I keep buying Broadcom (NASDAQ:AVGO | AVGO Price Prediction) and I am not going to pretend otherwise. Every paycheck, every rebalance, every time the stock pulls back, the buy button gets warm again. This is a position I am building for the next decade, and the receipts keep telling me to keep going.

The reason is simple in human terms before any spreadsheet opens. Hock Tan has turned this company into the silicon partner that the people building artificial intelligence cannot replace.

Custom AI accelerators, Ethernet AI switches, and the VMware software layer sitting between chips and workloads. When OpenAI joined the customer roster as the sixth name alongside Google, Anthropic, Meta and two others, my conviction stopped being a thesis and started being an inevitability I wanted to own shares of.

The Numbers That Keep Me Adding

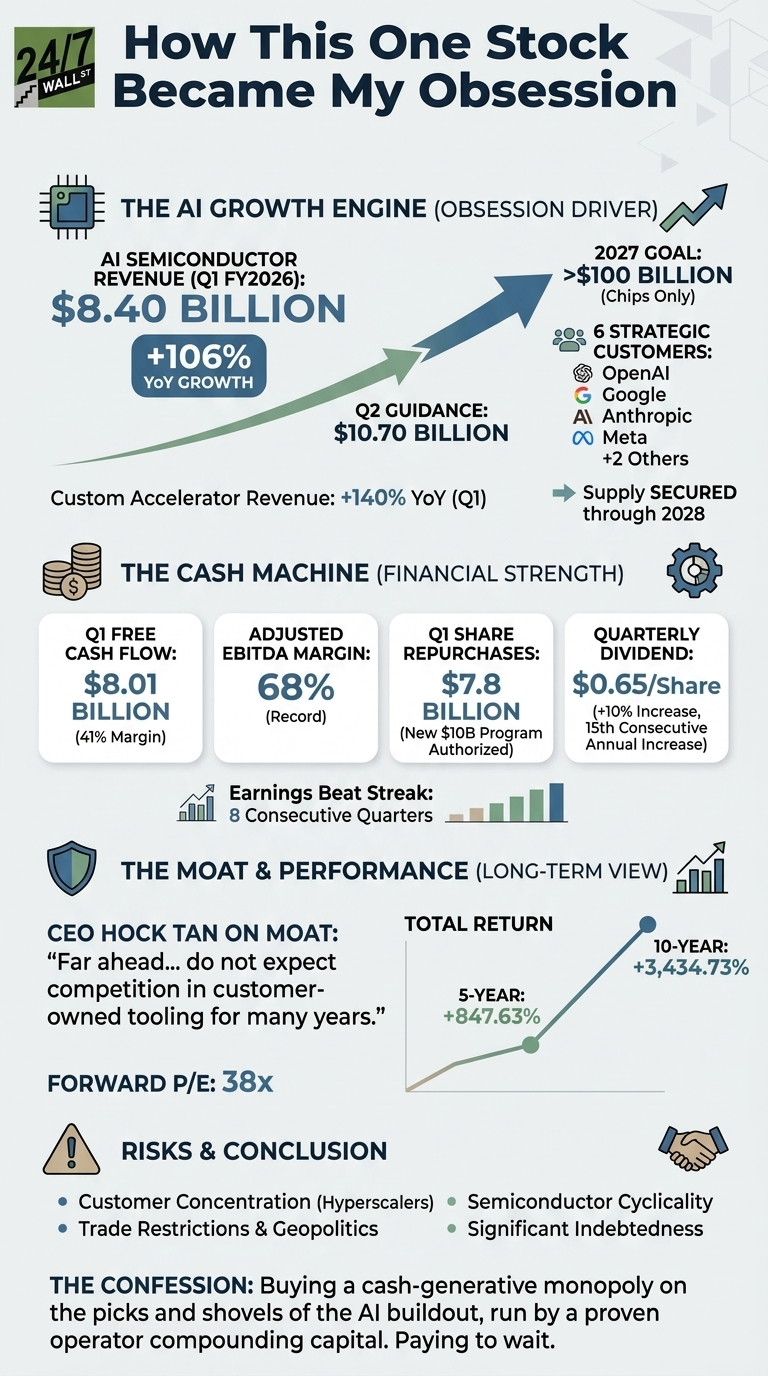

Start with what AI is actually doing to this business. AI semiconductor revenue hit $8.40 billion in Q1 fiscal 2026, up 106% year-over-year, and management guided Q2 AI revenue to $10.70 billion. Hock Tan told the Street he now has “line of sight to achieve AI revenue from chips, just chips, in excess of $100 billion in 2027” and that supply has been “fully secured” for 2026 through 2028.

Total Q1 revenue was $19.31 billion, a beat, and the company has now beaten earnings expectations in eight consecutive quarters. Then there is the cash machine underneath the AI story. Q1 free cash flow was $8 billion, representing 41% of revenue. Adjusted EBITDA margin printed a record 68%.

Full year fiscal 2025 operating cash flow was $27.54B. That cash is coming back to me. Broadcom repurchased $7.8 billion of stock in Q1 alone and authorized a new $10 billion repurchase program through December 31, 2026. The quarterly dividend was raised 10% to $0.65 per share, the fifteenth consecutive annual increase since fiscal 2011.

The third leg is the moat. Tan put it plainly: “you need a partner in silicon with the best technology, intellectual property, and execution capabilities. Modestly speaking, we believe we are far ahead in this regard, and we do not expect to see competition in customer-owned tooling for many years.”

Custom accelerator revenue grew 140% year-on-year in Q1. Anthropic alone is expected to demand in excess of 3 gigawatts of compute in 2027. That is a multi-year industrial commitment.

The Risk I Refuse to Wave Away

Customer concentration is real. A handful of hyperscalers drive most of the AI revenue, and any one of them blinking on capex would land hard. Layer in semiconductor cyclicality, trade restrictions, dependence on contract manufacturing, and significant indebtedness, and this carries real cyclical and balance-sheet risk. The forward multiple sits at 38x while trailing P/E reads 82x. Pay up and you wear it.

What keeps me buying anyway is that those six customers are now structurally embedded. Tan described the relationships as “deep, strategic, and multi-year” with insights stretching three to four years out. Concentration only kills you when the customer can leave. These customers cannot leave on a 12-month timeline without breaking their own roadmaps.

Why The Buy Button Stays Warm

The five-year total return on this stock is 847.63%. The ten-year is 3,434.73%. I missed most of that. But, I am not going to miss the next chapter, the one where AI silicon revenue scales from $10.7 billion in a single quarter toward $100 billion a year while the dividend keeps climbing and the buybacks keep shrinking the share count.

I am buying a cash-generative monopoly on the picks and shovels of the AI buildout, run by an operator who has compounded shareholder capital through three semiconductor cycles, and they are paying me to wait. That is the entire confession.