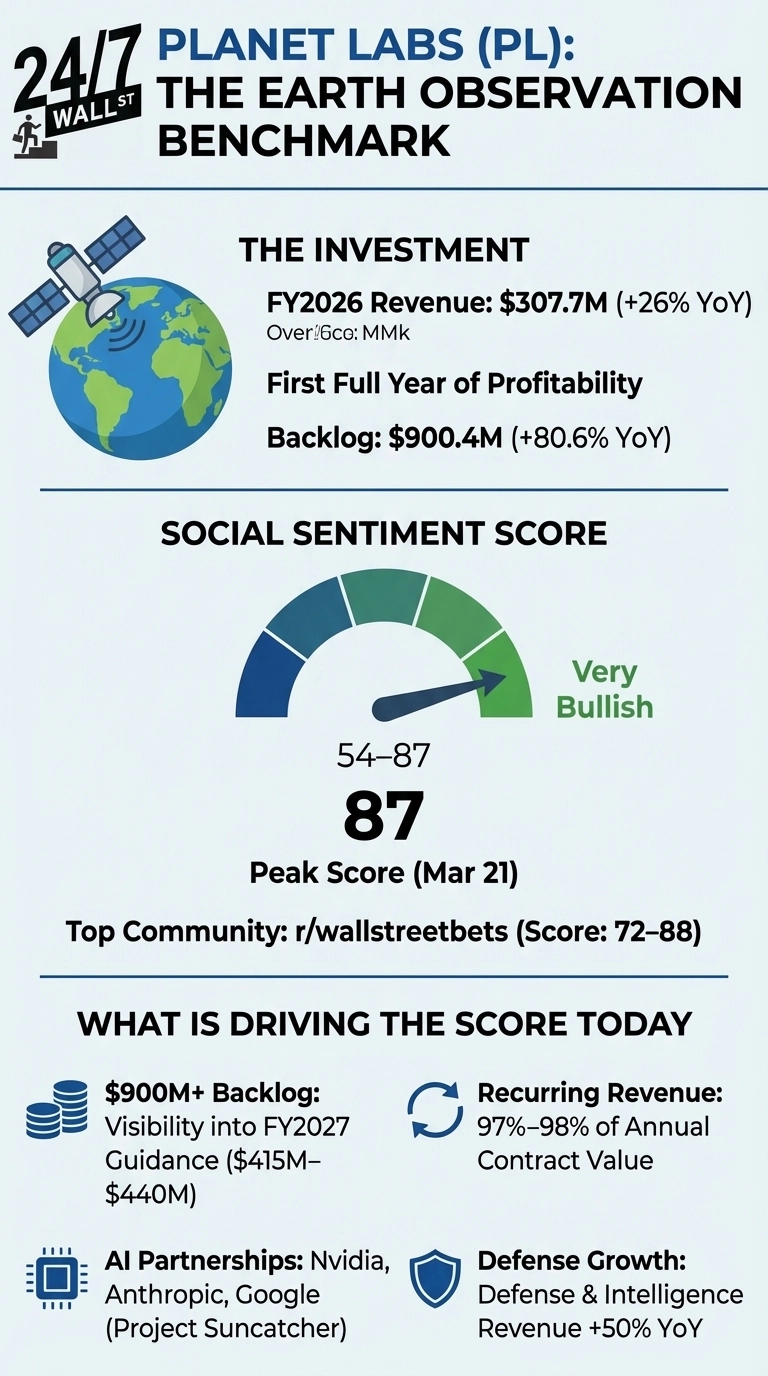

Operating the largest fleet of imaging satellites, Planet Labs (NYSE:PL) just delivered its first full fiscal year of profitability, and Reddit noticed immediately. Shares have risen 765% over the past year, from roughly $4 to $33, touching an all-time high of $36.28 on March 20, 2026, after Planet Labs reported $307.7 million in full-year FY2026 revenue, a 26% increase year-over-year. The clearest driver is a backlog that has ballooned to $900.4 million, up 80.6% year-on-year, exceeding the company’s entire annual revenue and giving management clear visibility into FY2027 guidance of $415 million to $440 million.

Why Reddit Is Using Planet Labs as the Space Sector Benchmark

Social sentiment for PL has remained “Very Bullish” since earnings, with scores ranging from 54 to 87 over the past week, peaking at 87 on March 21. The most active community is r/wallstreetbets, consistently scoring 72 to 88, while r/stocks shows more measured enthusiasm around 54 to 86. On r/stocks, user currysoup19 captured the prevailing mood: “While everyone was chasing the $RKLB and $ASTS pumps, Planet Labs just dropped a monster Q4 report and the market is finally waking up.”

On r/wallstreetbets, a post titled “Planet Labs – A Short Story” framed the business model plainly: “Imagine Google Maps, but it updates every 24 hours instead of every few years, and the CIA uses it.” The bulls cite three pillars:

- Defense and Intelligence revenue jumped 50% year-over-year in FY2026, driven by sovereign contracts with Germany and Sweden and expanding NATO surveillance agreements.

- 97% to 98% of Annual Contract Value is recurring, giving the backlog genuine predictive weight rather than one-off project noise.

- AI partnerships with Nvidia, Anthropic, and Google are positioning Planet Labs to move beyond imagery sales into orbital AI infrastructure, with Project Suncatcher targeting two prototype satellites in 2027.

Planet Labs – A Short Story

by u/redpillsbluepills in wallstreetbets

Margin Discipline Is the Watch Item Heading Into FY2027

A recent r/wallstreetbets due diligence post titled “SATL DD: The Next Planet Labs” used PL as the maturity benchmark for Earth observation, with the author describing Satellogic as “much earlier, much messier, and much riskier than Planet Labs.” Planet Labs has become the reference point for the entire Earth observation sector, a sign that its narrative has shifted from speculative to established.

For investors keeping a close eye on the stock, FY2027 EBITDA guidance of $0 to $10 million reflects near-term investment pressure from satellite manufacturing and R&D, and Q4 guidance implies an adjusted EBITDA loss of $3 million to $6 million, temporarily breaking the profitability streak. Management is betting that the Berlin facility expansion, which will add roughly 70 new employees to double Pelican’s production capacity, will pay off in contract delivery speed. With $443 million in cash on hand, they have the runway to make that bet, and investors are going to keep a close eye to see how things turn out.