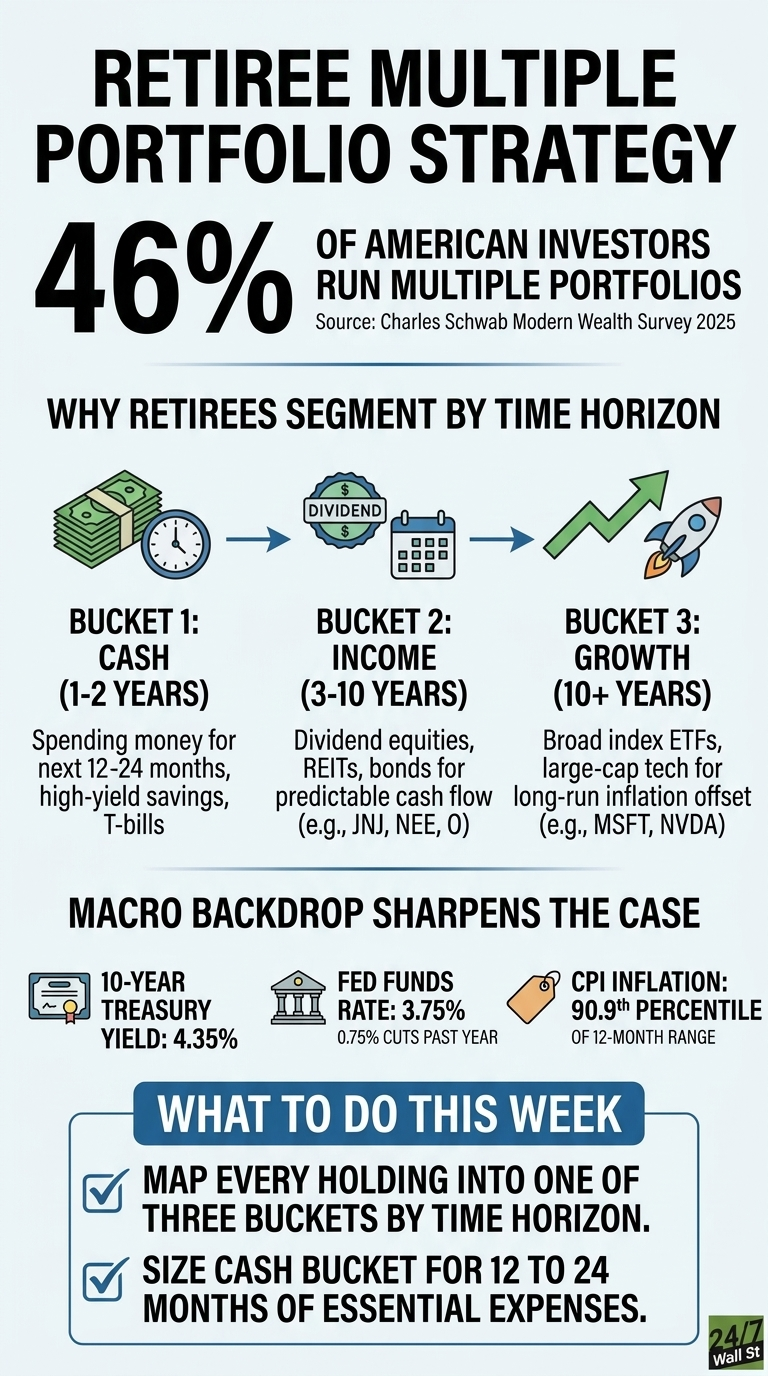

The Charles Schwab Modern Wealth Survey 2025 found that 46% of American investors maintain a main investment portfolio alongside one or more smaller, separate portfolios designated for different financial goals, while 39% still rely on a single portfolio for everything, and 15% run multiple portfolios used roughly equally. Among those running multiple accounts, 54% say the structure exists to pursue different financial objectives, with smaller groups citing new strategies (38%), new products (30%), and active trading (29%). For retirees, that pattern lines up almost exactly with the three-bucket retirement income framework that planners have used for decades.

Why Segmenting Matters More After the Paycheck Stops

Retirees no longer have wages to absorb a bad market year. A single blended portfolio forces the sale of whatever is liquid when rent is due, even if that means cashing out equities at a loss. Segmenting by time horizon addresses the sequence-of-returns problem directly: a cash bucket funds current spending, an income bucket refills the cash bucket, and a growth bucket refills the income bucket over a longer window.

The macro backdrop sharpens the case. The 10-year Treasury yields 4.35% as of April 27, 2026, the Fed Funds upper bound sits at 3.75% after 0.75 percentage points of cuts over the past year, and CPI is running at the 90.9th percentile of its 12-month range. Cash earns less than it did a year ago while inflation continues to erode purchasing power. The personal savings rate has fallen from 6.2% in Q1 2024 to 4.0% in Q4 2025, leaving thinner margins for retirees withdrawing from invested assets.

Bucket One: Cash for the Next 12 to 24 Months

The cash bucket holds spending money for the next one to two years. Typical vehicles include high-yield savings accounts, money market funds, short-duration Treasury ETFs, and Treasury bills laddered to mature when expenses come due. With short maturities that yield close to 10-year rates, this sleeve can cover real spending without forcing equity sales in a downturn. Sizing rule of thumb: 12 to 24 months of essential expenses, replenished quarterly from the income bucket.

Bucket Two: Income for Years Three Through Ten

The income bucket is built around dividend equities, REITs, and investment-grade bonds, with predictable cash flow as the design goal. Healthcare names such as Johnson & Johnson (NYSE:JNJ | JNJ Price Prediction) illustrate the dividend-aristocrat profile after raising its quarterly dividend 3.1% to $1.34 per share, extending a streak that now spans 64 consecutive years.

Regulated utilities like NextEra Energy (NYSE:NEE) anchor the same bucket, with 2026 adjusted EPS guidance of $3.92 to $4.02 and a yield near 2.44%.

Monthly-payer REITs such as Realty Income (NYSE:O), now on its 113th consecutive quarterly dividend increase with a yield around 5.08%, suit retirees who match income to monthly bills. Many investors use dividend-growth ETFs, broad REIT index ETFs, and aggregate bond ETFs to spread single-name risk across the bucket.

Bucket Three: Growth for Year Ten and Beyond

The growth bucket funds the back end of a 25- to 30-year retirement and offsets long-run inflation, which is why broad equity index ETFs and large-cap technology exposure typically anchor it. Mega-cap technology leaders reported FQ2 2026 revenue of $81.27 billion, up 16.7% year over year, and Q4 FY2026 revenue of $68.13 billion, up 73.2%, with Q1 FY2027 revenue guided to roughly $78 billion. Volatility comes with the territory; high-flying AI names carry a beta of 2.335, which is why this bucket should hold money the retiree does not plan to touch for at least a decade.

A Smaller Satellite Sleeve

Investors who want tactical exposure often add a small fourth sleeve, capped at 5% to 10% of the total. Regional banks like KeyCorp (NYSE:KEY), trading at a forward P/E of 12 with a 3.79% dividend yield, illustrate the cyclical financials that tend to benefit when the yield curve steepens. Capping the sleeve protects the rest of the plan from any single thesis going wrong.

What to Do This Week

- Map every current holding into one of the three buckets by time horizon. Anything that does not fit a defined role probably belongs somewhere else.

- Size the cash bucket to cover 12 to 24 months of essential expenses, and set up an automatic quarterly transfer from the income bucket to refill it.

- Open separate accounts or sub-accounts for each bucket. The Schwab survey shows that 57% of Americans believe modern portfolios are more sophisticated and require more professional guidance; structurally separating accounts makes it easier to apply and monitor that guidance.