Apple (NASDAQ: AAPL | AAPL Price Prediction) and Microsoft (NASDAQ: MSFT) just delivered holiday-quarter results that put two very different capital-return philosophies on display.

Apple leaned on the iPhone cycle and record services to print $143.76B in revenue. Microsoft leaned on Azure and a surging enterprise backlog. Both beat, both guided higher, and both reward shareholders. How they do it could not be more different.

iPhone Cycle Carries Apple. Azure And AI Carry Microsoft.

Apple posted a best-ever iPhone quarter at $85.27B, up 23.3%, with Tim Cook calling out “unprecedented demand” and all-time records across every geography.

Services hit an all-time high of $30.01B, up 14%. Greater China, a perennial worry, rebounded hard to $25.53B from $18.51B a year earlier. EPS of $2.84 beat the $2.67 estimate.

Microsoft’s story is backlog and buildout. Intelligent Cloud grew 29% to $32.91B, Azure accelerated 39%, and Microsoft Cloud crossed $50B for the first time. Commercial remaining performance obligations reached $625B, up 110% year over year, helped by OpenAI committing to $250B of incremental Azure purchases.

Satya Nadella framed it plainly: “We are only at the beginning phases of AI diffusion.” To feed that, capex exploded to $29.88B, up 89%. That is a serious infrastructure bet.

A Buyback Machine Vs. An AI Infrastructure Machine

| Lens | Apple | Microsoft |

| Core bet | Installed base of 2.5B devices + Services | Azure and Copilot diffusion |

| Quarterly capex | $2.37B | $29.88B |

| Cash returned last quarter | Buybacks $24.70B + dividend | $12.7B combined |

| 10-year stock return | 1,041% | 850% |

The headline promised a 900% figure, and that is where Apple quietly wins. A decade ago AAPL traded at $23.93 split-adjusted; it closed at $273.17. That is the compounding engine buybacks and the dividend combine to produce.

Microsoft’s dividend has climbed faster on a per-share basis, rising from $0.36 in early 2016 to $0.91 today, while Apple’s split-adjusted payout has roughly doubled to $0.26. Apple simply shrinks the share count faster, with $100B in fresh repurchase authorization on top.

What I Want To See Next Quarter

For Apple, I will be watching whether Services can hold 14% growth without iPhone 17 tailwinds, and whether the China rebound sticks.

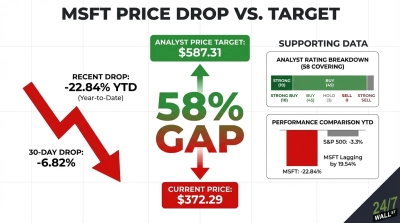

For Microsoft, the question is return on that capex. Azure guidance of 37 to 38% is healthy, but the 10.28% year-to-date drawdown tells me investors want proof the AI dollars convert. OpenAI investment losses of $3.1B last quarter are a reminder this is not free.

Why I Lean Apple For Compounders, Microsoft For Believers

If I am funding a long-hold account, Apple’s capital return story still feels durable to me. The 34 trailing P/E is rich, yet an installed base that large plus aggressive buybacks keeps compounding quiet and steady.

For a reader who believes AI workloads are in inning two, Microsoft at 26 trailing earnings with a $625B backlog is the more interesting setup, provided you can stomach capex swings. I would hesitate on both if tariff policy tightens further. Right now, I give Apple the edge on consistency, Microsoft the edge on upside.