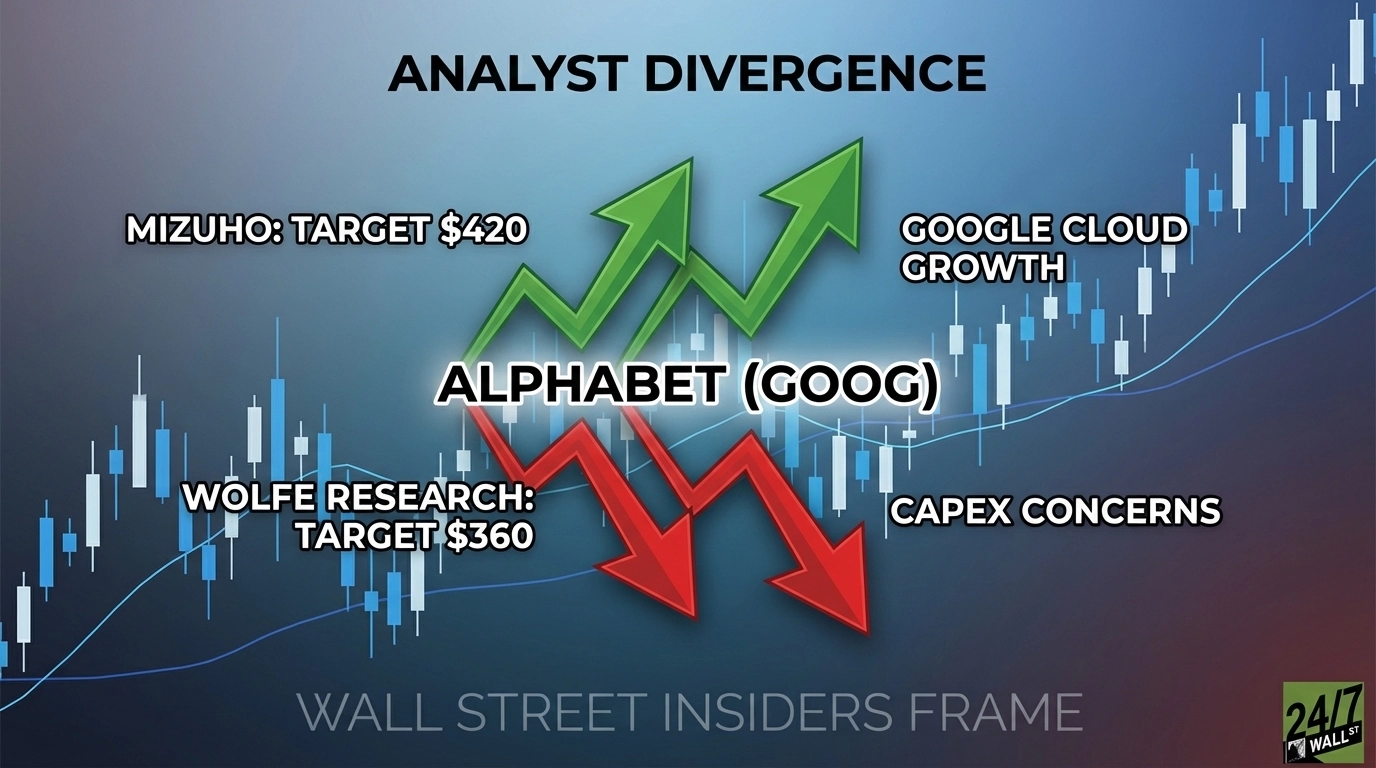

Alphabet (NASDAQ:GOOG | GOOG Price Prediction) is drawing sharply divergent calls from two respected Wall Street firms, even as both maintain bullish ratings. Wolfe Research trimmed its price target to $360 from $390, while Mizuho lifted its target to $420 from $410. Both held Outperform ratings, leaving investors with a $60 gap between two confident but divided views.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| GOOG | Alphabet | Wolfe Research | Price Target Cut | Outperform | Outperform | $390 | $360 |

| GOOG | Alphabet | Mizuho | Price Target Raised | Outperform | Outperform | $410 | $420 |

The Analyst’s Case

Mizuho analyst Lloyd Walmsley raised his price target citing Alphabet’s partnership with Anthropic and improved backlog trends as catalysts for stronger growth. Walmsley argues Wall Street is too conservative on Google Cloud, projecting cloud revenue could reach $149 billion by 2027, well above consensus. He flagged upside from TPU-related revenue with more favorable economics and stronger margins from Google Cloud than currently modeled.

Wolfe Research cut its price target by $30 while maintaining its Outperform rating. This reflects a more cautious view on near-term valuation headroom despite acknowledging underlying business momentum.

Company Snapshot

Alphabet closed fiscal 2025 crossing $400 billion in annual revenue for the first time, with full-year revenue of $402.84 billion, up 15.09% year over year. Q4 FY2025 delivered EPS of $2.82 against a $2.63 estimate and revenue of $113.83 billion, beating the $111.35 billion consensus by 2.23%. Google Cloud grew 48% year over year to $17.66 billion, with segment operating income more than doubling to $5.31 billion. Google Search remained durable at $63.07 billion, up 17%. The Gemini App scaled to 750 million-plus monthly active users, with Gemini models processing more than 10 billion tokens per minute.

Why the Move Matters Now

Alphabet trades at $315.72, below both targets, with a trailing P/E of 29x and forward P/E of 23x. The stock gained 7.22% over the past week after volatility, though it remains up just 0.68% year to date. The 52-week range of $147.89 to $349.90 illustrates the wide band of sentiment.

The central tension is capital allocation. Management guided for $175 billion to $185 billion in 2026 capital expenditures, a dramatic escalation from $91.45 billion in full-year 2025 CapEx. CEO Sundar Pichai stated: “We’re seeing our AI investments and infrastructure drive revenue and growth across the board. To meet customer demand and capitalize on the growing opportunities we have ahead of us, our 2026 CapEx investments are anticipated to be in the range of $175 to $185 billion.”

Bulls like Mizuho see this as the right bet on Cloud at a $70 billion-plus annual run rate. Bears point to full-year 2025 free cash flow of $73.27 billion, essentially flat year over year despite the CapEx surge as evidence returns have yet to materialize at scale.

The broader analyst community leans constructive: 62 analysts carry Buy ratings with zero Sell ratings, with a consensus price target at $359.53.

What It Means for Investors

The divergence between Wolfe’s $360 target and Mizuho’s $420 target reflects a genuine fork in the road: whether Alphabet’s AI infrastructure spending translates into Cloud margin expansion at Mizuho’s pace, or whether execution risk and valuation pressure cap near-term gains as Wolfe implies. Both firms remain bullish. The debate is timing and magnitude, not direction. Google Cloud growth rates and free cash flow trends are the key metrics to watch as the CapEx cycle matures.