Your retirement check is about to get squeezed by a Fed civil war you did not vote for. The cost of that fight is showing up in your bond fund, your CD ladder, and your gas tank.

The Stakes: a divided Fed means higher-for-longer rates and a sticky inflation tax on every retiree.

The Visible Change: An 8-4 Split and a Chair Who Will Not Leave

On April 29, 2026, the FOMC held the federal funds rate at 3.75% upper bound. The vote split 8-4, the widest dissent since October 1992. Governor Stephen Miran pushed for an immediate quarter-point cut. Regional presidents Beth Hammack, Neel Kashkari, and Lorie Logan opposed the easing bias in the statement.

Then Powell broke protocol. With his Chair term ending May 15, 2026 and Trump nominee Kevin Warsh already cleared by the Senate Banking Committee, Powell announced he will stay on as Governor through 2028. He called the Fed “battered” and cited a dropped DOJ probe as a “pressure tactic,” per Al Jazeera.

The Hidden Cost: Your Bonds Just Got Repriced

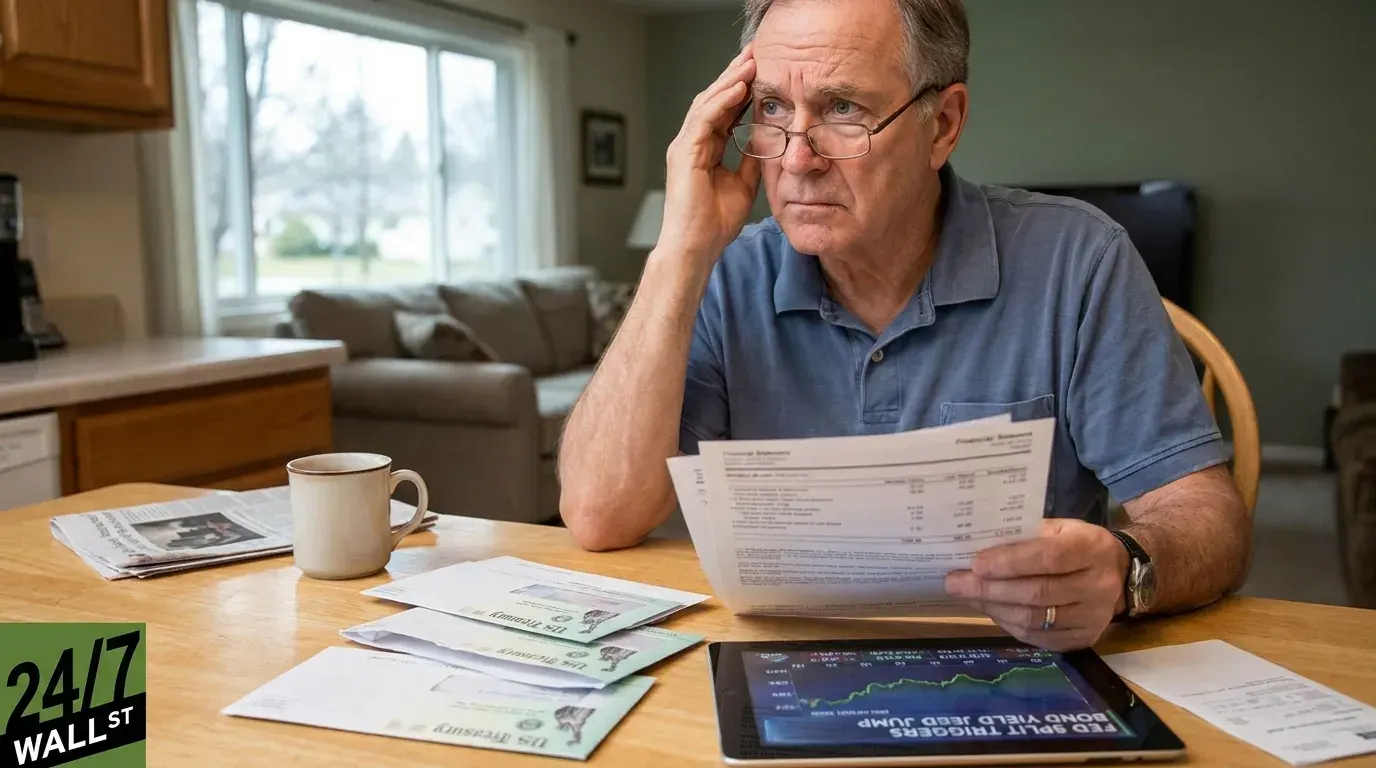

Markets reacted instantly. Per Reuters and Bloomberg, traders walked away from a 2026 rate cut and began pricing in a possible 2027 rate hike. The 10-year Treasury yield sits at 4.36% as of April 28, 2026, in the 79th percentile of the past 12 months. Higher yields knock down the price of bonds in your existing portfolio.

The inflation backdrop makes it worse. CPI hit 330.3 in March 2026, a 12-month high, and WTI crude jumped to $99.89 per barrel after spiking to $107 earlier this year on Strait of Hormuz disruptions. The Fed’s paralysis becomes a tax on every fixed-income retiree.

Who Pays the Most: Retirees on Fixed Incomes

Working households can negotiate raises. Retirees cannot. Consumer sentiment fell to 53.3 in March 2026, approaching recessionary levels, and Core PCE sits in the 91st percentile of the past year. Energy and medicine, two import-heavy categories, hit retirement budgets harder than salaried ones.

Defensive instruments retirees are evaluating in this environment:

- CD yields. Top-tier 12-month CDs remain anchored to the 3.75% upper bound while leadership is contested.

- Treasury bills and short notes. One-month-high yields allow laddered maturities without long-duration risk.

- TIPS for inflation protection. With CPI sticky and oil elevated, principal-adjusted Treasuries hedge the next print.

- Defensive dividend payers. Utilities and staples cushion the blow if growth slips back toward the 0.5% Q3 2025 reading.

Watch the May 15 transition and the next CPI release. The 10Y-2Y spread at 0.50%, in the 13.6th percentile, says the market does not believe this calm holds.