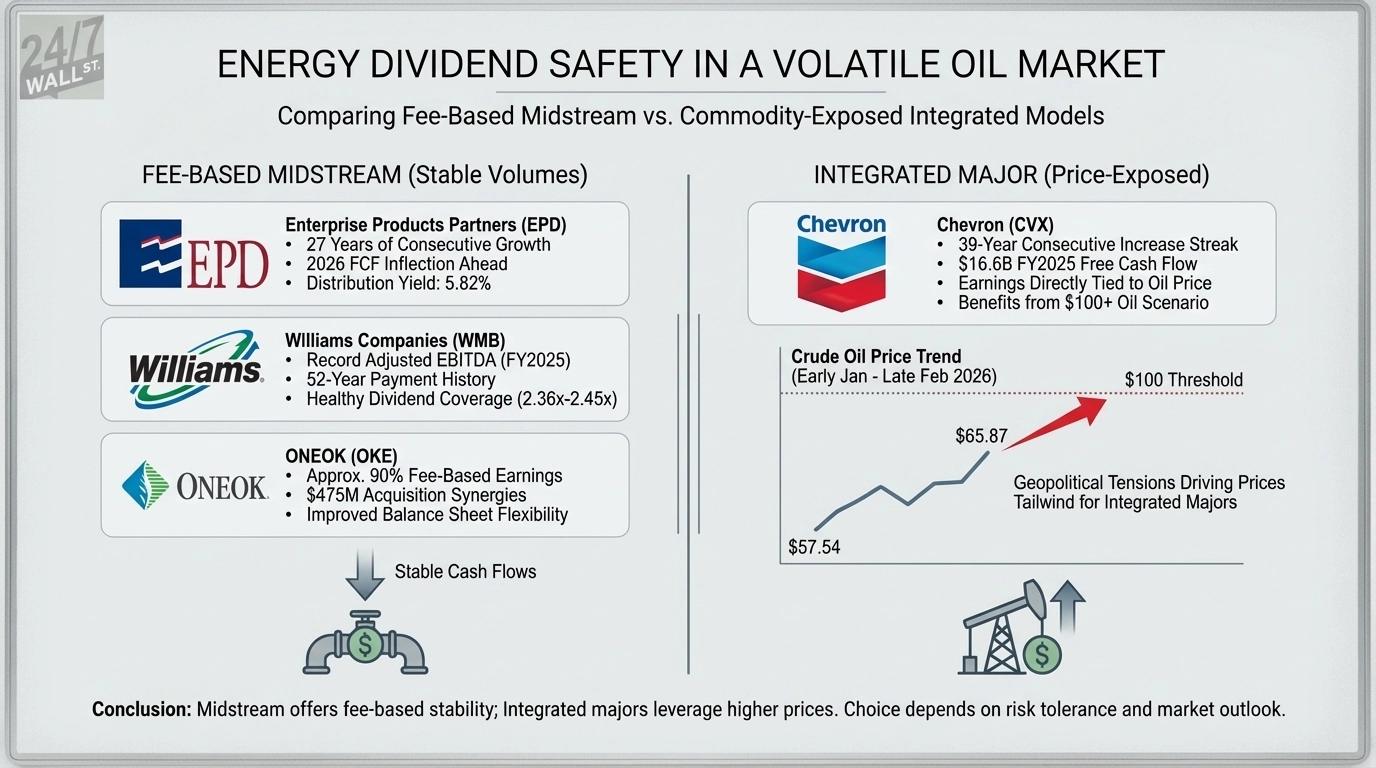

With Iranian Supreme Leader Ayatollah Ali Khamenei’s death on February 28, 2026 escalating Middle East tensions, crude oil has climbed from $57.54 in early January to $65.87 by late February, and the $100 conversation is back. For income investors, the question is not whether oil spikes, but whether your energy dividends survive any price environment. The answer depends heavily on which type of energy company you own.

Midstream vs. Integrated: Two Very Different Dividend Stories

The three midstream names here operate on fee-based models, meaning oil price direction matters far less than volumes. Enterprise Products Partners (NYSE:EPD | EPD Price Prediction), Williams Companies (NYSE:WMB), and ONEOK (NYSE:OKE) collect tolls on energy infrastructure. Chevron (NYSE:CVX), as an integrated oil major, is most directly exposed to where crude goes next.

Enterprise Products Partners: 27 Years of Growth, FCF Inflection Ahead

| Metric | Value | Assessment |

|---|---|---|

| Annual Distribution | $2.20/unit | Annualized Q4 rate |

| Distribution Yield | 5.82% | Attractive for income |

| Consecutive Years of Growth | 27 years | Exceptional streak |

| FY2025 Operating Cash Flow | $8.585B | Strong |

| FY2025 FCF | $3.006B | Heavy capex year |

EPD’s 2025 organic growth capex of roughly $4.5B compressed free cash flow, but that cycle is ending. 2026 growth capex drops to $1.9B-$2.3B, which should meaningfully expand distributable cash. CEO Jim Teague said in Q3 2025: “With this large wellhead to water build out cycle behind us, we believe 2026 will see an inflection point in the partnership’s free cash flow.” The distribution coverage metrics point to a stronger free cash flow backdrop heading into that inflection.

Williams: Record EBITDA, Comfortable Coverage

Williams delivered record adjusted EBITDA of $7.75B in FY2025, capping a five-year EBITDA CAGR of 9%. The company raised its dividend 5% for 2026, to $0.525 per quarter. Management guides 2026 dividend coverage of 2.36x-2.45x, a healthy cushion. With 52 consecutive years of dividend payments and a Transco pipeline that is essentially irreplaceable infrastructure, Williams has historically maintained dividend payments regardless of where WTI trades.

ONEOK: Acquisition Integration Paying Off

ONEOK raised its quarterly dividend from $1.03 to $1.07 in February 2026, a 4% increase. With approximately 90% fee-based earnings and $475M in cumulative acquisition synergies through year-end 2025, the business has grown substantially. The company extinguished roughly $3.1B of long-term debt in 2025, improving balance sheet flexibility. CEO Pierce Norton noted: “ONEOK delivered another year of double-digit earnings growth in 2025, with increased volumes and continued synergy capture from a multi-year acquisition plan highlighting the value created by our integrated systems.”

Chevron: The One That Actually Needs $100 Oil

Chevron is the outlier. Its $7.12 annualized dividend is backed by a 39-year consecutive increase streak and $16.6B in FY2025 free cash flow. But with Brent averaging $64/barrel in Q4 2025 and oil still well below the widely discussed $100 threshold, earnings are under pressure. Quarterly earnings fell 23.8% year-over-year. The dividend is safe for now given the balance sheet, but a sustained low-price environment would force Chevron to fund it from debt. A move toward the $100 level would be a direct earnings tailwind. CEO Mike Wirth acknowledged the challenge: “This resulted in industry-leading free cash flow growth and superior shareholder returns, despite declining oil prices.”

Comparing the Dividend Structures: Fee-Based vs. Commodity-Exposed

EPD, Williams, and ONEOK operate fee-based models that historically keep distributions stable whether crude is at $65 or the widely discussed $100 threshold. Chevron’s dividend carries a 39-year track record and a strong balance sheet, but its earnings are more directly tied to where oil prices settle. If geopolitical risk keeps oil elevated, Chevron stands to benefit most from a price perspective. If prices retreat, the fee-based midstream structure has historically provided more stable cash flows.