The devastating inflation of the past four years has created a hand-to-mouth economic scenario for millions of Americans. The dearth of savings ability, due to escalated prices of essentials, has led to crushingly high credit card debt levels for many, with credit card debt overhang averaging over $20,000 per person. Retirement saving is a consideration that many believe they can now return to, with the prospects of a Trump economy boom resumption in 2025.

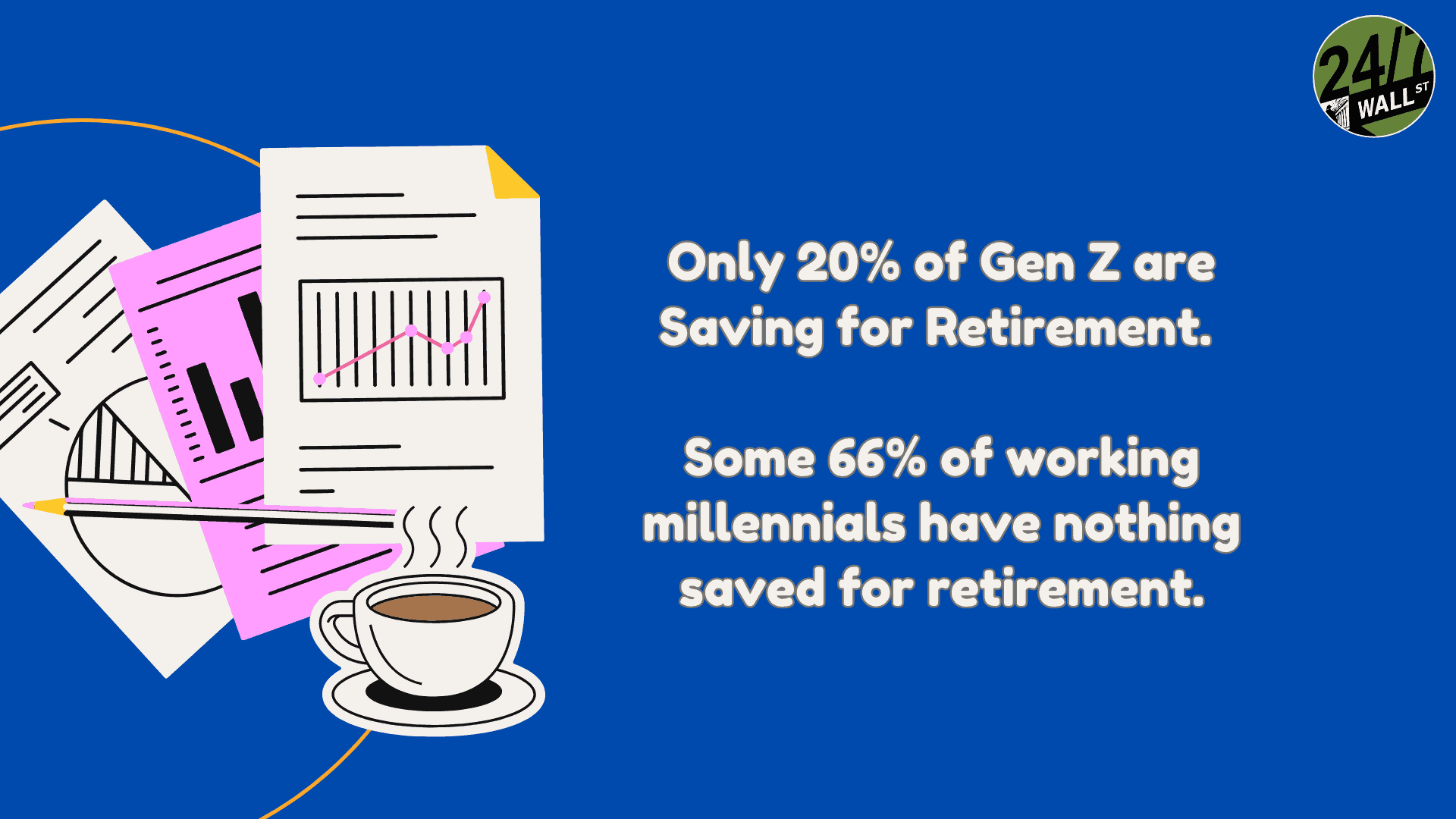

Gen-Zers who entered the workforce in the past ten years are the ones who may be behind the curve in retirement savings. Those who are a bit older may be close but have been forced to neglect retirement savings due to inflation. Additionally, assumptions on costs and lifestyle expenses made ten or more years ago may no longer be valid or adjusted for the escalated prices of goods and services from inflation.

A Benchmark Of Comparison

Due to inflation and inexperience, many Gen-Z aged people who entered the workforce voer the past decade are behind the curve in their retirement savings.

Retail broker Edward Jones handles thousands of individual accounts from all age brackets, so they are a reliable information source when it comes to optimal retirement savings levels. For millennials and Gen-Zers earning $100,000, Edward Jones has a benchmark reference for retirement savings level averages. Here is a sample of the list from ages 25-40:

| 25 | $0-$20,000 |

| 26 | $0-$35,000 |

| 27 | $0-$55,000 |

| 28 | $20,000-$70,000 |

| 29 | $35,000-$90,000 |

| 30 | $50,000-$105,000 |

| 31 | $65,000-$125,000 |

| 32 | $85,000-$145,000 |

| 33 | $100,000-$165,000 |

| 34 | $120,000-$185,000 |

| 35 | $140,000-$205,000 |

| 36 | $160,000-$225,000 |

| 37 | $180,000-$245,000 |

| 38 | $200,000-$270,000 |

| 39 | $220,000-$295,000 |

| 40 | $245,000-$315,000 |

For Those Who Are Behind The Curve

For those people who find that their retirement savings levels are below the average range and wish to achieve parity, there are several remedial measures that can be taken.

- Make a budget to get a clear picture of household and monthly expenditures and income to determine a target amount of savings per month in order to reach parity by a targeted age.

- Cut unnecessary spending – the daily $6.75 Starbucks latte is an extravagance if regular coffee will deliver the desired caffeine. Other items to cut will soon become apparent.

- Put the savings into a growth-oriented retirement account. Those using an employer-sponsored 401-K will have less options than those using a Roth or conventional IRA. Mutual funds or market index funds are the general growth choices, but some indexes, like technology, may have more upside potential in a shorter time span. The faster growth will maximize savings to more quickly reach parity levels.

For Those Who Are Ahead Of The Curve

People whose retirement savings are ahead of the curve will find that taking the steps to maximize growth early on can put them into F.I.R.E. mode for potential early retirement.

For those people who find that they are ahead of the curve, bravo! There are still steps that can be taken to build on that advantage and possibly assume a F.I.R.E. (Financial Independence Retire Early) strategy, which will afford a range of career and retirement choice options in the future. Those steps would include:

- Diversifying the portfolio to include exposure to international markets and commodities. Geopolitical events, both current and future, will create growth opportunities that may be unavailable in the USA.

- If the retirement plan has the option, choose to reinvest any dividends, rather than let the cash accumulate passively at anemic money market rates.

- Some IRAs allow for precious metals investment. The purchase of physical gold and silver, both of which have recently seen a steep upside trend, should be investigated. Gold is a reliable inflation hedge, and recent news from BRICS indicates possible asset-backed non-dollar currency for international trade based on gold, silver and oil. Additionally, silver is a depleting asset, since it is utilized for smartphone, LED screen, and battery manufacturing.

This opinion article should be viewed solely for informational value. If customized financial advice is sought, consulting with a financial professional should be conducted.