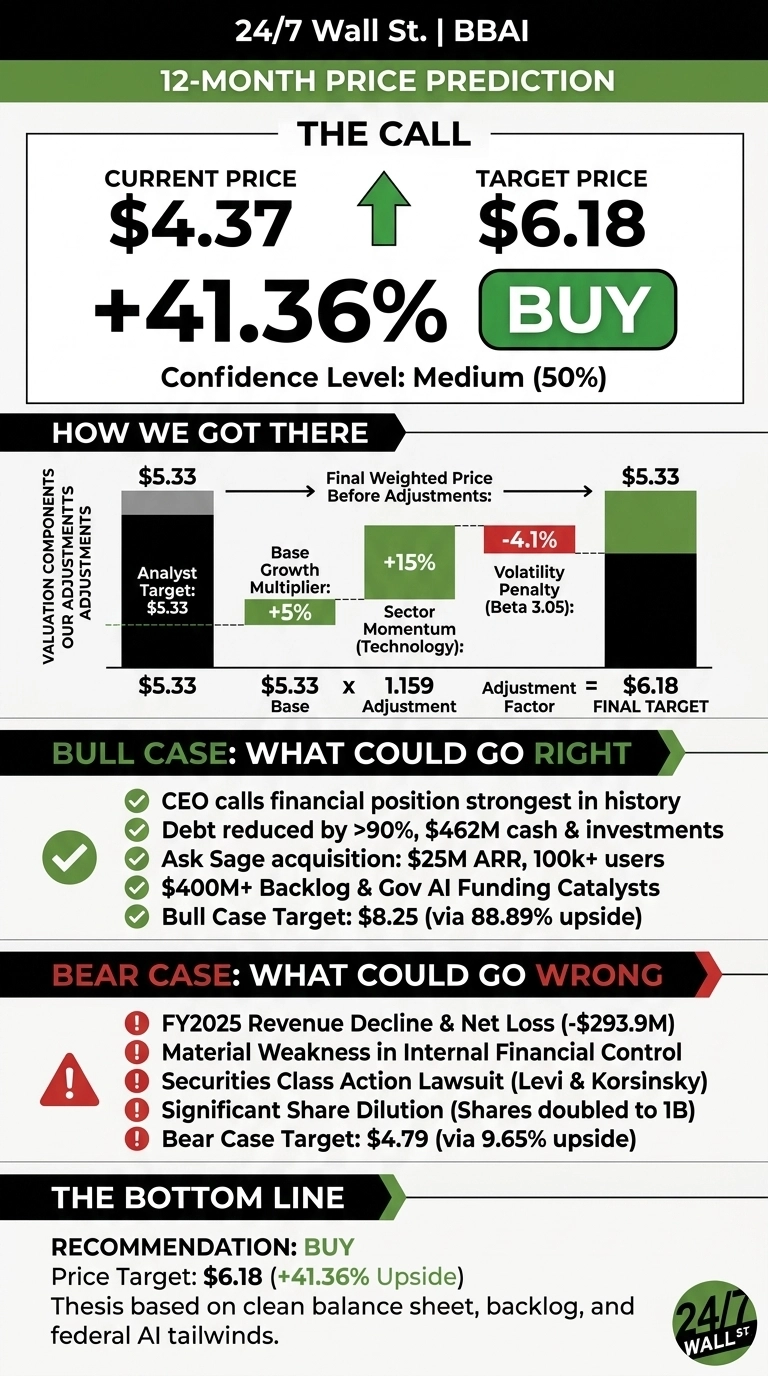

BigBear.ai (NYSE:BBAI | BBAI Price Prediction) is a high-volatility AI defense play that delivered a constructive Q1 2026. The stock has fallen from $9.39 52-week high to $4.37, but the recent 14.4% one-week bounce suggests the worst of post-earnings repricing may be behind us. Our 24/7 Wall St. price target is $6.18 over 12 months, implying meaningful upside. Confidence is medium, reflecting data gaps in analyst coverage.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $4.37 |

| 24/7 Wall St. Price Target | $6.18 |

| Upside | 41.36% |

| Recommendation | BUY |

| Confidence Level | 50% |

A Volatile Year With a Q1 2026 Inflection

BBAI is up 24.5% over the past month and 41.42% over the past year, but still down 19.07% year to date.

The Q1 2026 earnings report on May 5 delivered $34.4 million in revenue with an EPS of -$0.12, missing the -$0.08 consensus. Gross margin expanded to 34% from 21.3% in the prior quarter, and backlog rose 14% to $281.9 million. Management affirmed full-year 2026 revenue guidance of $135 million to $165 million.

Catalysts include a $53 million U.S. intelligence contract, more than $60 million in national security awards, and exposure to a potential $900 million U.S. Air Force contract vehicle.

The Case for $8 and Beyond

Bulls have a credible roadmap. CEO Kevin McAleenan called BigBear.ai the “strongest financial position in the company’s history” after debt was cut by more than 90% and $693 million was raised through ATM facilities.

The $250 million Ask Sage acquisition brings $25 million in ARR and 100,000+ users on 16,000 government teams, while CargoSeer extends the trade and travel franchise. Add the $170 billion DHS supplemental and $150 billion DoD disruptive defense allocation from the One Big Beautiful Bill, and a re-rating becomes plausible. Our bull-case path tracks to $8.25 within 12 months, an 88.89% return. H.C. Wainwright maintains a Buy rating despite trimming its target.

What Could Go Wrong

The bear case is real. FY2025 revenue fell to $127.67 million with a -$0.82 EPS, and Q4 2025 revenue dropped 38% year over year. There is a material weakness in internal control over financial reporting, an active Levi & Korsinsky securities class action, and shareholders just doubled authorized shares from 500 million to 1 billion, opening the door to further dilution. Insider activity has skewed toward selling. Our bear case lands at $4.79 over 12 months.

Bulls argue the FY2025 net loss of -$293.91 million is heavily distorted by non-cash items, including a $70.64 million goodwill impairment and $53.4 million long-lived asset impairment, while operating fundamentals improve alongside Q1 2026 margin expansion.

The Setup From Here, With Position Size in Mind

Our price target is $6.18, our recommendation is buy, and confidence is medium at 50%. The combination of a clean balance sheet, a $400M+ backlog, and exposure to multi-hundred-billion-dollar federal AI tailwinds tips the scale. The thesis strengthens if Q2 confirms gross margin durability above 30% and backlog continues climbing. It weakens if dilution accelerates or another government program cancellation hits the top line.

Here is where our model projects BBAI could trade, assuming current growth trajectories and government spending tailwinds hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $4.66 |

| 2027 | $6.15 |

| 2028 | $8.12 |

| 2029 | $9.35 |

| 2030 | $10.85 |

These projections assume BigBear.ai continues integrating Ask Sage and CargoSeer while government AI budgets expand. Significant upside or downside could result from large contract awards, further dilution, or resolution of pending securities litigation.