Eli Lilly (NYSE:LLY | LLY Price Prediction) just delivered one of the strongest first quarters in big pharma history, but shares have pulled back sharply from their February peak. That gap between operating performance and stock price is where our model sees opportunity.

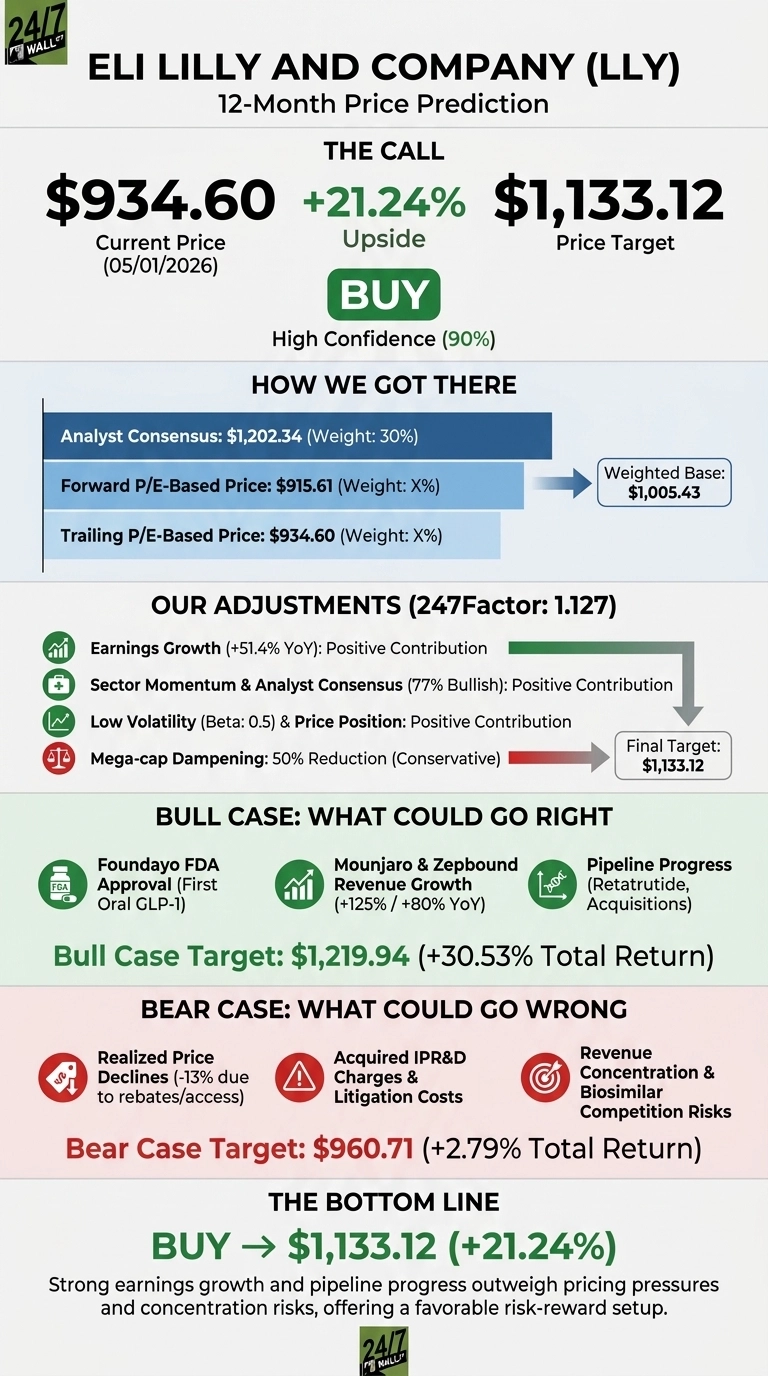

Our 24/7 Wall St. price target for Eli Lilly is $1,133.12 over the next 12 months, implying 21.24% upside from the current price of $934.60. Our recommendation is buy with a 90% confidence rating, our highest tier.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $934.60 |

| 24/7 Wall St. Price Target | $1,133.12 |

| Upside | 21.24% |

| Recommendation | BUY |

| Confidence Level | 90% |

From $1,062 Peak to a Buyable Pullback

Lilly is down 12.89% year to date after peaking near $1,062 in December 2025, yet shares jumped 9.8% on April 30 following a blockbuster Q1 earnings report.

Revenue hit $19.80 billion, beating estimates by 11.25% and growing 55.5% year over year. Non-GAAP EPS came in at $8.55 versus a $6.79 consensus, a 25.88% beat. Mounjaro alone generated $8.66 billion (up 125%), and Zepbound added $4.16 billion (up 80%). Lilly raised full-year revenue guidance to $82 billion to $85 billion and EPS guidance to $35.5 to $37.

The Case for $1,219 and Higher

Bulls have plenty of fuel. CEO David Ricks called out “the U.S. FDA approval of Foundayo, the only approved GLP-1 pill that can be taken any time of day, without food and water restrictions.” An oral GLP-1 dramatically expands the addressable obesity market beyond injectables.

Retatrutide Phase 3 data showed significant A1C and weight reductions in type 2 diabetes, and Mounjaro joined China’s National Reimbursed Drug List. Four announced acquisitions (Orna, Centessa, Kelonia, Ajax) extend the pipeline into cell therapy and CAR-T.

Our bull-case scenario takes shares to $1,219.94, a 30.53% total return. Analyst consensus already sits at $1,202.34 with 24 buy ratings against one sell.

The Risks Worth Watching

Realized prices fell 13% in Q1 as rebates and access agreements bit into Mounjaro and Zepbound economics. China NRDL inclusion, while expanding volume, compresses international price per dose. Lilly also booked $584 million in acquired IPR&D charges and $279 million in litigation-related charges this quarter.

Bulls would counter that volume grew 65%, more than offsetting price declines, and IPR&D charges reflect investment in tomorrow’s pipeline rather than core profit erosion. Still, revenue concentration in two GLP-1 products and looming biosimilar competition justify caution. Our bear case lands at $960.71, only 2.79% above today.

Bottom Line

The 24/7 Wall St. price target of $1,133.12 with a buy rating and 90% confidence reflects a rare setup: a mega-cap compounding earnings above 50% while shares trade 12.89% below where they started the year.

The bull thesis hinges on whether Foundayo can scale the GLP-1 category beyond injection-comfortable patients. The bear thesis centers on rebate pressure compressing gross margins faster than volume growth offsets. The risk-reward skews favorable based on our model.

Eli Lilly Price Prediction 2026-2030

Looking further ahead, here is where our 24/7 Wall St. price target model projects Lilly could trade in coming years, assuming current growth trajectories and margin guidance hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $1,133.12 |

| 2030 | $1,674.95 |

These projections assume Lilly continues executing on Foundayo, retatrutide, and pipeline acquisitions. Significant upside or downside could come from oral GLP-1 share gains, biosimilar timing, or further pricing concessions in major markets.