Retiring at a young age presents some unique challenges. Traditional retirement advice just doesn’t apply!

In a recent Reddit post I discovered, a 28-year-old entrepreneur shared their impressive income trajectory, aiming to hit $5M by age 35 and questioning the safest withdrawal rate for a 50-year retirement.

If you’ve been reading with us for a while, you probably know that the 4% rule is the classic recommendation for withdrawing during retirement (though the 4% retirement rule may be dead). But that’s for a 30-year retirement horizon, and it just doesn’t apply to young retirees.

In this article, I’ll look at how to calculate a safer withdrawal rate to ensure a comfortable retirement for those planning to retire early.

24/7 Wall St. Key Points:

- Aim for a 3% withdrawal rate if you plan to retire early.

- Factor in inflation when calculating your retirement needs and adjust your strategy over time to account for these market changes.

- Also: Take this quiz to see if you’re on track to retire (Sponsored)

Let’s jump right in:

Key Considerations for a Safe Withdrawal Rate

So, what makes a safe withdrawal rate? There are three main points to keep in mind:

1. Longevity and Time Horizon

Simply put, how long do you plan to retire? If you’re retiring early (like our Reddit poster), the rules of traditional retirement probably don’t apply to you!

With the potential of a 50-year retirement, I’d recommend a withdrawal rate of 3% or even less to ensure that the retirement funds last a lifetime. This more cautious approach allows for market fluctuations and rising living costs over the remaining decades of your life.

2. Inflation and Rising Expenses

As the Reddit poster noted, living expenses are very likely to increase with inflation over the next few decades (just like at what stuff cost 50 years ago!).

Therefore, I recommend adjusting your withdrawal strategy accordingly. Building in inflation adjustments is vital, even if you can’t predict exactly what things will cost in 50 years.

The fact is simple:

Things will cost more ten years from now, likely by quite a bit.

3. Flexibility and Rebalancing

No plan meets first contact, and a retirement plan is no different! The best retirement plan should involve some flexibility and regular rebalancing.

Monitor your spending and portfolio performance regularly, and be prepared to make small adjustments. Inflation may be higher (or lower) than you originally expected. You may need to temporarily cut back during tougher years to extend the longevity of your nest egg.

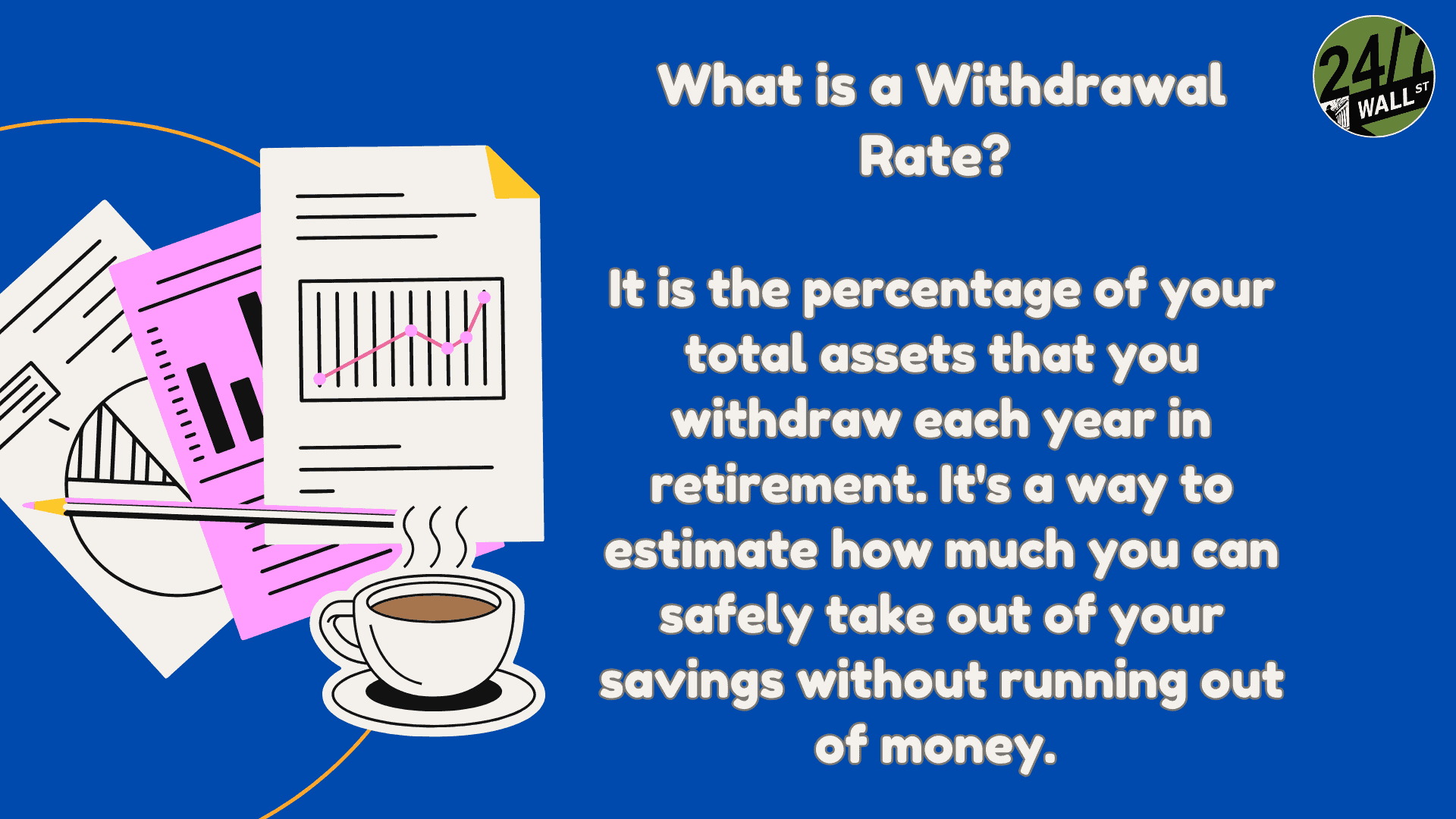

What is a Safe Withdrawal Rate When Retiring Young?

For anyone retiring young, especially at 35, the safest bet is to aim for a withdrawal rate of around 3%. This is lower than the usual recommendation of 4%, but it accounts for the longer inflation and market changes.

You should aim to remain flexible, though. You will need to periodically reassess your savings and retirement plan to ensure your money will last through your extended retirement.