Electric vehicle stocks have faced a bumpy road lately, with softening demand, tariff worries, and high interest rates testing even the strongest players. Investors wonder if newer entrants like Rivian can scale fast enough to compete against Tesla’s (NASDAQ:TSLA | TSLA Price Prediction) volume machine or Ford’s (NYSE:F) established truck network. Rivian’s (NASDAQ:RIVN) latest quarterly results offer a mixed bag that investors should examine closely, but act on carefully..

Better Than Expected, but Not Good Enough

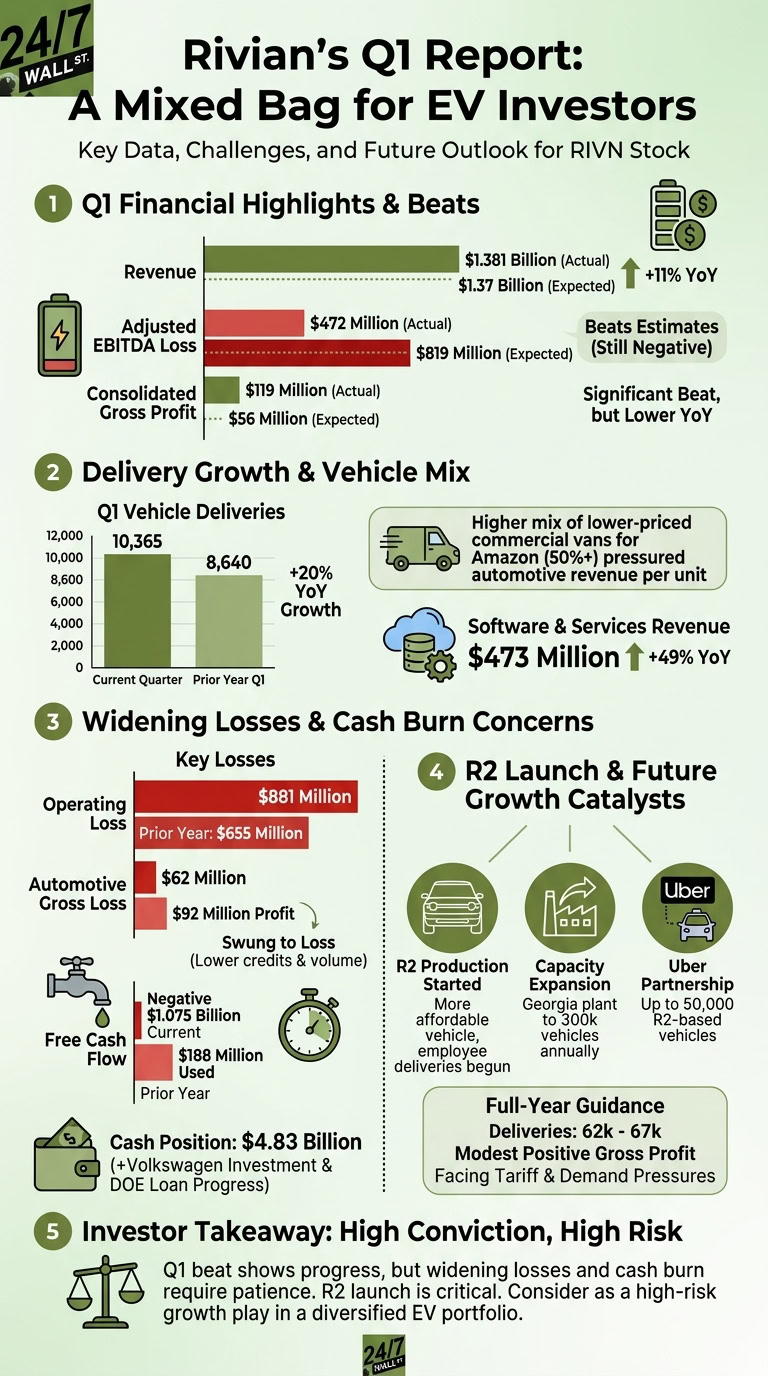

Rivian reported first-quarter results on Friday, posting revenue of $1.381 billion, up 11% from the year-ago quarter, slightly ahead of the roughly $1.37 billion Wall Street anticipated.

It delivered adjusted EBITDA losses of $472 million, producing negative adjusted margins of 34.2%, worse than the 26.5% generated last year. Still, that beat analysts’ expectations of around an $819 million loss. The company generated $119 million in consolidated gross profit — well above the $56 million analysts projected.

Vehicle deliveries also reached 10,365 units, a solid 20% increase from 8,640 in Q1 2025. This growth came despite a higher mix of lower-priced commercial vans for Amazon (NASDAQ:AMZN), which pressured automotive revenue per unit as they accounted for over half the deliveries in the quarter.

Rivian continues to perform better as a software and services stock, with revenue jumping 49% to $473 million, helping offset the automotive segment’s challenges.

Losses Still Widening in Key Areas

That said, let’s not sugarcoat it. While the operating loss widened from $655 million a year earlier, Rivian’s automotive gross profit of $92 million last year swung to a $62 million loss this time around, largely because regulatory credit sales dropped by $100 million and lower production volume. It was much improved from the $432 million lost in Q4, showing Rivian is getting costs under control.

Yet net cash used in operating activities hit $703 million, up sharply from $188 million last year. Free cash flow was negative $1.075 billion. Rivian ended the quarter with $4.83 billion in cash, cash equivalents, and short-term investments — bolstered by a $1 billion Volkswagen investment — plus additional liquidity, which gives it plenty of runway still. But cash burn remains a headline risk for a company still scaling up.

Compare that to peers: Tesla continues generating positive free cash flow at scale, while Ford’s F-150 Lightning benefits from a massive existing truck buyer base. Rivian’s R1T and R1S sit in the premium segment, where demand has proven more elastic.

The R2 Launch and Partnerships Offer Hope

Importantly, Rivian started production of its more affordable R2 vehicles. It began employee deliveries of the EV and expects external customer deliveries soon. It also raised is Georgia plant capacity to 300,000 vehicles annually and secured progress on a $4.5 billion Energy Dept. loan. It is putting all of its chips on the introduction of the lower cost R2 to help it swing to annual profits in the coming years.

The Uber Technologies (NYSE:UBER) robotaxi partnership for up to 50,000 R2-based vehicles adds another growth vector.

Full-year guidance held steady for 62,000 to 67,000 deliveries — up from 42,000 EVs in 2025 — and modest positive gross profit for the year. Management acknowledged persistent tariff and demand pressures but points to cost efficiencies and software margins as tailwinds.

Investors, though, looked past the headline beat and zeroed in on persistent challenges. Rivian stock, which had added modest gains after the release, ultimately closed down more than 8% on Friday. Soft demand, tariff woes, and high interest rates are testing even the strongest players. Investors wonder if newer entrants like Rivian can scale fast enough to compete.

In short, Rivian beat estimates on the top line, gross profit, and loss metrics this quarter. Deliveries grew nicely, and new initiatives like R2 position it for broader market reach. That said, widening operating losses, ongoing cash consumption, and reliance on commercial vans highlight the execution risks it faces in a competitive EV landscape.

Key Takeaway

Savvy investors should view Rivian as a high-conviction, high-risk growth story. The Q1 beat shows progress on gross profitability and delivery growth, but the trend in losses and burn rate requires patience — and close monitoring of whether the R2 can really make a meaningful impact.

Investors who believe the lower cost EV will gain traction, might consider taking a position as part of a diversified EV portfolio rather than a core holding until sustained profitability emerges. Everyone else should stay on the sidelines. The data says Rivian is moving forward, just not as fast or profitably as many hoped or expected.