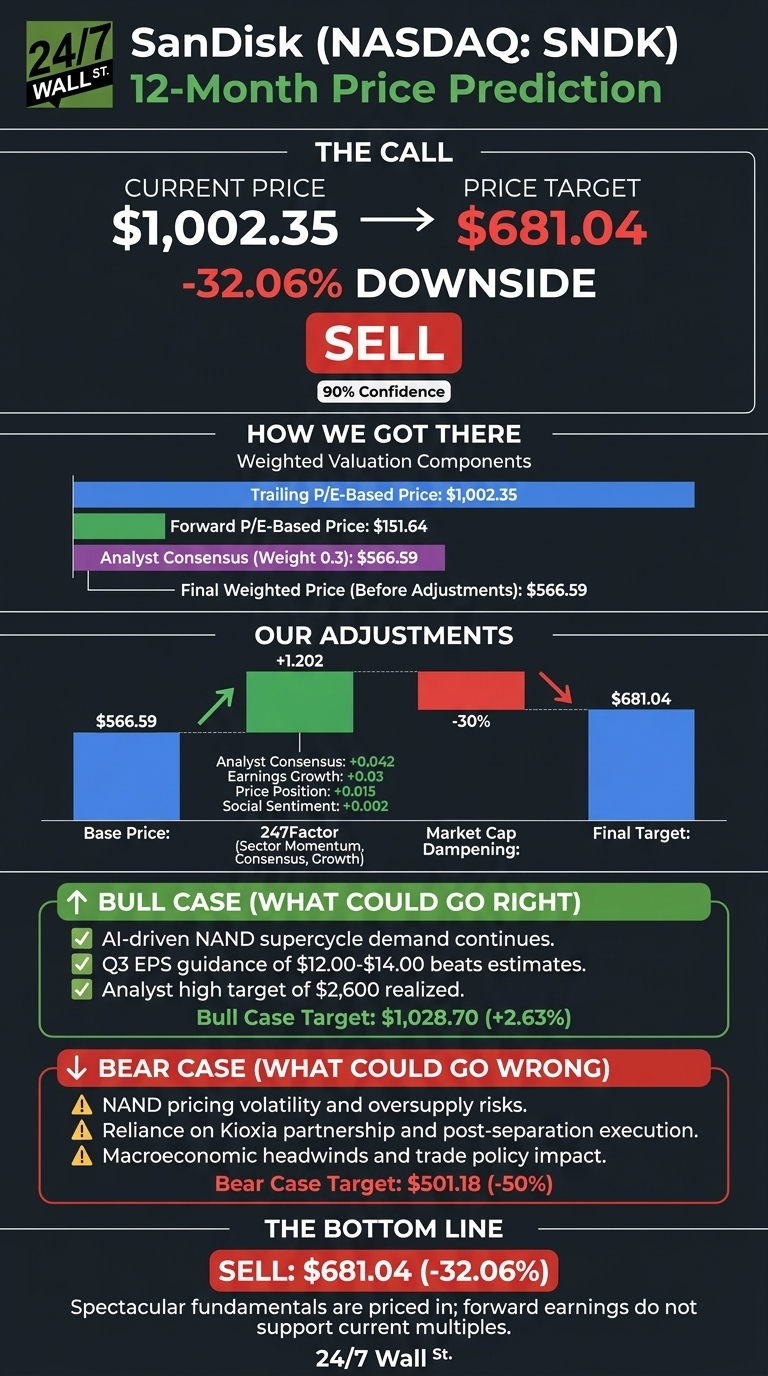

SanDisk (NASDAQ:SNDK | SNDK Price Prediction) has staged one of the most extraordinary rallies in semiconductor history, climbing 3,006% over the past year on the back of an AI-driven NAND supercycle. With shares now at $1,002.35, the question is whether the stock has front-run fundamentals.

Our 24/7 Wall St. price target for SanDisk is $681.04 over the next 12 months, implying 32.06% downside. Our recommendation is sell, with 90% model confidence. Spectacular fundamentals are already priced in, and forward earnings do not support current multiples.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $1,002.35 |

| 24/7 Wall St. Price Target | $681.04 |

| Upside/Downside | -32.06% |

| Recommendation | SELL |

| Confidence Level | 90% |

Why We Could Be Wrong

SanDisk is one of the most divisive stocks in the market. The structural NAND shortage, BiCS8 ramp, and High Bandwidth Flash collaboration with SK Hynix are real catalysts that could push earnings well above current models. Melius Research at $1,350 and Evercore ISI’s bull case at $2,600 argue the rally has further to run. Treat our price target as one datapoint.

A 3,000% Year and a Q3 Earnings Report That Looms Large

SNDK is up 10.94% over the past week, 62.76% over the past month, and 322.26% year to date, off a 52-week range of $31.01 to $1,070.66. NASDAQ-100 inclusion on April 20, 2026 added institutional bid, though shares fell 6.34% on April 28 ahead of earnings.

Q2 FY26, filed January 29, 2026, delivered strong results. Non-GAAP EPS came in at $6.20 versus $3.54 expected, a 74.97% beat. Revenue of $3.025 billion grew 61.3% YoY, with Datacenter up 76% YoY. Management guided Q3 revenue to $4.40B to $4.80B and EPS to $12.00 to $14.00. The Q3 report drops tomorrow.

The Case for $1,350 and Beyond

Q2 free cash flow exploded to $980 million, gross margin guidance for Q3 sits at 65% to 67%, and Q3 EPS guidance of $14 annualizes to roughly $56.

BofA Securities sees $1,080, Evercore ISI $1,200, GF Securities $1,277, and Bernstein $1,250. Polymarket traders price a 97.1% probability of an earnings beat. If Q3 results land at the high end and FY27 EPS approaches $50, a 25x multiple gets you to $1,250+.

What Could Go Wrong

The bear case starts with cyclicality. NAND has always been a commodity, and Wells Fargo’s Equal Weight rating with a $975 target reflects discomfort with premium multiples on potentially peak earnings. Western Digital’s planned divestiture of 7.5 million SNDK shares creates an overhang. A bear scenario lands at $501.18.

Bulls argue current trailing GAAP EPS of $7.49 is distorted by the $1.83 billion goodwill impairment taken in Q3 FY25, and forward P/E of 19 tells the real valuation story.

Where the Risk/Reward Stands

SanDisk is a great company at a stretched price. The 24/7 Wall St. price target is $681.04, recommendation sell, confidence 90%. The gap between trailing reality and forward expectation already embedded at $1,002 tips the scale. The bull case strengthens if Q3 EPS comes in above $14 and management raises FY27 outlook materially. The bear case takes hold if Q3 lands in line and NAND spot pricing rolls over.

Looking ahead, here is where our 24/7 Wall St. price target model projects SNDK could trade, assuming the AI memory cycle moderates as supply catches up post-2028.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $681.04 |

| 2027 | $640.00 |

| 2028 | $590.00 |

| 2029 | $545.00 |

| 2030 | $502.13 |

These projections assume SanDisk executes on BiCS8 and HBF while NAND pricing normalizes. Significant upside could come from sustained AI inference memory demand. Downside risk centers on a memory cycle reset post-2028.