Retiring early and living a comfortable life is a goal for many. Sometimes, we think we are so far behind we will never catch up. But by adjusting our view just a little, we may be pleasantly surprised at how close we are.

That was my immediate reaction to a Redditor’s post on the r/ChubbyFIRE subreddit, a board devoted to retiring early but maintaining an upscale standard of living. He is a 42-year old Army veteran who was injured while on active duty.

He receives a modest pension of $1,500 as well as disability benefits of $4,800, or $6,300 per month total. The Redditor just got a civilian job and will qualify for a second pension when he turns 60 years old. While he has a four-year old daughter, he has just $150,000 saved for retirement. He has read he needs around $5.5 million saved and wants to know how he can reach his goal.

While it looks like he is too far behind to catch up, in reality he is far closer than he realizes.

24/7 Wall St. Key Points:

- Having realistic retirement goals is important, but also look at your entire financial picture.

- If you are one of just 11% of workers today who receive a pension, that is an important income source that can help take you across the finish line.

- Be proactive by having a backup plan ready to act on to improve your situation.

- Also: Take this quiz to see if you’re on track to retire (Sponsored)

The Redditor is actually in good shape. First, few workers today get pensions. Many employers ditched defined benefit plans in favor of defined contribution plans like 401(k)s. According to the Pension Rights Center, only 11% of private-sector workers are covered by a pension plan today. The Bureau of Labor Statistics says 87% of employees at medium and large establishments had pensions in 1979. The landscape has dramatically shifted since then and yet the Redditor will have two pensions upon retirement.

A rich source of reliable income

Pensions are income that last a lifetime. Similarly, the disability benefits he receives will also continue in perpetuity and have the additional benefit of being non-taxable. So the Redditor will have a minimum of $76,400 in income a year just from his military service.

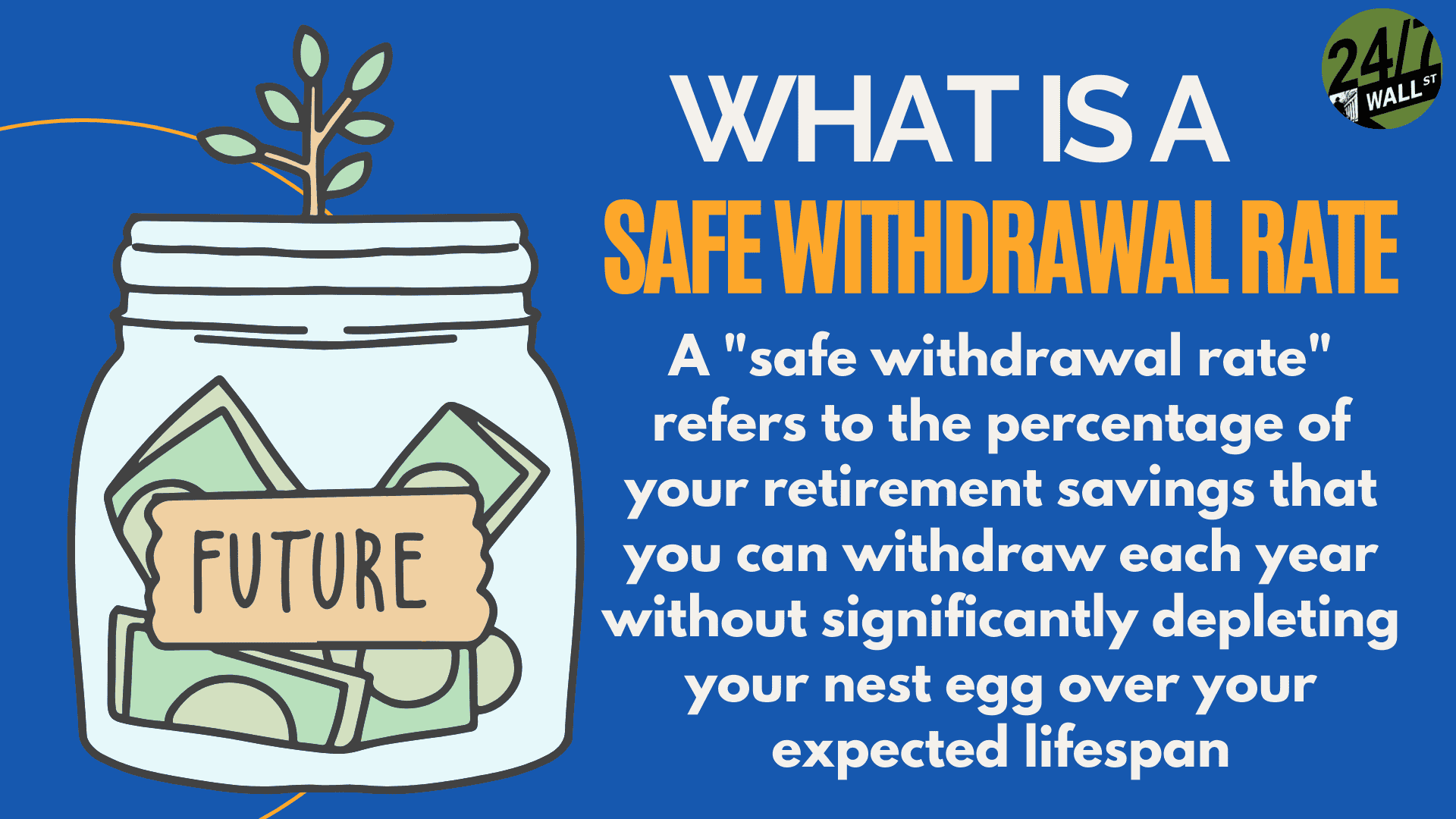

Assuming a safe withdrawal rate (SWR) of 3.5% from his proposed $5.5 million savings goal, he is expecting on spending $150,000 a year. His pension income gets him halfway there so he will only need to make up a difference of $73,600. But because he will received a second pension and also Social Security benefits, he likely already achieved his goal.

A workable plan for early retirement

While I’m not a financial planner, and these are just my opinions, a good plan of attack from here would be to invest in the stock market.

Buying an S&P 500 fund such as the Vanguard S&P 500 ETF (NYSEARCA:VOO | VOO Price Prediction), SPDR S&P 500 ETF Trust (NYSEARCA:SPY), or similar vehicle, would allow him to earn the popular index’s long-term historical average of 10% annually.

Obviously, past performance is no guarantee of future results and year-to-year results will vary, but over nearly seven decades, the S&P 500 has an incredibly consistent track record. If the Redditor makes regular monthly contributions over the next two decades, the power of time and compound interest will catapult him beyond his goal.

Starting with the Redditor’s existing savings, if he makes just $500 in monthly contributions earning 7% annually (to account for inflation), the Redditor would have nearly $750,000 saved at age 60. Using the SWR from earlier, that would equate to an additional $26,000 in annual income.

That means he should also try to put money aside for an emergency fund and carefully track his expenses so that he is living below his means. He might also consider putting aside some money for his daughter’s college education. A 529 college savings plan would be a good idea, and she could seek out grants and scholarships. She could also go to a community college or pursue a trade or apprenticeship.

Key takeaway

It is important to look at your entire financial picture to assess your situation. Seeking out the assistance of a financial planner and tax professional can help you determine the best course of action for your particular needs.

Yet just by shifting your focus only a little, you may quickly realize that as difficult a spot as it might seem that you are in, things could be much better than you think.