The Motley Fool Money podcast panel spent a recent episode pushing back on the narrative that AI is about to gut enterprise software demand. The debate was sparked by ServiceNow (NYSE:NOW | NOW Price Prediction), which sank 14% following earnings despite beating expectations and raising guidance.

ServiceNow’s Beat-and-Raise Quarter That Got Punished

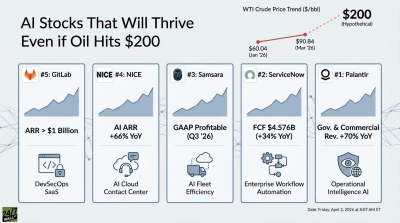

The panel framed the reaction as disconnected from reality. As the host put it, “Were things really that bad from ServiceNow that we need to sell off?” Software stocks broadly fell 5% to 10%, with some now trading at P/E multiples of just 10-12. On the numbers, the answer looks clear. ServiceNow reported Q4 FY2025 EPS of $0.92 versus $0.89 expected on revenue of $3.57 billion, up 20.66% year over year. cRPO grew 25%, and Now Assist net new ACV more than doubled. Management also guided FY2026 subscription revenue to $15.53 to $15.57 billion with a 32% non-GAAP operating margin.

CEO Bill McDermott told investors there is “no AI company in the enterprise better positioned for sustainable profitable revenue growth than ServiceNow.” Despite that, the stock has been punished. Shares are down 41.97% year to date and 52.86% over the past year, closing at $88.89 on April 29.

The Reality Check

The panel’s strongest pushback came from real-world demand signals. A caller relayed feedback from a CEO who said, “flat out nothing has changed in their software purchasing habits due to AI.” Instead, the panel argued that companies like ServiceNow are likely beneficiaries of AI rather than victims. Using Jensen Huang’s 5-layer cake analogy for AI infrastructure, they positioned ServiceNow higher up the stack, where software orchestrates and monetizes AI capabilities. The company’s own metrics support that view. ServiceNow closed 244 deals over $1 million in net new ACV, up nearly 40% year over year, and now has 603 customers generating more than $5 million in ACV. Those are not signs of weakening demand.

The Intel Parallel

To highlight the disconnect, the panel pointed to a very different reaction elsewhere in tech. The panel turned to Intel (NASDAQ:INTC) as a valuation mirror image. They praised a “very respectable quarter”, with the foundry business growing 16% and a shift from GPUs to CPUs creating opportunity. Intel’s Q1 FY2026 backed that up: revenue of $13.58 billion, Data Center and AI up 22% YoY, and CEO Lip-Bu Tan citing “significantly increasing” demand for CPUs and advanced packaging.

The reaction to the company’s earnings could not have been more different. Intel shares jumped 45.17% in a single week and are up 365.83% over the past year, even as some investors warn the stock is approaching peak-cycle valuations at over 100x forward earnings.

Bottom Line

Until there is real concrete evidence of AI replacing enterprise software spend, the SaaSpocalypse label looks overblown. With ServiceNow generating $2 billion of free cash flow at a 57% Q4 FCF margin, the gap between fundamentals and the stock price is the story worth watching.