When the 401(k) was introduced in 1978, it was meant to supplement traditional pensions — not replace them. Back then, more than half of American workers could count on a pension. But as pensions disappeared, the 401(k) quietly became the cornerstone of retirement savings. Today, over 70 million Americans rely on it, with about $7.4 trillion locked away in these accounts.

Fidelity data shows that more than half a million Americans have reached “401(k) millionaire” status. Still, the system has its limits. A 401(k) alone wasn’t designed to carry someone through decades of retirement — yet millions of people treat it as their only plan.

That’s exactly what one Redditor recently discovered when his father retired after a long career in IT. Despite being financially savvy, his dad had saved only through a 401(k). Now, he’s realizing that even a healthy balance may not stretch as far as expected — and it’s sparked an online debate about whether most retirees are too dependent on a single savings vehicle.

24/7 Wall St. Key Points:

- The 401(k) retirement program has been one of the best developments in retirement planning, creating hundreds of thousands of 401(k) millionaires.

- The retirement program, though, isn’t your only option and not necessarily your best one, making talking with a financial planner an essential part of your planning process.

- With numerous investment vehicles available, make sure you are taking advantage of the best aspects of each to lay the groundwork for a comfortable retirement.

- Also: Take this quiz to see if you’re on track to retire (Sponsored)

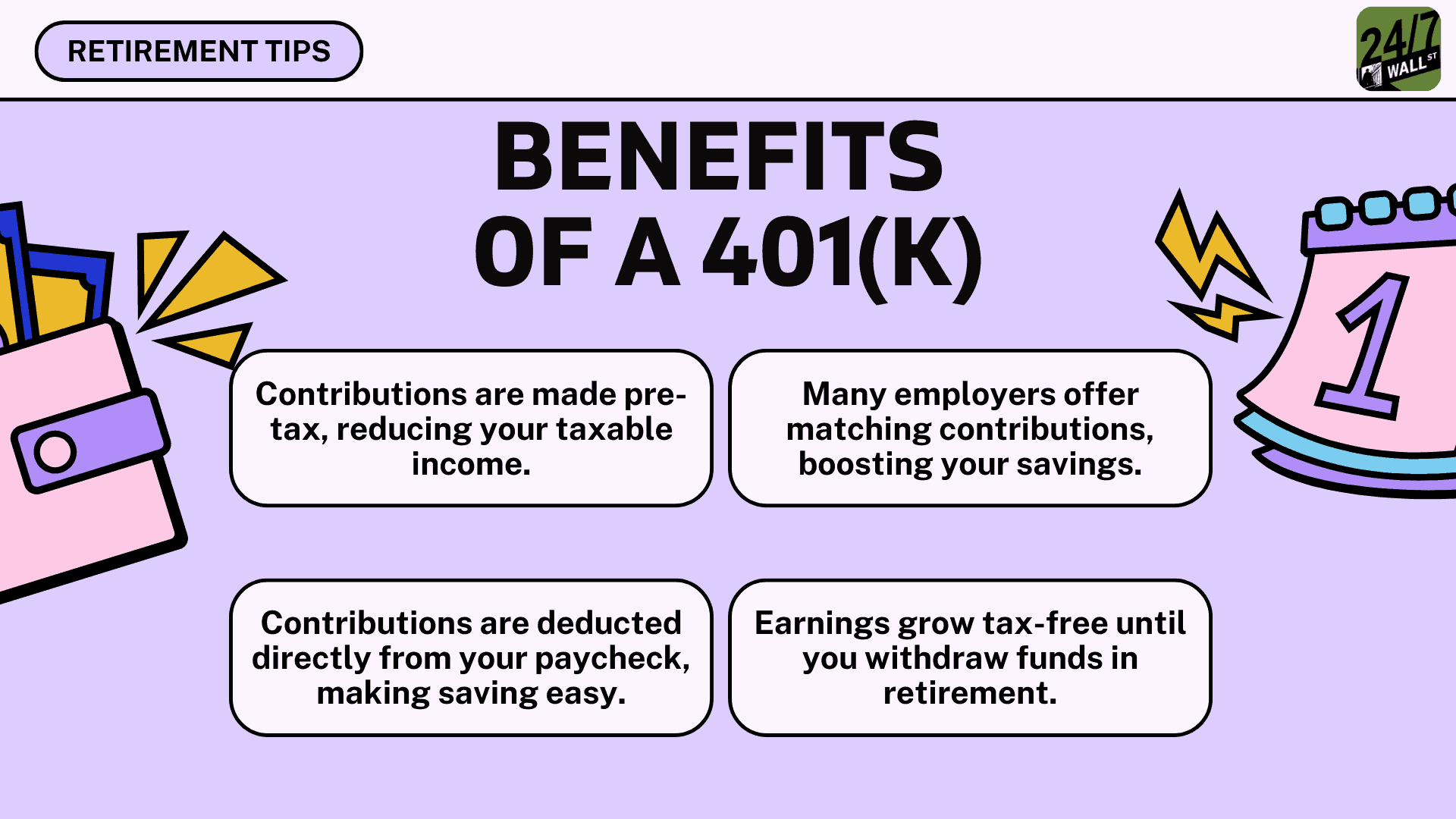

401(k) plans are awesome to a point

The thing about retirement planning is that it is a lot more complex than simply putting money aside in a savings program. As good as a 401(k) plan is, it has its limits.

Because money put into the plan is done with pre-tax dollars, the earnings are taxed at the end when you begin withdrawing the money. If you have been extremely successful in your investments inside the program, or perhaps because you have been successful, the tax bite at withdrawal could be substantial, even if you are in a lower tax bracket.

Now I’m not a financial planner or a tax professional, so these are just my opinions, but I understand why professionals often recommend only putting enough money into a 401(k) up to the employer match, if your employer offers one.

The employer match is where for every dollar a worker contributes the employer will match it dollar-for-dollar, or a percentage of it, up to a specified percentage of your income. Workers should take full advantage of that free money to supercharge their retirement savings.

Yet once you hit that threshold, it’s often advised you then begin contributing to a Roth IRA or HSA (or both). Only after maxing out those limits should you then contribute more to your 401(k).

Key takeaways

Because a Roth IRA is funded with after-tax contributions, the earnings inside the account grow tax-free upon withdrawal. The maximum you can contribute to a Roth is $7,000 if you’re under 50 and $8,000 for those 50 or older.

But you might want to fund an HSA first up to the maximum $4,150 (or $5,150 for those 55 or older) because these accounts are triple tax-advantaged. Contributions are pre-tax, so they lower your income, earnings grow tax-free, and withdrawals for eligible healthcare expenses are also tax-free. Since healthcare costs are likely to be one of your largest expenses in retirement, it is smart to take advantage of this savings plan.

But only after maxing out these alternative investment vehicles should you then go back and start contributing more to your 401(k).

Now there are other strategies to use, such as a backdoor or mega backdoor Roth IRA, that could help you do more. It’s why talking with a financial planner and tax professional is an important consideration. They can advise you on the best strategy to use that fits your particular situation.