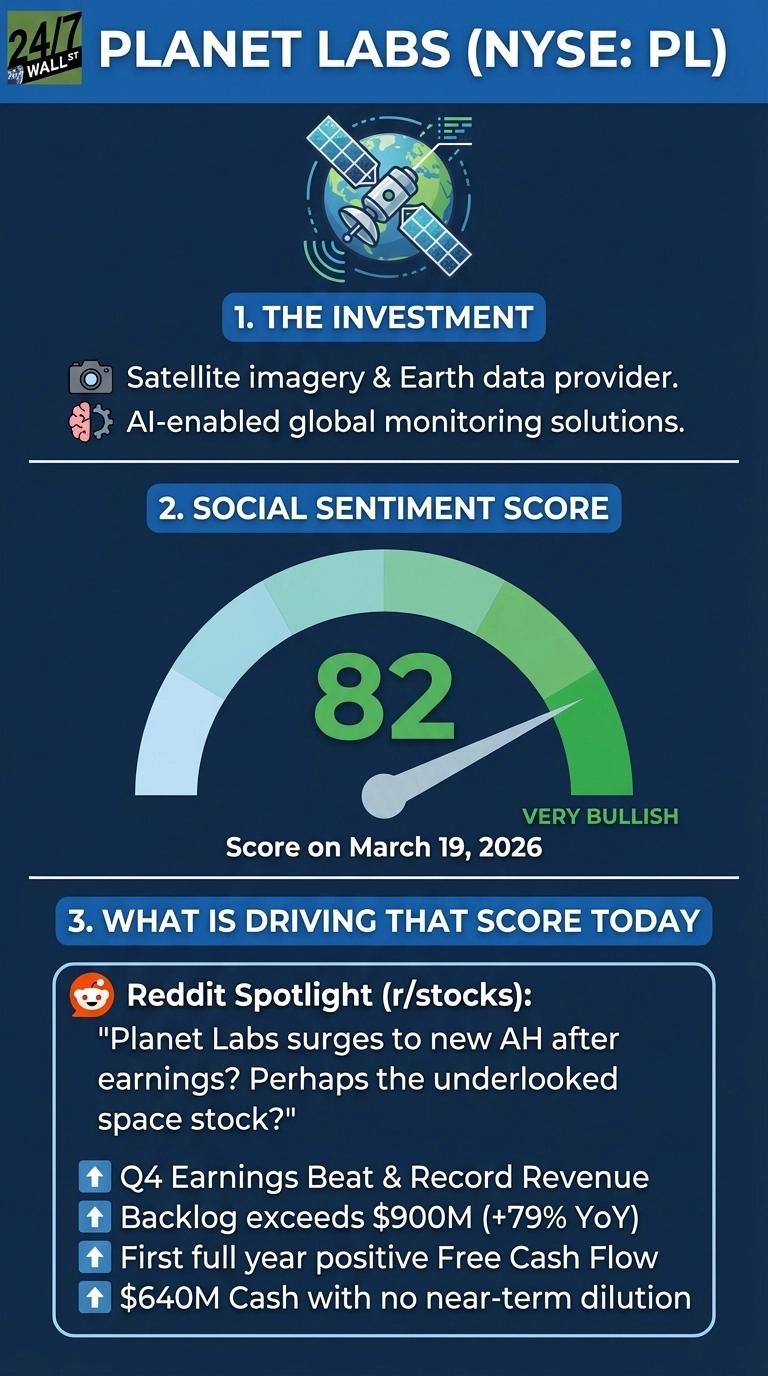

Planet Labs (NYSE:PL), a leading provider of global, daily satellite imagery and geospatial solutions, saw its shares jump 23% after hours on March 19 after the company posted its largest quarterly revenue ever and a backlog that now exceeds its entire annual revenue. Moving into the following day, shares surged 29% on March 20 after Q4 revenues hit $86.82 million, a 41% year-over-year jump that beat analyst estimates by 10.6%. The company also crossed a milestone that has eluded it for years: its backlog reached $900.4 million, up 80.6% year-on-year. Reddit volume on PL jumped the evening before the big gap, suggesting retail attention arrived just as institutional momentum was building.

The Backlog Tells the Real Story

As far as the numbers go, that drove this giant increase, full-year revenue reached $308 million, with Defense and Intelligence demand surging 50% year-over-year as governments worldwide scrambled for sovereign space capabilities. CEO Will Marshall framed it plainly: “Just as satellite services were transformative last year, we expect AI to be transformative this year, enabling us to unlock massive markets even faster.”

Overall, fiscal 2027 revenue guidance is $415 million to $440 million, representing 35% to 43% growth, and this guidance is now backstopped by a backlog that exceeds the company’s entire annual revenue. The catch: Planet intentionally pivoted toward large government and enterprise deals, resulting in a declining customer count but higher revenue per customer, and is discontinuing the customer count metric entirely.

Reddit Wakes Up to the “Underlooked Space Stock”

Sentiment on r/stocks spiked to 82 (Very Bullish) on the evening of March 19, driven by a post from user currysoup19: “While everyone was chasing the $RKLB and $ASTS pumps, Planet Labs just dropped a monster Q4 report and the market is finally waking up.”

Planet Labs surges to new AH after earnings? Perhaps the underlooked space stock?

by u/currysoup19 in stocks

The bullish case centers on three developments:

- Planet Labs posted a non-GAAP EPS of zero in Q4, beating analyst estimates of negative 5 cents, marking the first quarter in which the company did not lose money on an adjusted per-share basis, and the first full fiscal year of positive free cash flow and adjusted EBITDA profitability.

- Planet Labs carries $640.1 million in cash with no near-term need for dilution, in contrast to peers still burning through equity raises.

- A partnership with NVIDIA to build what the Reddit post called “the first GPU-native AI engine for planetary data,” adding an AI infrastructure angle to the satellite services business.

Defense Concentration Is the Question Investors Can’t Ignore

A 50% surge in Defense and Intelligence revenue is powering growth, but it could also deepen reliance on government budgets with termination-for-convenience clauses. Management’s answer is believed to be AI: fiscal 2027 is positioned as the “year of AI,” with investments expected to unlock commercial markets in insurance and energy. Whether that commercial pivot materializes separates a durable growth story from a defense contractor with a satellite fleet. While the current consensus price target of $24.71 is roughly 27% below today’s market price of $33.94, the gap likely indicates the street’s rapid decalibration. This valuation disconnect suggests that investors are now pricing in the ‘AI pivot’ as a near-term certainty rather than a long-term goal, effectively treating Planet as a high-margin platform months before the fiscal 2027 ‘Year of AI’ revenue actually hits the ledger.