I keep buying Eli Lilly (NYSE:LLY | LLY Price Prediction), and the latest quarter just made it harder to stop. This is a confession of conviction. I have been adding through every dip in 2026, and the most recent earnings report told me the thesis is accelerating.

What pulls me back to the buy button is simple. Lilly sits at the center of the largest therapeutic shift in modern medicine, the GLP-1 build-out for diabetes and obesity, and it is the only company with a metabolic franchise this deep, this fast-growing, and this defensible.

When CEO David Ricks said “2026 is off to a strong start” and that Foundayo “will meaningfully expand the number of people who can benefit from GLP-1s,” I read that as the next leg of compounding starting.

The data behind the conviction

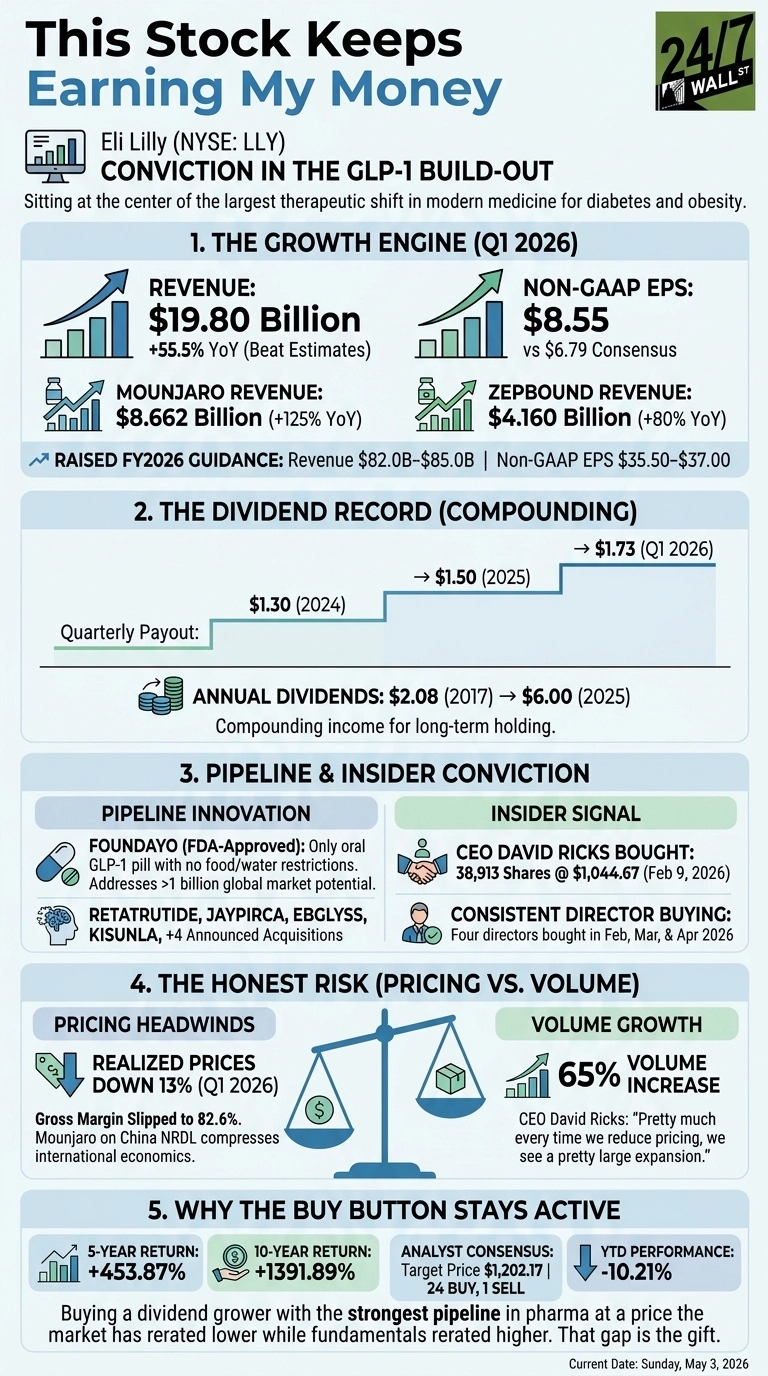

Reason one is the growth engine. Q1 2026 revenue came in at $19.80 billion, up 55.5% year over year, with non-GAAP EPS of $8.55 against a $6.79 consensus.

Mounjaro printed $8.662 billion, up 125%, and Zepbound delivered $4.160 billion, up 80%. Management raised full-year guidance to $82 billion to $85 billion in revenue and $35.5 to $37 in non-GAAP EPS. Companies this size do not grow this fast by accident.

Reason two is the dividend record. The quarterly payout climbed from $1.30 in 2024 to $1.50 across 2025 and then $1.73 in Q1 2026. Annual dividends went from $2.08 in 2017 to $6 in 2025. That is the kind of compounding I want sitting in a retirement account for a decade.

Reason three is the pipeline and insider conviction. Foundayo, the only approved GLP-1 pill with no food or water restrictions, opens an oral market Ricks pegs at “over 1 billion people around the world with obesity and related conditions.” Behind it sit retatrutide, Jaypirca, Ebglyss, Kisunla, and four announced acquisitions. Then on February 9, 2026, CEO Ricks bought 38,913 shares at $1,044.67, alongside more than a dozen other executives. Four directors have kept buying in February, March, and April 2026. That is the clearest signal I track.

The honest risk

Pricing is the real concern. Realized prices fell 13% in Q1, gross margin slipped to 82.6%, and the Mounjaro NRDL addition in China compresses international economics. Revenue concentration in two products is a genuine vulnerability. The reason it has not changed my thesis is volume.

The business posted 65% volume growth, and Ricks framed it plainly: “Pretty much every time we reduce pricing, we see a pretty large expansion.” Lower price, far more patients, more durable franchise.

Why the buy button stays active

The stock is down 10.21% year to date while the underlying business compounds at over 50% growth. Five-year return: 453.87%. Ten-year return: 1391.89%.

Analyst consensus sits at $1,202.17 with 24 buy ratings against one sell. I am buying a dividend grower with the strongest pipeline in pharma at a price the market has rerated lower while the fundamentals rerated higher. That gap is the gift, and I plan to keep taking it.