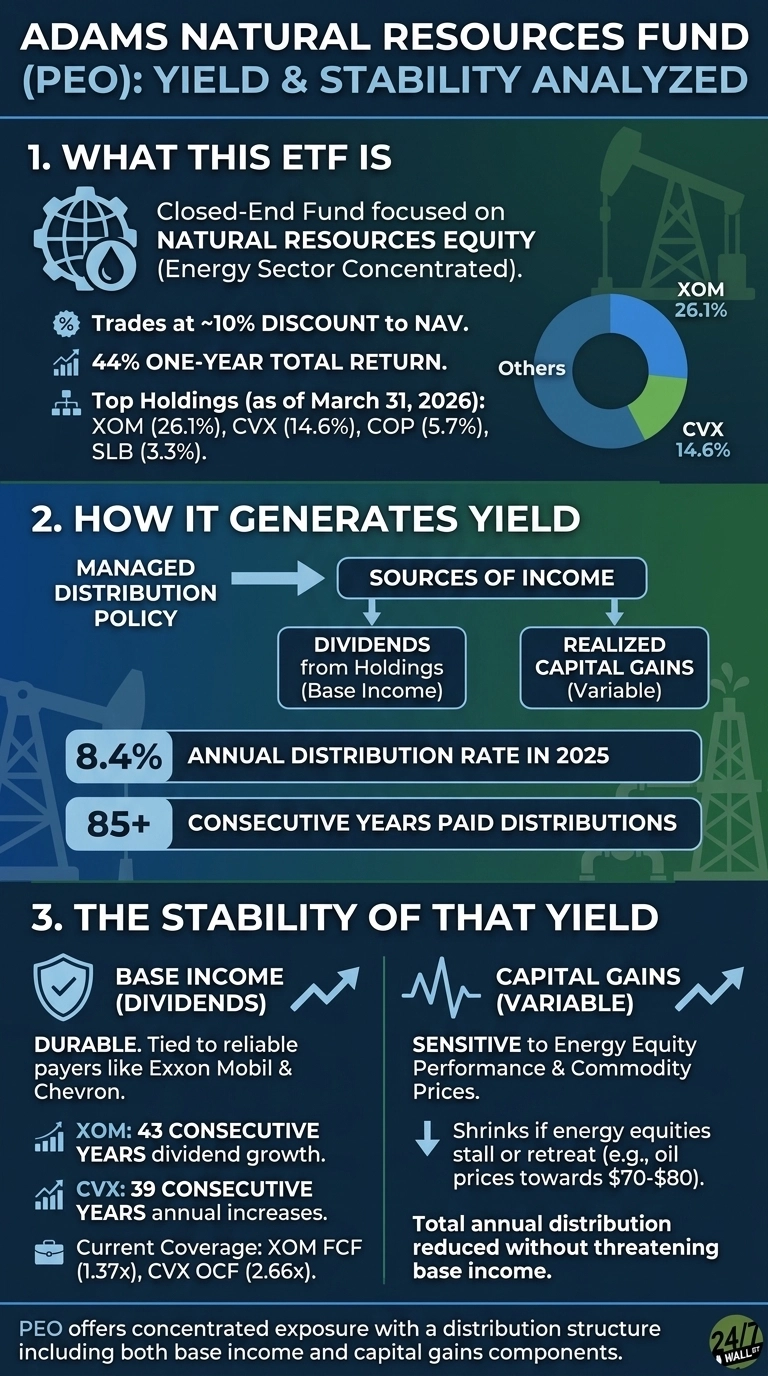

Adams Natural Resources Fund (NYSE:PEO) trades at a roughly 10% discount to its net asset value and has delivered a 27% one-year total return. The fund’s 8% trailing yield based on its $2.05 per share in 2025 distributions attracts income-focused investors, though that yield carries real commodity risk.

How PEO Generates Income

PEO is a closed-end fund that has paid distributions for more than 85 consecutive years. Income comes from dividends on underlying holdings and realized capital gains from portfolio activity. The fund uses a Managed Distribution Policy, a structured approach where distributions are set as a fixed percentage of NAV rather than tied directly to income earned, targeting a 2% quarterly distribution rate based on average net asset value, which produced an 8.4% annual distribution rate in 2025.

The portfolio is heavily concentrated. As of March 31, 2026, the top two positions represented 40.7% of net assets: Exxon Mobil (NYSE:XOM | XOM Price Prediction) at 26.1% and Chevron (NYSE:CVX) at 14.6%. ConocoPhillips (NYSE:COP) contributes 5.7%, and SLB (NYSE:SLB) adds 3.3%. The top ten holdings account for 67.7% of net assets.

Dividend Safety by Position

| Holding | Weight | Earnings Payout Ratio | FCF Payout Ratio | FCF Coverage |

|---|---|---|---|---|

| Exxon Mobil (XOM) | 26.1% | ~60% | ~100% | 1.0x |

| Chevron (CVX) | 14.6% | ~75% | ~100% | 1.3x |

| ConocoPhillips (COP) | 5.7% | ~50% | N/A | N/A |

| SLB | 3.3% | ~49% | N/A | N/A |

Exxon remains the fund’s most influential income driver. The company extended its 43‑year dividend growth streak with a quarterly payout of $1.03. The earnings payout ratio sits near 60%, which is reasonable, but free cash flow tightened materially in 2025 as operating cash flow softened and capital spending increased. Exxon generated roughly $11 billion of FCF in the second half of 2025 against more than $17 billion in annual dividends, placing the FCF payout ratio above 100% and pushing coverage below 1×. The cushion is thinner than in 2022, when higher commodity prices supported far stronger cash generation.

Chevron’s profile is steadier but still pressured. Lower commodity realizations pulled full‑year earnings down, lifting the earnings payout ratio into the 70–80% range. Free cash flow also contracted, and dividend payments exceeded full‑year FCF, resulting in a payout ratio above 100%. Even so, Chevron maintained a positive cash‑flow buffer, with operating cash flow covering dividends by roughly 1.3×. The company raised its quarterly dividend to $1.78 in early 2026, extending a 39‑year streak that underscores management’s commitment to the payout.

ConocoPhillips and SLB carry smaller weights and more moderate payout profiles. COP’s Q4 2025 adjusted EPS of $1.02 reflected softer pricing, but the company’s long‑standing framework of returning 45% of cash from operations to shareholders provides a structural anchor for distributions. SLB reported lower full‑year earnings, but its Q4 2025 free cash flow remained strong and comfortably covered its dividend, supporting the stability of its smaller contribution to the fund’s income stream.

Oil Prices and Distribution Risk

Oil has been moving around a lot. After sliding into the mid‑fifties late last year, WTI rebounded sharply in early 2026 before settling back toward the hundred‑dollar range. The exact highs and lows matter less than the overall pattern. When crude swings this much, cash flow among the major producers tends to follow suit. A meaningful pullback would show up across the entire sector at the same time.

This is important because PEO’s capital gains distributions respond much more directly to commodity prices than its base income. Those gains have grown over the past few years as energy stocks rallied, but they can shrink quickly if the sector loses momentum. Even if Exxon and Chevron keep their dividends steady, the capital gains portion of PEO’s payout can contract when oil prices soften.

Total Return Context

PEO has delivered strong total returns. The share price has climbed over the past year, and the fund’s largest holdings have also posted solid gains during the broader energy rally. Investors have collected income while also benefiting from meaningful price appreciation.

Distribution Durability Depends on Which Component You’re Watching

The base income stream is the stable part of the story. Exxon and Chevron have protected their dividends through recessions, price crashes, and the 2020 collapse. Their current cash flow still supports those payouts, even though free cash flow is not as strong as it was during the peak years of the cycle.

The variable part is the capital gains distribution. That number moves with energy equity performance and with oil prices. A sustained pullback toward more moderate crude levels would likely reduce PEO’s total annual distribution, but it would not threaten the core dividend income.

PEO is essentially a concentrated energy equity fund with a two‑part distribution. The base income comes from dividends paid by companies like Exxon and Chevron. The capital gains portion rises and falls with the commodity cycle. Understanding which part you rely on makes the overall picture of the distribution much clearer.