Software stocks have sold off so rapidly that many on Wall Street are calling this a “SaaSpocalypse”. Snowflake (NYSE:SNOW | SNOW Price Prediction) has also been a victim, but it has been beaten down to the point where it’s time to start loading up. This company was the “next big thing” in cloud computing 4 years ago, before it declined significantly and has been treading water since.

It then went on a brief 150% rally from 2024 lows to October 2025 highs before reversing course and falling all the way back to prices SNOW stock stayed rangebound at for years.

Again, this is just one out of dozens of software stocks that are sitting at aggressive discounts today. What makes Snowflake special is that its growth rate estimates remain high, plus the $44 billion market cap can lead to massive upside potential down the line. Let’s take a look at the ins and outs of this company.

What Snowflake does

Snowflake was built on the idea that enterprises should be able to store data without being locked into any single cloud provider, as large companies had significant trouble managing data. Snowflake’s answer was to separate compute from storage, meaning you only pay for what you actually use, and you can scale each independently. The platform runs simultaneously on AWS, Microsoft Azure, and Google Cloud, so customers are never beholden to one vendor.

Companies are still struggling with managing a large amount of data, so the thesis itself hasn’t changed since Snowflake’s founding. The main issue with the business is that the market has consistently taken things too far in either direction.

Why SNOW stock fell again

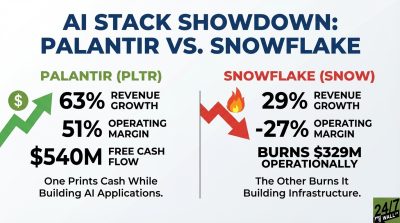

What happened after 2025 is very similar to what happened in 2022. Back in 2022, the market pushed SNOW stock to euphoric levels before growth started to moderate and hold stable instead of accelerating. And in 2025, the euphoria went too far yet again. Snowflake’s Q4 FY2026 report showed revenue beating estimates by 2.3%, along with an 8.6% beat on EPS. The stock still fell because investors wanted to see an acceleration.

Revenue growth also slipped a little, but we’re looking at 30% year-over-year, which is nothing to scoff at.

| Date | Snowflake Inc (SNOW) Revenue with Estimate (in millions) |

|---|---|

| 2029-01-28 | 8896.35 |

| 2028-01-28 | 7283.93 |

| 2027-01-28 | 5903.85 |

| 2026-01-28 | 4683.95 |

| 2025-01-28 | 3626.40 |

| 2024-01-28 | 2806.49 |

| 2023-01-28 | 2065.66 |

| 2022-01-28 | 1219.33 |

| 2021-01-28 | 592.05 |

| 2020-01-28 | 264.75 |

| 2019-01-28 | 96.67 |

Still, there’s the fear that if autonomous AI agents from OpenAI, Anthropic, and others can increasingly act on data rather than just query it, the traditional SaaS and data warehousing model loses pricing power.

Snowflake itself has in-house AI models to counteract this “threat,” but I don’t think it will ever lose significant pricing power from AI. A research paper showed that AI models succeed on 8-17% of tasks when operating by themselves against enterprise databases.

I see a recovery, albeit not an explosive one

The whole SaaS sector is likely to have a lid over it as long as the market sees AI as a threat. I’d argue Snowflake isn’t even a SaaS company. Software-as-a-service companies depend on the number of subscriptions to their platform, either on a monthly or yearly basis. Snowflake’s financials depend on the amount of compute being consumed, so it can keep growing even if it loses users. Also, the company added a record 740 net new customers in Q4, up 40% year-over-year.

Snowflake’s growth is simply too fast to ignore, and the stock trades at a very low multiple compared to historical prices. Price-to-FCF is at less than 40x, whereas it has historically traded at over 90x FCF.

Analysts have an average price target of $237.7, which means you’d be paying ~72x free cash flow. The FCF margin has actually been rising, so I’d estimate you’re paying less than 20x FCF two years out.

If the FCF premium holds, you’re looking at 30% annualized gains in the coming years. If the market is willing to pay that estimated 72x FCF premium, we might be in for a triple-digit rally like the one that started in 2024.

There is plenty of cloud computing demand to go around, so I do not think the bear case will win out in the end. My base case is that SNOW stock ends the year above $200.