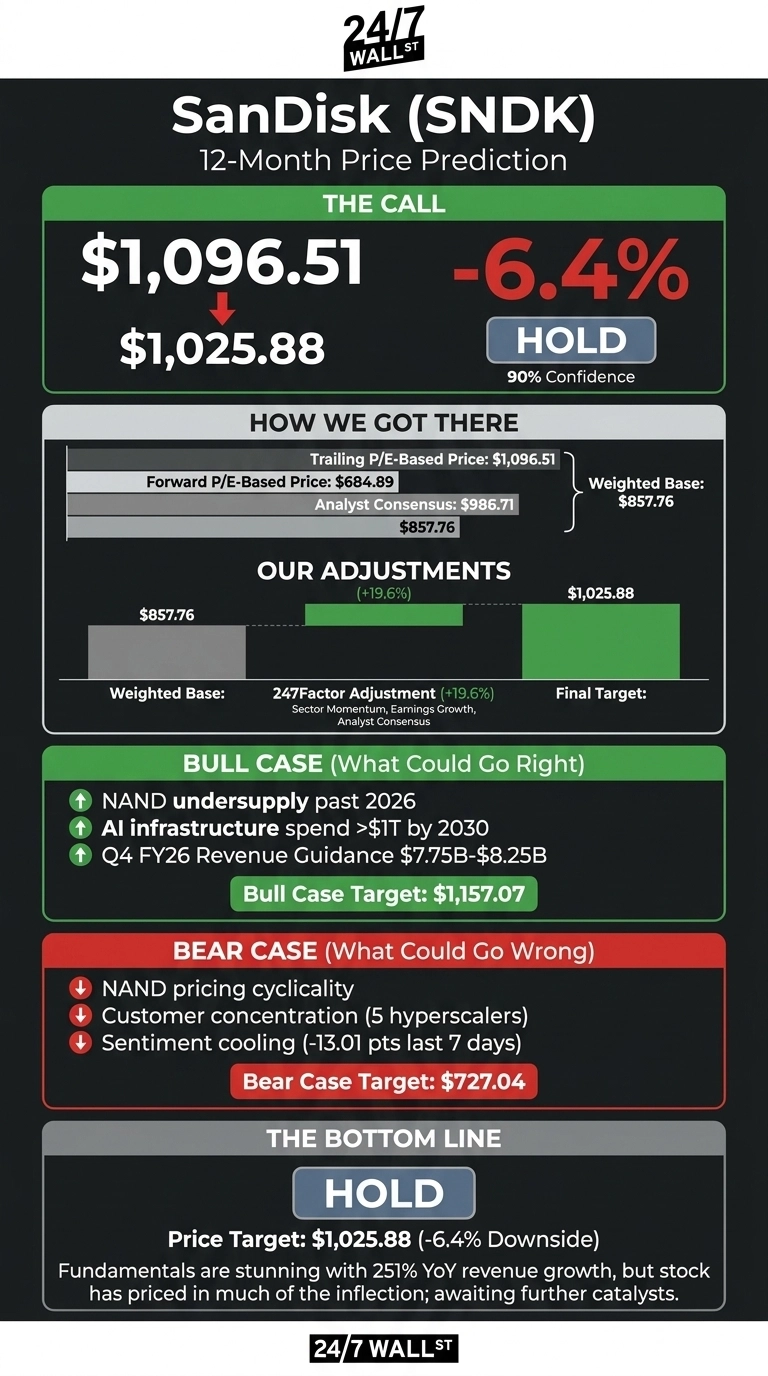

Few stocks have rewritten their narrative as quickly as SanDisk (NASDAQ:SNDK | SNDK Price Prediction). Shares have surged from $32.11 to $1,096.51 over the past year, a gain of 3,314.86%, on structural NAND pricing reset and datacenter mix shift.

Our 24/7 Wall St. price target for SanDisk is $1,025.88 over the next 12 months, slightly below current levels.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $1,096.51 |

| 24/7 Wall St. Price Target | $1,025.88 |

| Upside/Downside | -6.44% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Our price target sits roughly 6.4% below current levels, but this is one of tech’s most divisive momentum stories. Real upside could come from continued hyperscaler qualifications, faster High Bandwidth Flash ramp for AI inference, or NAND undersupply extending past 2026. Treat our number as one datapoint among many.

From $35 to $1,095 in Twelve Months

The recent run has been violent. SNDK is up 17.6% in the past week, 72.59% over the past month, and 361.92% year to date.

Q3 FY2026 revenue of $5.95 billion beat estimates by 25.68% and grew 251.03% year over year, while non-GAAP EPS of $23.41 crushed the $14.66 consensus. Datacenter revenue hit $1.467 billion, up 645% year over year. Gross margin expanded to 78.4% from 22.5%. Management retired $650 million of debt, reaching zero long-term debt, and authorized a buyback.

Why Bulls See $1,200 and Beyond

The bull case rests on three legs. First, supply remains tight: management has stated “demand for our NAND products continued to outpace our supply, a dynamic we expect to persist through the end of calendar year ’26 and beyond.”

Second, datacenter is becoming the largest NAND segment, with CEO David Goeckeler noting AI infrastructure spend “expected to surpass $1 trillion by 2030.”

Third, Q4 FY2026 guidance calls for revenue of $7.75 billion to $8.25 billion and non-GAAP EPS of $30.00 to $33.00. Fresh Buy ratings with targets above $1,200 have emerged, and our internal bull-case scenario points to $1,157.07 over 12 months.

The Risks Worth Watching

NAND is cyclical. The same pricing surge that drove gross margin from 22.5% to 78.4% in four quarters can reverse. SanDisk carries customer concentration risk through five hyperscaler engagements and structural dependency on the Kioxia Flash Ventures partnership.

Trailing P/E of -99 reflects the FY2025 goodwill impairment of $1.83 billion, though bulls correctly note that charge was non-cash and reflected post-separation accounting rather than a deterioration in operating performance. Sentiment has cooled, with the composite score down 13.01 points over the past seven days. Our bear-case scenario lands at $727.04, a 33.7% drawdown.

Hold for Now, but Stay Close

I rate SanDisk a hold with a $1,025.88 Price Target and 90% confidence. Fundamentals are stunning, but the stock has priced in much of the inflection. I’d be a buyer if NAND tightness extends meaningfully into 2027 or HBF lands a marquee AI inference design win. I’d step aside if Q4 FY2026 misses guidance or pricing visibility weakens.

Our price target model projects SanDisk could trade as follows, assuming current trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $1,025.88 |

| 2030 | $1,077.93 |

These projections assume SanDisk executes the BiCS8 ramp and converts hyperscaler engagements into multi-year NBM contracts. Significant upside or downside could result from the next NAND pricing cycle and High Bandwidth Flash commercial trajectory.