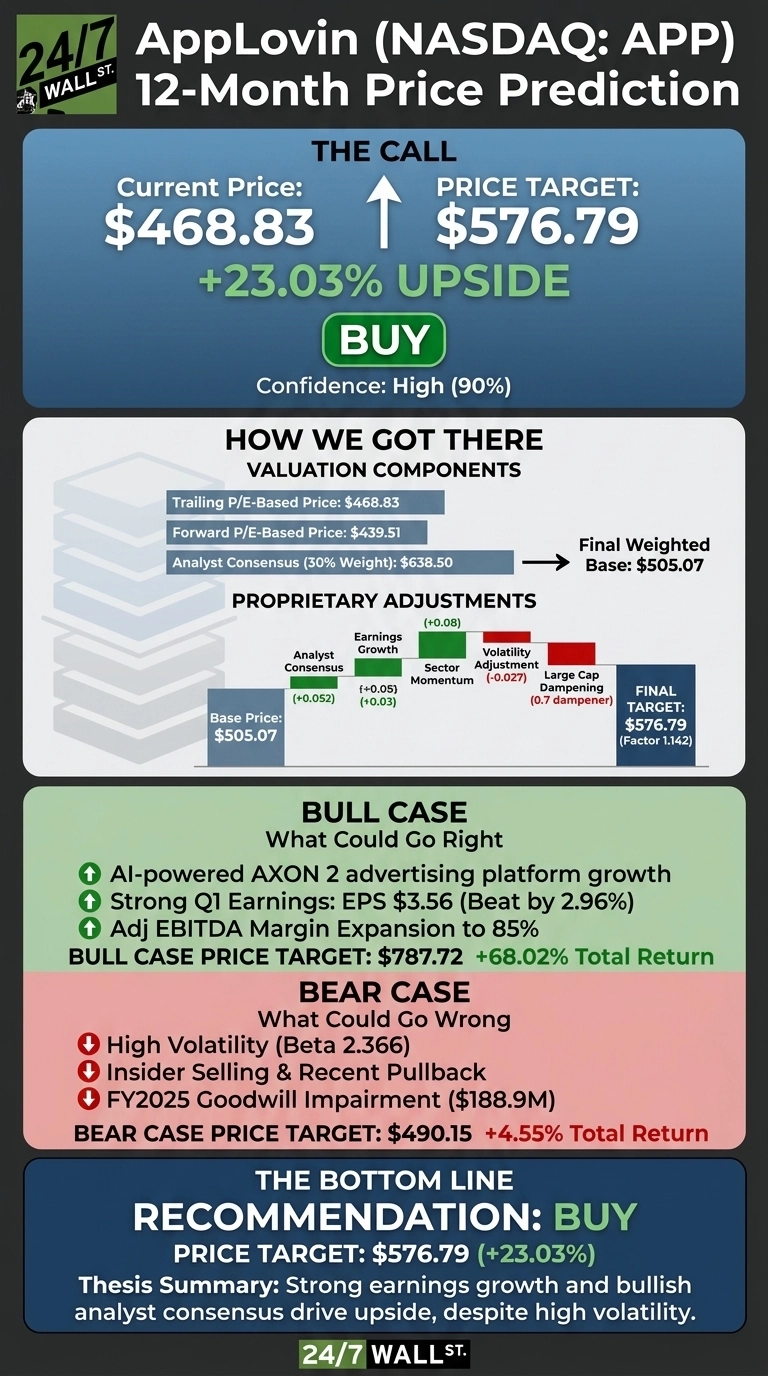

Our AppLovin (NASDAQ:APP | APP Price Prediction) call comes at a moment when the stock has recovered ground after a weak first quarter. Shares trade at $468.83 as of writing, and our proprietary model points to meaningful upside from here. The 24/7 Wall St. price target for AppLovin is $576.79, implying 23.03% upside over the next 12 months. Confidence is high at 90%, and the recommendation is buy.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $468.83 |

| 24/7 Wall St. Price Target | $576.79 |

| Upside | 23.03% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Volatile Year, A Strong Q1

APP has been volatile. Shares are up 53.91% over the past year and 13.61% in the past month, but down 30.42% year to date after peaking near $745.61 last cycle.

Q1 2026 beat expectations across the key lines. AppLovin posted EPS of $3.56 against a $3.46 estimate, revenue of $1.84 billion (up 24.15% YoY), and adjusted EBITDA margin of 85%. Net income more than doubled to $1.21 billion, and free cash flow hit $1.29 billion, funding $1 billion in buybacks. Q2 guidance calls for revenue of $1.92 billion to $1.95 billion.

Why Bulls See a Breakout to $787

The bull case rests on AXON 2, AppLovin’s AI ad engine, continuing to compound. Pure play ad tech focus following the games divestiture has expanded the adjusted EBITDA margin to 85%, and operating income grew 117% YoY. The Street target of $638.50 reflects 26 buy or strong buy ratings versus zero sells. Our bull case scenario projects shares could reach $787.72 by May 2027, a 68.02% total return, if AppLovin extends ad tech share gains beyond mobile gaming into e-commerce and CTV.

What Could Go Wrong

The bear case is meaningful. APP carries a beta of 2.36, sits 14% below its 52 week high, and trades at a forward P/E of 31. FY2025 included a $188.9 million goodwill impairment, and insider activity skews to selling.

Bulls would counter that the goodwill charge is a one time mark and that buyback intensity (2.2 million shares in Q1) signals management conviction. Our bear case scenario lands at $490.15, only 4.55% above today.

Our Take on APP Here

The price target of $576.79 with 90% confidence supports a buy rating. The tipping factor is margin structure: 76.9% operating margins on accelerating revenue is rare. The bull thesis strengthens if Q2 lands inside guidance and the AXON platform shows continued ad spend growth from non-gaming verticals. The thesis weakens if revenue growth decelerates below 20% YoY or if regulatory scrutiny on ad attribution intensifies.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $576.79 |

| 2027 | $574.69 |

| 2028 | $686.62 |

| 2029 | $750.14 |

| 2030 | $776.99 |

These projections assume AppLovin continues executing its pure play ad tech strategy. Significant upside or downside could result from AXON adoption beyond mobile gaming or a broader ad market downturn.