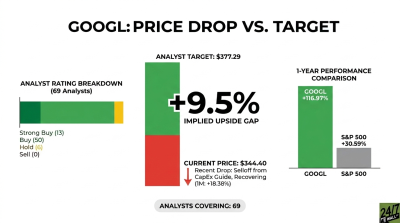

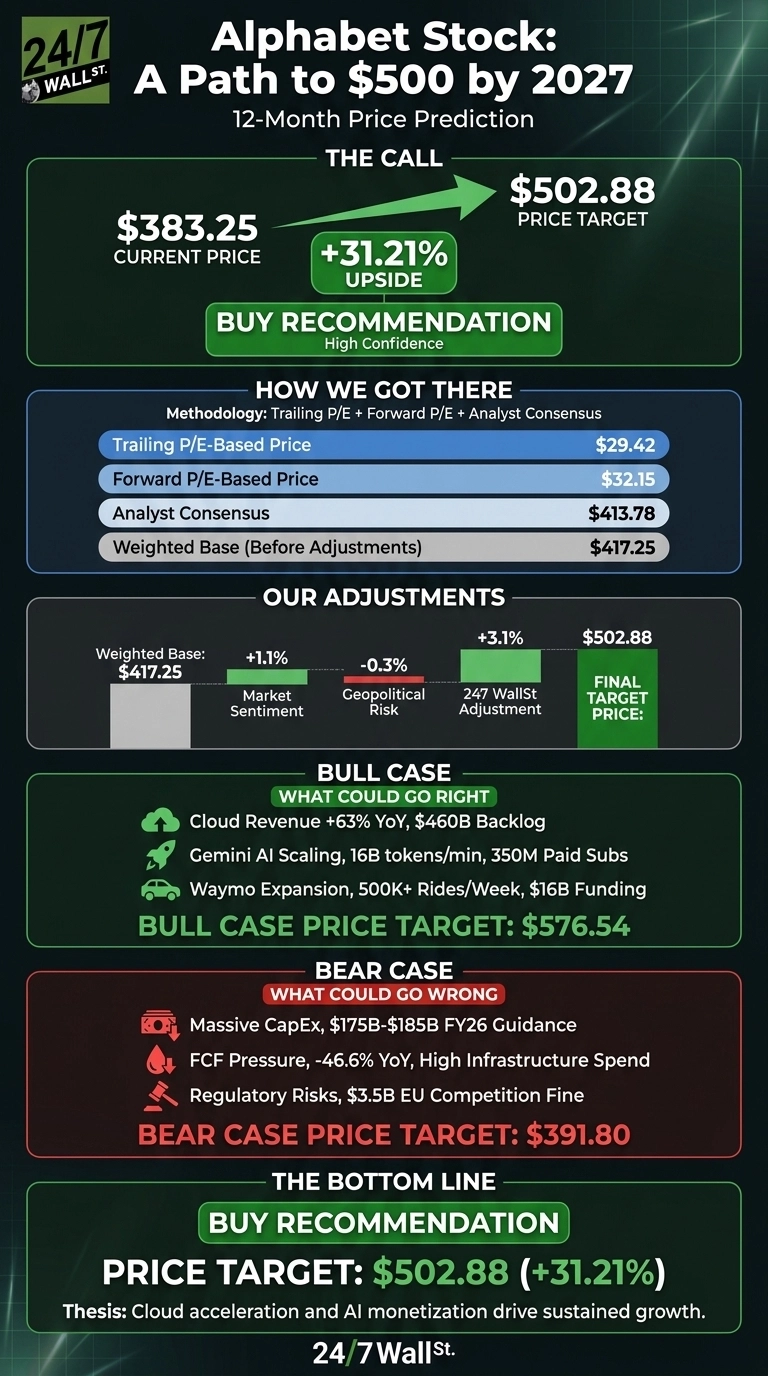

Our 24/7 Wall St. price target for Google (NASDAQ: GOOGL | GOOGL Price Prediction) points to $502.88 over the next 12 months, which would take shares well past the $500 mark. With GOOGL trading at $383.25, that implies 31.21% upside. The model’s rating is buy with a high confidence reading of 90%. Cloud is compounding, Gemini usage is scaling rapidly, and free cash flow continues to fund the buildout.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $383.25 |

| 24/7 Wall St. Price Target | $502.88 |

| Upside | 31.21% |

| Recommendation | BUY |

| Confidence Level | 90% |

Cloud Surge and the Sprint Past $380

GOOGL has rallied sharply. Shares are up 9.39% in the past week, 29.58% over one month, and 134.45% over the past year. The catalyst was a blowout Q1 FY2026 report on April 29, 2026: revenue of $109.896 billion (up 21.79% YoY) and EPS of $5.11 against a $2.63 consensus, a 94.1% beat. Google Cloud revenue jumped 63% to $20.028 billion, with backlog nearly doubling to over $460 billion.

Operating margin expanded to 36.1%, and the board raised the dividend 5% to $0.22 per quarter.

The Case for $575+

Cloud is accelerating quarter over quarter, and the $460 billion backlog gives multi-year revenue visibility. Gemini is processing more than 16 billion tokens per minute via API, up 60% from the prior quarter, while paid subscriptions reached 350 million. Waymo is running over 500,000 autonomous rides per week and just closed a $16B funding round.

CEO Sundar Pichai stated: “2026 is off to a terrific start. Our AI investments and full stack approach are lighting up every part of the business.” Our bull-case scenario lifts GOOGL to $576.54 by May 2027, a 50.43% total return.

What Could Stall the Rally

The bear case centers on capital intensity. Q1 CapEx of $35.674 billion more than doubled YoY, dragging free cash flow down 46.63% to $10.116 billion. Full-year 2026 CapEx guidance of $175 billion to $185 billion is substantial. Bulls counter that this spend funds the cloud backlog and AI capacity directly tied to the 63% Cloud growth.

Other risks: Google Network revenue slipped from $7.256 billion to $6.971 billion, insider activity skews toward selling per 158 recent transactions, and the headline net income of $62.578 billion was flattered by $36.91 billion in unrealized equity gains that can reverse. Our bear case lands at $391.80, essentially flat from here.

A Bullish Setup

Our price target of $502.88, a buy rating, and high confidence rest on one tipping factor: cloud growth is accelerating. The thesis strengthens if Q2 Cloud revenue holds the 50%+ growth trajectory and CapEx translates into incremental backlog. It weakens if backlog conversion stalls or AI monetization fails to offset Network ad weakness. Right now, the data tilts decisively bullish.

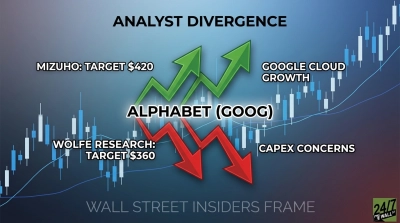

Canaccord raised the firm’s price target to $450 from $415 and keeps a Buy rating on the shares. The firm said Google reported strong Q1 results, with total revenue modestly ahead of expectations on continued Search momentum and a standout quarter for Cloud.

Looking ahead, our price target model projects GOOGL could trade in the coming years, anchored by base-case 5-year output of $833.42 by May 2031.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $502 |

| 2027 | $577 |

| 2028 | $655 |

| 2029 | $740 |

| 2030 | $833 |

These projections assume Alphabet continues compounding cloud and AI revenue while defending Search. Significant upside or downside could come from regulatory action on Search distribution or a step-function breakthrough in Gemini that resets the AI competitive landscape.