America’s electrical grid is being asked to power something it was never designed for: the AI revolution. Data centers, EV charging networks, and industrial reshoring are colliding with decades of underinvestment in grid infrastructure, creating a structural demand surge that has reshaped how investors think about utilities, industrials, and power equipment. Tema Electrification ETF (NASDAQ:VOLT) was built specifically around that collision.

What VOLT Is Actually Trying to Do

VOLT is an actively managed ETF that launched December 3, 2024, with a mandate to capture the full electrification value chain: generation, transmission, grid equipment, and the utilities absorbing the load. The thesis is not that electricity demand will grow modestly. The U.S. is entering a structural demand inflection driven by AI data centers, electric vehicles, and manufacturing reshoring, with aging coal, oil, and nuclear power infrastructure requiring replacement at the same time demand is accelerating.

The fund holds approximately 29 stocks, a concentrated lineup by ETF standards. The top 10 positions account for roughly 49% of total assets, with Bel Fuse at 6.61%, Powell Industries at 6.52%, NextEra Energy at 6.35%, Quanta Services at 4.92%, and American Electric Power at 4.73% rounding out the largest weights.

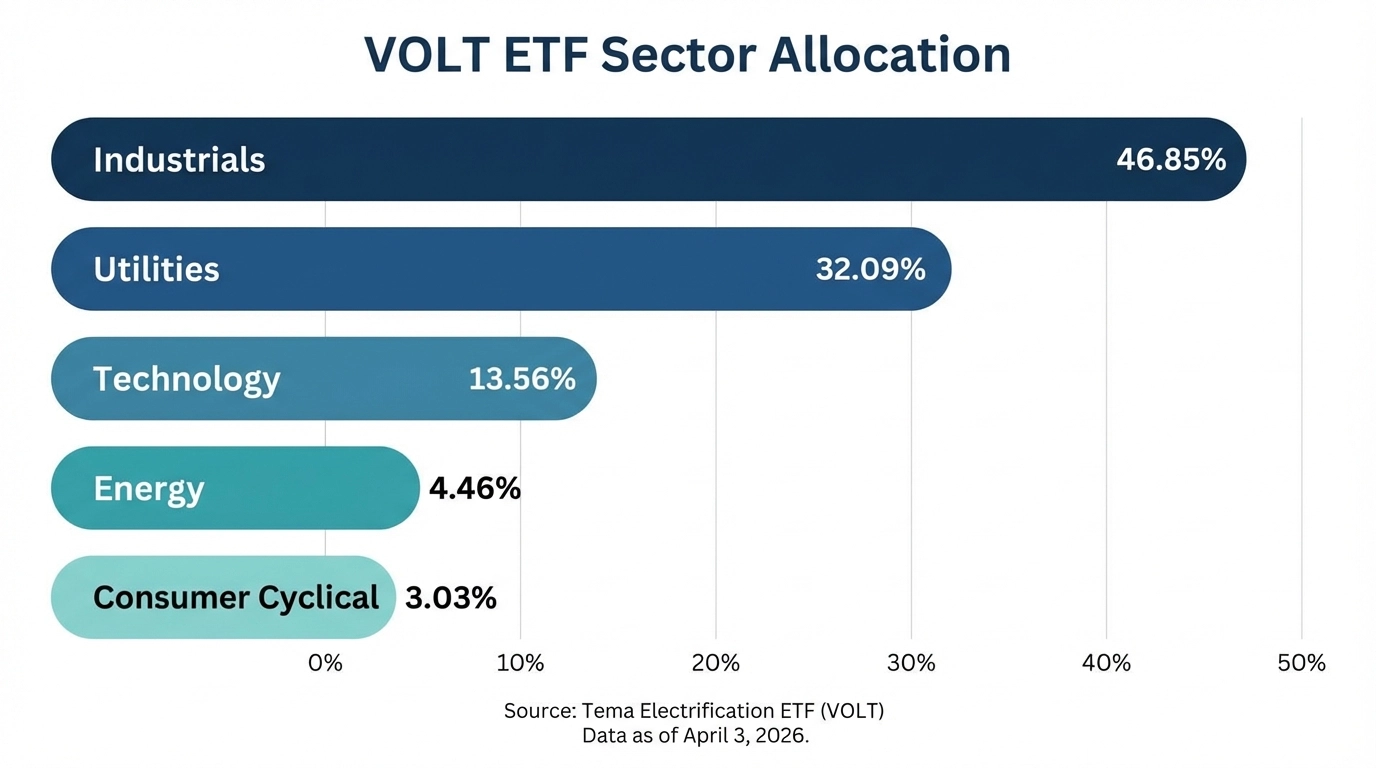

The sector composition deliberately overweights the infrastructure layer rather than pure-play utilities. Industrials make up nearly 47% of the portfolio, utilities roughly 32%, and technology about 14%. Companies wiring the grid, building switchgear, and laying transmission lines often have more direct earnings leverage to the buildout cycle than the utilities themselves.

The Earnings Case for Grid Infrastructure

VOLT’s return engine is the fundamental earnings growth of companies that build and maintain electrical infrastructure at a moment when demand is outpacing supply. The American Society of Civil Engineers rated U.S. energy infrastructure a D+ in its 2025 report card, down from a C- four years prior, reflecting decades of deferred investment now colliding with surging commercial electricity demand.

WTI crude oil recently spiked to nearly $91 per barrel, a level not seen since the 2022 energy crisis, reinforcing the economic argument for electrification as a hedge against fossil fuel price volatility. expanded demand from EVs and AI data centers continues to translate into capital spending commitments from the largest technology companies in the world.

VOLT is up roughly 20% year to date and has gained about 60% over the past year. Tema’s own marketing highlights a forecast that U.S. electricity demand could rise 78% by 2050 relative to a 2023 baseline.

A Strong Start, but a Short Track Record

VOLT has delivered on its premise so far, but it is a young fund. It launched in December 2024, meaning its strong one-year return reflects genuine sector tailwinds rather than a full market cycle. Investors have raised this point directly, noting that the fund’s concentration raises a question about whether it broadens exposure or amplifies it.

That concern is legitimate. VOLT is a high-conviction sector bet, not a diversifier. Its 0.75% expense ratio is above its category average, a cost that only makes sense if active management consistently identifies the right companies within the electrification chain. For comparison, a broader utility ETF like the First Trust NASDAQ Clean Edge Smart Grid Infrastructure Index Fund (NASDAQ:GRID) charges 0.56% and returned 44% over the past year. VOLT’s 60% one-year gain is meaningfully higher, suggesting active management has added value in this environment, though one year is too short a window to declare victory.

Three Tradeoffs Investors Need to Understand

- Concentration risk is real and intentional. With roughly 29 holdings and nearly half the portfolio in the top 10 names, a single earnings disappointment from a Powell Industries or a regulatory setback for NextEra Energy can move the fund materially. VOLT behaves more like a focused stock portfolio than a diversified ETF, and investors should size it accordingly.

- Regulatory and infrastructure risk cuts both ways. Regulatory and infrastructure risk is embedded in the thesis. The same permitting bottlenecks and grid interconnection queues that create the investment opportunity can also delay project timelines and compress near-term earnings, even if long-term demand projections remain intact.

- The expense ratio requires active management to keep earning its keep. At 0.75%, investors are paying for stock selection. In a rising-tide environment, a passive alternative may capture most of the return at lower cost. The premium is only justified if the manager continues tilting toward the highest-earnings-leverage names within the theme.

VOLT is a focused, actively managed bet on the structural electrification of the U.S. economy, best suited as a satellite position for growth-oriented investors who want direct exposure to the grid buildout cycle. Anyone expecting it to smooth portfolio volatility or generate meaningful income should look elsewhere.