ServiceNow (NYSE: NOW | NOW Price Prediction) and Shopify (NASDAQ: SHOP) are both high-multiple technology names, but which one carries the more compelling short thesis right now? The answer, based on valuation, earnings quality, and price behavior, favors Shopify as the more exposed name.

Valuation: Shopify Is More Exposed

Shopify trades at a significant premium on a price-to-sales basis. With a current price of $127.41 and FY2025 revenue of $11.556 billion, the implied price-to-sales multiple sits near 14x sales. ServiceNow, with FY2025 revenue of $13.278 billion and a current price of $94.19, trades closer to 7x trailing sales. That gap is meaningful.

On earnings multiples, the contrast sharpens further. Shopify carries an implied P/E of 88x. ServiceNow trades at a trailing P/E of 53x, with a forward P/E near 21x and a PEG ratio of 0.842, suggesting the market is not pricing in excessive optimism relative to growth. Shopify’s valuation demands sustained execution with no margin for error.

Winner: ServiceNow is less stretched; Shopify is more vulnerable on valuation.

Earnings Quality: Shopify’s Unreliable GAAP Story

Shopify posted FY2025 GAAP net income of $1.231 billion, down 39.03% year over year, driven by equity investment mark-to-market swings rather than operational deterioration. That volatility cuts both ways. In Q1 2025, equity investment losses of $908 million drove net income to negative $682 million. In Q2 2025, equity investment gains of $568 million pushed net income to $906 million. The GAAP earnings line is essentially noise, making valuation anchoring nearly impossible for short sellers seeking a fundamental catalyst.

ServiceNow’s earnings picture is far cleaner. FY2025 GAAP net income grew 22.67% year over year to $1.748 billion. Q4 2025 EPS of $0.92 beat the $0.89 consensus estimate. Full-year EPS of $3.51 beat the $3.412 estimate. Consistent GAAP profitability with predictable beat patterns positions ServiceNow as a fundamentally resilient name, not a short candidate.

Winner: Shopify’s earnings volatility makes it the weaker fundamental story and the more attractive short on this dimension.

Price Behavior and Risk: Shopify Has Corrected Less

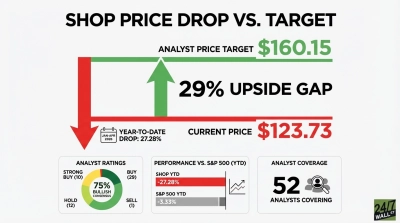

ServiceNow has already absorbed a severe de-rating. The stock is down 38.5% year to date and 42.3% lower than a year ago. Its 52-week high was $211.48, and it now trades near $94.19, closer to its 52-week low of $81.24. Shorting a stock that has already fallen more than 40% from its highs, with 42 analyst Buy ratings against just one Sell and a consensus target of $174.51, carries substantial squeeze risk.

Shopify is down 20.9% year to date but has bounced 6.1% over the past week. Its beta of 2.822 signals extreme volatility, which cuts against short sellers who need controlled drawdown risk. Still, the stock carries 12 analyst Holds and one Sell against its coverage, a notably softer consensus than ServiceNow’s near-unanimous bullish positioning. Shopify’s 52-week range of $80.35 to $182.19 reflects how wide the dispersion of outcomes remains.

Winner: ServiceNow’s extreme correction reduces remaining short opportunity; Shopify retains more downside potential from current levels.

Verdict

Shopify is the stronger short candidate. Its valuation at roughly 14x sales and an implied P/E of 88x demands near-perfect execution in an environment where tariff exposure and consumer spending sensitivity represent real headwinds. GAAP earnings are structurally unreliable due to equity investment volatility, leaving the market with no clean anchor for fair value.

ServiceNow, despite its own risks from federal budget tightening and M&A integration complexity, has already repriced sharply, carries overwhelmingly bullish analyst coverage, and generates $4.576 billion in annual free cash flow with a guided 36% FCF margin for FY2026. Shorting ServiceNow here means fighting the tape, the analysts, and the fundamentals simultaneously. Shopify offers a cleaner thesis with more valuation room to compress.