Alphabet (NASDAQ:GOOG | GOOG Price Prediction) just delivered a standout Q1, and our model points to additional upside. After a 9.97% single-day jump on the Q1 print, GOOG now trades at $381.94. Our 24/7 Wall St. price target for Alphabet is $460, implying 20.44% upside over the next 12 months.

Our recommendation is buy, with a 90% confidence level. This is one of our higher-conviction calls in large-cap tech right now.

| Metric | Value |

|---|---|

| Current Price | $381.94 |

| 24/7 Wall St. Price Target | $460 |

| Upside | 20.44% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Q1 Print That Reset the Narrative

Alphabet has rallied, climbing 13.08% over the past week, 33.15% over the past month, and 138.21% over the past year. Shares now sit roughly 3% below the 52-week high of $382.63, well off the $148.97 low.

The catalyst was Q1 2026, reported April 29, 2026. EPS came in at $5.11 versus the $2.63 consensus, a 94.1% beat that included $36.91B in unrealized equity gains. Revenue hit $109.90B, growing 21.79% YoY, with operating margin expanding to 36.1%. Cloud was the headline, posting 63% growth to $20.028B with backlog nearly doubling QoQ to over $460 billion.

Why Bulls See a Breakout Ahead

The bull case rests on Cloud and AI monetization. Gemini is now processing more than 16 billion tokens per minute via direct API, up 60% from the prior quarter, and Gemini Enterprise paid MAUs grew 40% QoQ. Paid subscriptions reached 350 million, Waymo crossed 500,000 autonomous rides per week, and Search revenue still grew 19% despite AI competition fears.

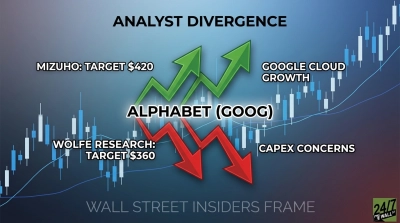

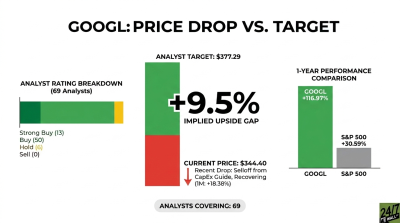

Of 69 analyst ratings, 63 are Buy or Strong Buy, with zero Sell calls. Our bull-case scenario points to $533.07 by May 2027, a 39.57% total return. CEO Sundar Pichai framed it on the call: “2026 is off to a terrific start. Our AI investments and full stack approach are lighting up every part of the business.”

The Risks Worth Watching

The bear case is real. Capex more than doubled YoY to $35.674B, driving free cash flow down 46.63% to $10.116B. Management’s $175B to $185B 2026 capex guide creates ROI risk if AI monetization lags.

Google Network revenue declined to $6.971B from $7.256B, and the EU’s $3.5B fine highlights ongoing regulatory pressure. Bulls would counter that the FCF decline reflects deliberate infrastructure investment funding the very Cloud backlog now compounding at triple-digit rates. Our bear case lands at $362.22, a modest 5.16% drawdown.

The Bottom Line

The 24/7 Wall St. price target sits at $460, recommendation buy, confidence 90%. The factor that tips the scale is the Cloud backlog: $460 billion of contracted future revenue is a multi-year visibility moat that justifies aggressive capex.

The bull thesis holds if Gemini and Cloud monetization sustain north of 40% growth into 2027. The bear thesis holds if the $175B to $185B capex commitment turns into a margin trap before revenue catches up.

Alphabet Price Prediction 2026-2030

Looking further ahead, here is where our 24/7 Wall St. price target model projects Alphabet could trade in the coming years, assuming current growth trajectories and AI monetization continue.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $460 |

| 2027 | $515 |

| 2028 | $575 |

| 2029 | $625 |

| 2030 | $673.60 |

These projections assume Alphabet continues executing on Cloud, Gemini, and Waymo. Significant upside or downside could come from a step-change in AI search monetization or, conversely, a Department of Justice remedy that forces structural changes to Search distribution.