Monthly income from a fund blending senior loans, high-yield corporate bonds, and CLO debt tranches sounds appealing, but the real question is whether SPDR Blackstone High Income ETF (NYSEARCA:HYBL) earns its place in a portfolio or charges more for what cheaper alternatives already do.

What HYBL Is Actually Trying to Do

HYBL is an actively managed ETF built around a specific income problem: most high-yield bond funds carry meaningful interest rate sensitivity, which punishes investors when rates rise. HYBL attempts to solve this by combining senior loans, high-yield corporate bonds, and debt tranches from U.S. collateralized loan obligations (CLOs). The result is a portfolio with lower duration and lower volatility compared to traditional high-yield funds, while still targeting high current income with monthly distributions.

Senior loans are floating-rate instruments whose coupons reset as benchmark rates move. That floating-rate exposure is the core mechanism keeping HYBL’s duration low. CLO debt tranches add structured credit exposure, offering yield pickup above plain corporate bonds in exchange for complexity. Together, these three asset classes are meant to deliver income that holds up across rate environments rather than collapsing when the Fed moves.

The Yield Looks Compelling in This Rate Environment

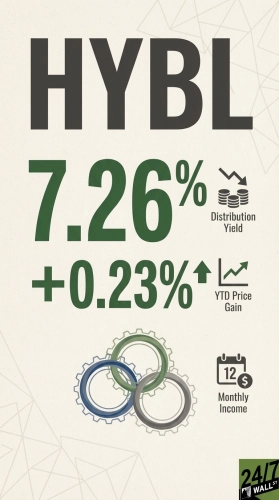

With the Fed Funds Rate at 3.75% and the 10-year Treasury yielding around 4.3%, HYBL’s 7.2% yield offers a meaningful spread above risk-free rates. The fund’s dividend yield from ETF profile data sits at 6.58%, with analyst-cited figures ranging from 7.2% to 7.7% depending on the measurement period. The income premium over Treasuries is real.

The yield curve is also constructive. A 10Y-2Y spread of 0.5% signals a normal, positively-sloped curve with no recession warning. That matters for high-yield credit: spread compression tends to characterize this kind of environment, reducing pressure on leveraged borrowers. The Fed has cut rates 75 basis points over the past 12 months, which typically supports credit quality and reduces default pressure on leveraged borrowers.

Does the Performance Back the Promise?

HYBL has delivered 6% price appreciation over one year and 24% since its February 2022 inception. Its passive peer, iShares iBoxx High Yield Corporate Bond ETF (NYSEARCA:HYG | HYG Price Prediction), returned 7% over the same one-year period. On price return alone, HYBL trails slightly, though the gap is narrow. Year-to-date, HYBL is down less than 1% while HYG is essentially flat at up less than 1%.

Analyst commentary on Seeking Alpha noted that returns have been comparable to peers despite the higher expense ratio, which is a reasonable verdict. Active management has not destroyed value here, but it has not created a clear edge either.

The Tradeoffs Worth Understanding

- Cost drag is real: HYBL carries a 0.70% expense ratio, which is higher than the category average. The fund’s own ETF profile data shows a net expense ratio of 0.007, which conflicts with analyst-cited figures and likely reflects a data error. The 0.70% figure from multiple independent analyst sources is the more credible number. Over time, that fee compounds against income.

- CLO complexity adds opacity: CLO debt tranches are not straightforward instruments. Their performance depends on the underlying loan pools, tranche seniority, and structured waterfall mechanics. In a stress scenario, like a recent VIX spike to around 31, CLO tranches can reprice sharply even when underlying credit quality holds.

- Short track record limits conviction: HYBL launched in February 2022, meaning it has never been tested through a full credit cycle. One analyst flagged this directly, noting that short historical data makes assessing long-term risk management challenging. Four years of history is not enough to judge how Blackstone’s active management performs in a genuine credit downturn.

HYBL makes the most sense as an income sleeve for investors who want monthly cash flow, can tolerate credit risk, and value the lower duration profile from floating-rate loan and CLO exposure. Anyone expecting it to outperform a passive high-yield index on total return should weigh the 0.70% fee against a track record that, so far, only matches rather than beats cheaper alternatives.