Merck (NYSE:MRK | MRK Price Prediction) delivered its fourth consecutive earnings beat, but shares slipped on the earnings report. With acquisition charges clouding the quarter, here is where the stock heads next.

The 24/7 Wall St. Price Target for Merck Is $135.70

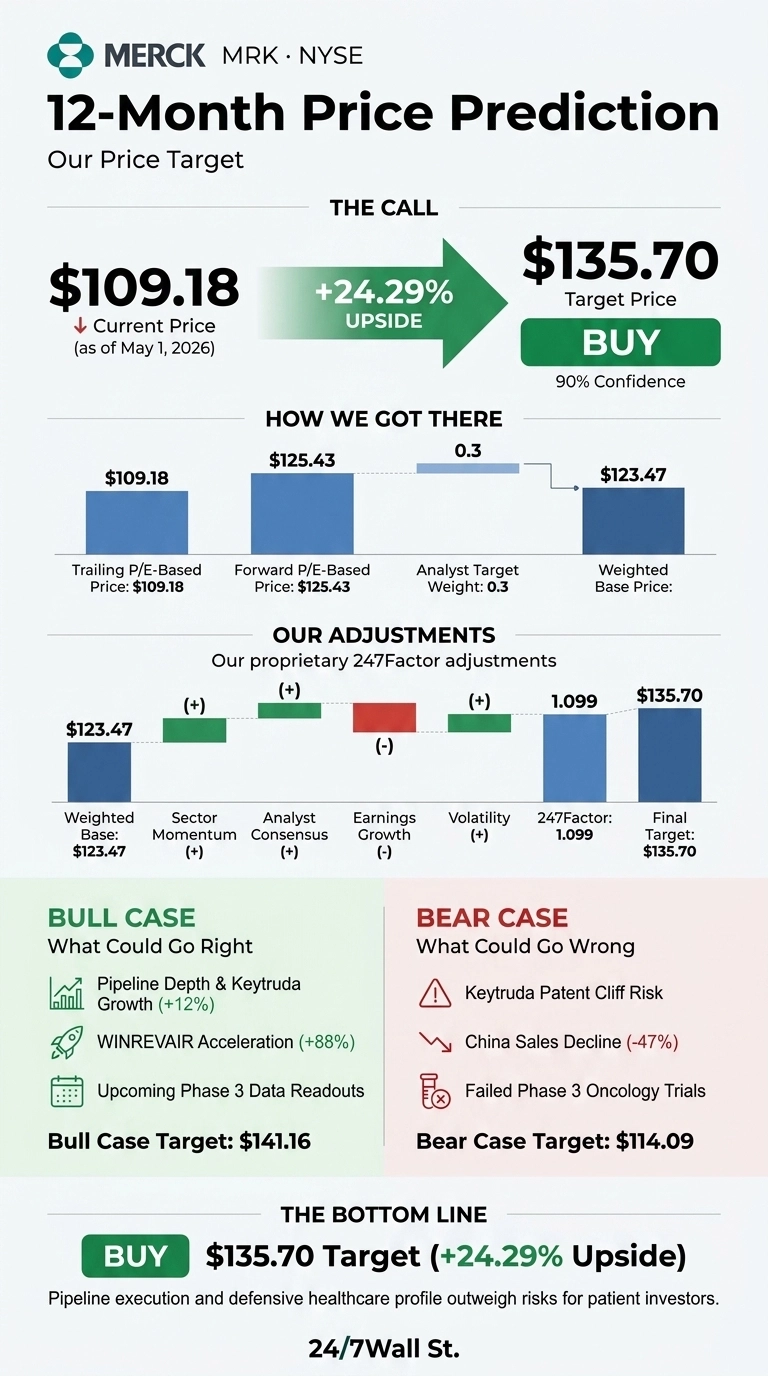

Our 24/7 Wall St. price target for Merck is $135.70 over the next 12 months, implying 24.29% upside from the current $109.18. Our recommendation is buy, with a confidence level of 90%. A defensive healthcare profile, deep Phase 3 pipeline, and stock trading well below its 52-week high create an attractive setup for patient investors.

| Metric | Value |

|---|---|

| Current Price | $109.18 |

| 24/7 Wall St. Price Target | $135.70 |

| Upside | 24.29% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Quarter Dominated by KEYTRUDA and Acquisition Charges

Merck reported Q1 2026 revenue of $16.29 billion, growing 4.87% year over year and beating consensus by 2.77%. Non-GAAP EPS of -$1.28 topped the -$1.47 estimate, a 13.15% beat. The headline loss reflects a $9.0 billion Cidara acquisition charge, with operating performance remaining intact.

KEYTRUDA generated $8.03 billion (up 12%), while WINREVAIR jumped 88% to $525 million. Management raised full-year guidance to $65.80 billion to $67 billion in revenue and $5.04 to $5.16 in non-GAAP EPS.

Despite the beat, shares slipped 1.6% on the day and are down 9.24% over the past month, though up 32.8% over the past year.

The Case for $141 and Beyond

The bull thesis rests on pipeline depth. The CEO highlighted “we are moving with speed to transform our portfolio to one with a diversified set of growth drivers across a broad set of therapeutic areas… as we enter a particularly robust period of Phase 3 data readouts.”

Near-term catalysts include the June 19, 2026 WELIREG + KEYTRUDA adjuvant RCC PDUFA, the August 17, 2026 KEYTRUDA + Padcev MIBC decision, and the October 10, 2026 ifinatamab deruxtecan PDUFA.

Wall Street consensus is 62% bullish with 18 buy/strong buy ratings versus zero sell ratings. Our bull-case scenario lands at $141.16 for a 29.29% total return.

What Could Go Wrong

The bear case centers on the KEYTRUDA patent cliff, GARDASIL’s China collapse (down 19% with China revenue down 47%), and three failed Phase 3 oncology trials (LITESPARK-012, KEYNOTE-975, and KEYNOTE-866).

Bulls counter that $14.8 billion in combined Cidara and Terns charges represent investments in long-duration growth, while GAAP losses mask non-GAAP profitability backed by an 82% gross margin.

The bear-case scenario lands at $114.09, modest 4.5% upside that still reflects the floor provided by Merck’s defensive characteristics and forward P/E of 22x.

The Bottom Line on Merck

The 24/7 Wall St. price target of $135.70 and buy rating reflect 90% confidence that pipeline execution outweighs the noise. The bull case rests on KEYTRUDA’s expanding indications and WINREVAIR’s 88% growth bridging the company through patent expirations.

The bear case strengthens if more Phase 3 trials fail or China weakness spreads to other franchises. The setup, near 52-week lows on a stock with a 2.94% dividend yield and 15x trailing P/E, marks one of the more attractive valuation setups Merck has shown in months.

Here is where our 24/7 Wall St. price target model projects Merck could trade, assuming current pipeline execution and healthcare sector dynamics hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $135.70 |

| 2027 | $150 |

| 2028 | $168 |

| 2029 | $187 |

| 2030 | $207.82 |

These projections assume Merck executes on its pipeline strategy. Significant upside or downside could result from KEYTRUDA biosimilar timing or breakthrough Phase 3 data from the June 1, 2026 Oncology Investor Event at ASCO.