The airline industry has always been brutally cyclical, but 2026 is exposing just how thin the margin for error really is. Oil prices have surged following President Trump’s military confrontation with Iran, consumers are pulling back on discretionary travel, and weaker carriers are discovering that low fares only work when costs stay under control.

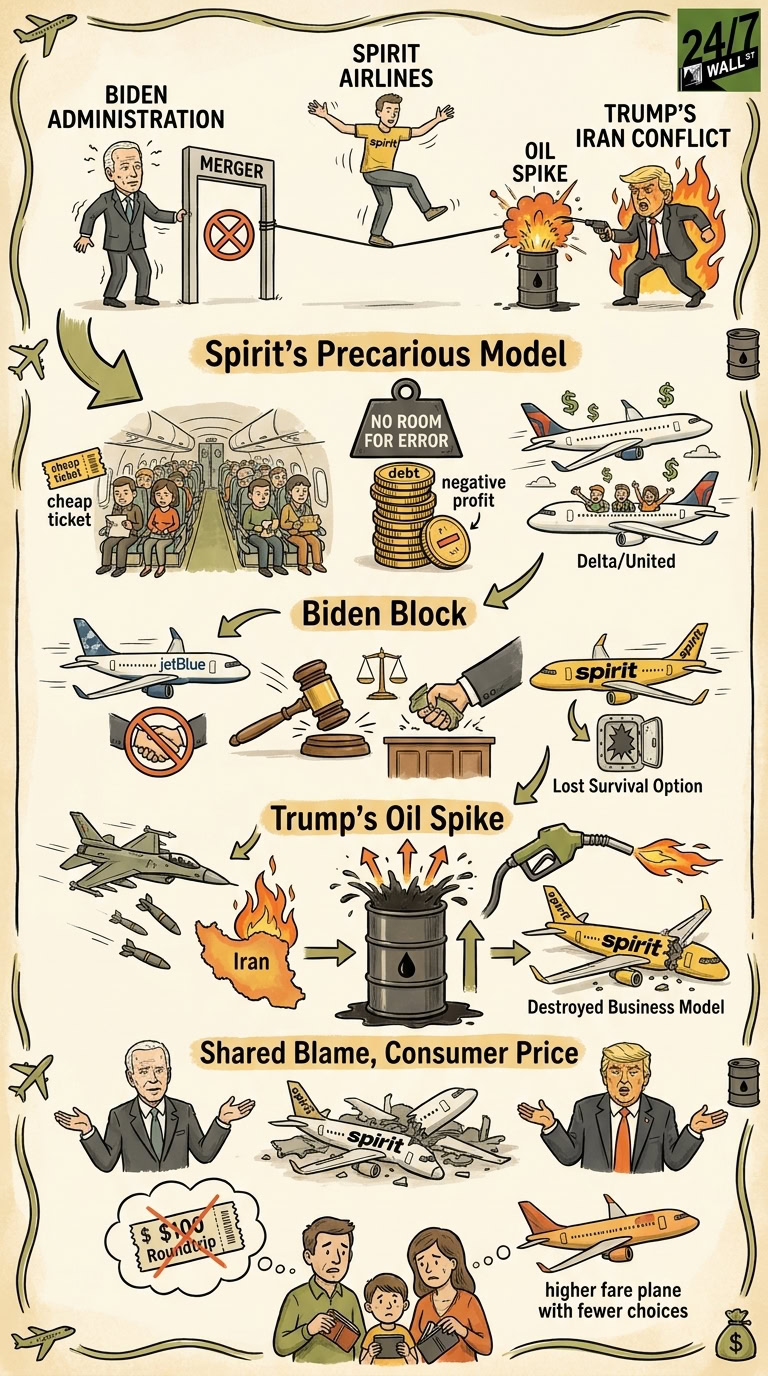

That backdrop matters because it explains why the collapse of Spirit Airlines was never caused by a single event. The ultra-low-cost carrier was already walking a financial tightrope. The real question investors should ask is this: who shook the rope harder — President Biden or Trump?

Spirit Built a Massive Following — and Reputation Problem

For years, Spirit Airlines succeeded by offering fares legacy airlines could not touch. Roundtrip tickets under $100 became common. Travelers hated the fees, complained about cramped seating, and routinely ranked Spirit near the bottom in customer satisfaction surveys from organizations like J.D. Power, yet planes stayed full because price-sensitive consumers cared more about affordability than luxury.

That model worked when fuel prices remained manageable and demand stayed strong. But Spirit’s finances were deteriorating long before its shutdown. According to its SEC filings, the airline lost $1.2 billion between 2023 and 2025 while carrying more than $5 billion in total debt and lease obligations. Its operating margin remained deeply negative even as larger rivals like Delta Air Lines (NYSE:DAL | DAL Price Prediction) and United Airlines (NASDAQ:UAL) returned to profitability.

Here’s what the numbers looked like before the collapse:

| Airline | 2025 Operating Margin | Net Debt/EBITDA | Average Fare Strategy |

| Spirit Airlines | -14.8% | Negative EBITDA | Ultra-low-cost |

| JetBlue Airways (NASDAQ:JBLU) | -3.1% | 5.8x | Discount |

| Delta Air Lines | 9.2% | 2.1x | Premium |

| United Airlines | 7.3% | 2.4x | Mixed |

Spirit had almost no room for error. One shock could push it over the edge.

Biden’s Administration Blocked Spirit’s Lifeline

In early 2024, the Biden Justice Dept. successfully blocked JetBlue Airways from acquiring Spirit Airlines. Federal regulators argued the merger would reduce competition and raise fares because Spirit’s ultra-cheap tickets pressured larger airlines to keep prices low.

Ironically, regulators may have been correct about fares. Now that Spirit is gone entirely, airfare pricing pressure could weaken even more.

The court ruling effectively removed Spirit’s best survival option. JetBlue had offered roughly $3.8 billion for the airline, including debt assumptions and shareholder compensation. Spirit shareholders approved the deal. Management supported it. Yet the merger died in court after the Justice Dept. argued consumers would lose access to budget travel.

Unsurprisingly, that concern may now become reality anyway.

With Spirit liquidated, thousands of employees have lost jobs, routes are disappearing, and budget-conscious travelers face fewer ultra-low-cost choices. Frontier Airlines (NASDAQ:ULCC) remains, but Spirit had become one of the largest ULCC operators in the country with more than 200 aircraft before the collapse.

Granted, Spirit’s balance sheet problems existed before Biden blocked the merger. But removing the company’s clearest path to survival undeniably accelerated the pressure.

Trump’s Iran Conflict May Have Delivered the Final Blow

That said, the proximate cause of Spirit’s shutdown appears tied directly to fuel costs.

Following Trump’s military escalation with Iran and disruptions around the Strait of Hormuz, crude oil prices surged sharply in 2026. Brent crude briefly climbed above $118 per barrel, while jet fuel prices rose more than 35% year over year.

For most airlines, higher fuel costs hurt profits. For Spirit, they destroyed the business model.

Spirit relied on ultra-low fares and high passenger volume. It lacked the premium seating, international business traffic, and loyalty program economics that larger airlines use to offset rising costs. Fuel historically represented roughly 30% of Spirit’s operating expenses, so when oil spiked, the airline simply could not raise ticket prices enough without losing customers.

Management reportedly told creditors the current operating environment had become unsustainable due to fuel inflation and weakening consumer demand.

In other words, Trump’s Iran conflict may not have created Spirit’s weaknesses, but it exposed them at exactly the wrong moment.

Key Takeaway

In short, there is plenty of blame to go around. The Biden administration likely bears responsibility for blocking the JetBlue acquisition that could have preserved jobs, aircraft capacity, and shareholder value. Spirit lost access to its clearest financial escape hatch after the merger ruling.

But when all is said and done, Trump’s Iran conflict and the resulting oil spike appear to have been the immediate trigger that made continued operations impossible. While his attempt to save the airline was thwarted by creditors, it sealed Spirit’s fate.

If investors are assigning percentages, the evidence probably leans slightly toward Biden carrying more responsibility because the merger block removed Spirit’s long-term survival option while there was still time. Higher fuel prices hurt every airline. Spirit alone lacked the balance sheet to absorb the shock because regulators prevented consolidation.

In any case, consumers will end up paying the price. Spirit’s disappearance removes one of the industry’s strongest downward pressures on airfare pricing — and airline tickets rarely get cheaper when competition disappears.