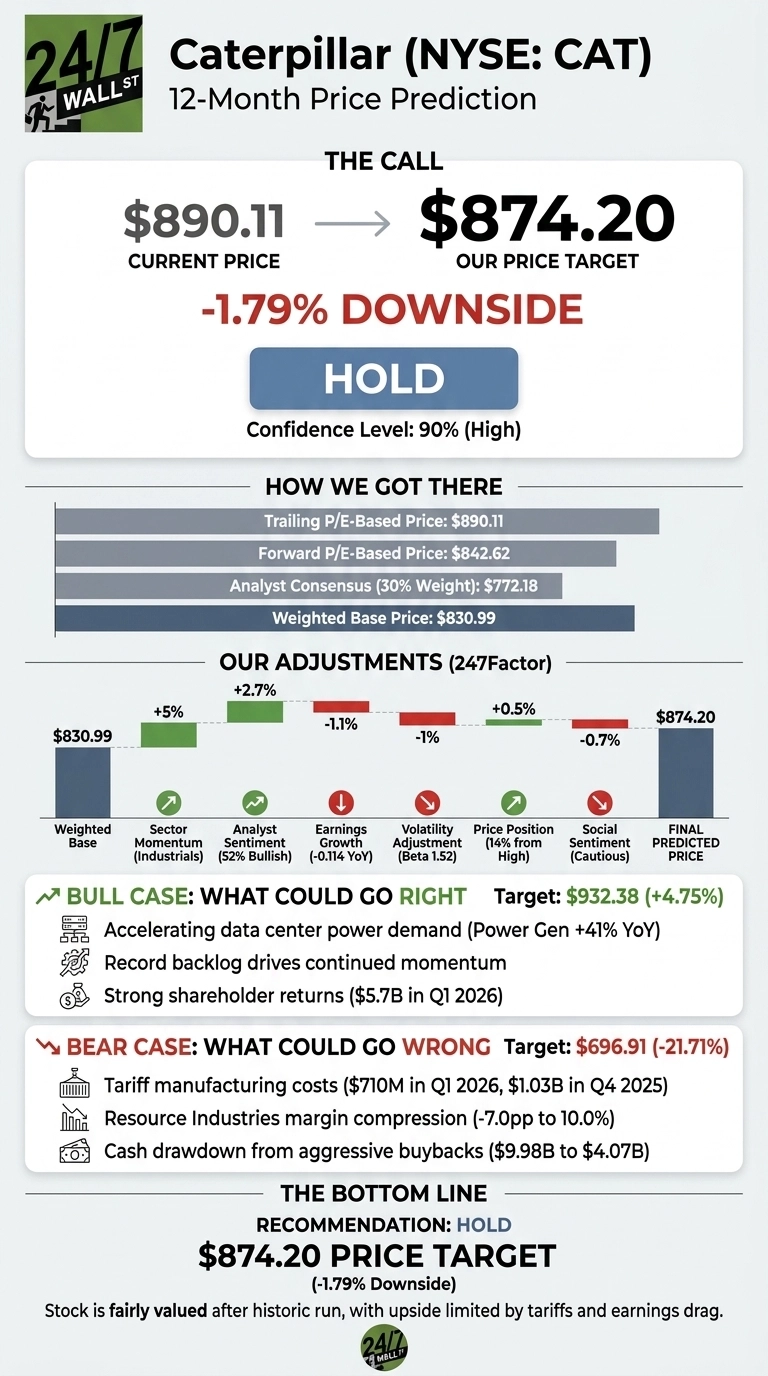

The industrial giant has gone on a tear. Caterpillar (NYSE:CAT | CAT Price Prediction) sits at $890.11 after a blowout Q1 2026 earnings report, up 25.88% in the past month and 190.94% over the past year.

Our 24/7 Wall St. price target for Caterpillar is $874.20 over the next 12 months, implying -1.79% downside. Our recommendation is hold, with high confidence at 90%. The stock is, in our view, fairly valued after a historic run.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $890.11 |

| 24/7 Wall St. Price Target | $874.20 |

| Upside/Downside | -1.79% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Our 24/7 Wall St. price target of $874.20 sits modestly below where Caterpillar trades today, and we want to be upfront: this is a stock with serious momentum. Real upside could come from accelerating data center power demand, where Power Generation revenue jumped 41% YoY, or from sustained infrastructure tailwinds. Treat the price target as one datapoint. A full bull case appears below.

A Record Quarter Sets the Stage

Caterpillar’s Q1 2026 results, released April 30, 2026, were the catalyst behind a 9.88% single-day surge. Revenue hit $17.41 billion, up 22% YoY, with EPS of $5.54.

Construction Industries grew 38% to $7.16 billion, and Power & Energy climbed 22%. CEO Joe Creed cited “a record backlog” as the foundation for momentum. The stock now trades just 14% below its 52-week high of $896.98 after a YTD gain of 56.04%.

The Case for $930+

Bulls have plenty to point to. Power Generation revenue rose 41% YoY on data center engine and turbine demand, with retail Power Gen sales up 48%. North America revenue jumped 32% to $10.23 billion.

Caterpillar returned $5.7 billion to shareholders in Q1 alone, including $5 billion in buybacks. With 15 Buy or Strong Buy ratings on the Street, our bull case scenario points to $932.38 over 12 months and a peak of $943.71.

The Risks Worth Watching

The bear case starts with tariffs. Manufacturing cost headwinds hit $710 million in Q1 2026, after $1.03 billion in Q4 2025. Resource Industries profit fell 39% with margin compression of 7 percentage points.

Cash dropped from $9.98 billion to $4.07 billion, and dealer inventory builds raise pull-forward demand risk. Bulls would counter that the cash drawdown reflects aggressive buybacks, and that tariff pressure is an external cost issue. Insider activity has skewed toward selling. Our bear scenario lands at $696.91, a -21.71% drawdown.

Hold for Now

Our 24/7 Wall St. price target is $874.20, the recommendation is hold, and confidence is 90%. The decisive factor: the stock has already priced in the data center boom.

The bullish path requires Power Generation orders to accelerate further and tariff costs to ease in the back half of 2026. The cautious path opens up if dealer inventory builds reverse or Resource Industries margins keep compressing. After a 190.94% one-year run, the setup favors patience over chasing the run.

Caterpillar Price Prediction 2026-2030

Looking further ahead, here is where our 24/7 Wall St. price target model projects Caterpillar could trade in the coming years, assuming current growth trajectories and tariff dynamics normalize.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $874.20 |

| 2027 | $905 |

| 2028 | $935 |

| 2029 | $955 |

| 2030 | $975.44 |

These projections assume Caterpillar continues executing on backlog conversion and data center demand. Significant upside or downside could result from a step-change in infrastructure spending or a sustained downturn in mining capex.