When it comes to retirement, there are some longstanding rules of thumb many people rely on. Unfortunately, finance expert Suze Orman has a warning about one of those rules. Orman has urged people to stop following the 4% rule, saying “I would not be using the 4% figure on any level.”

So, what is the 4% rule, why is Orman urging you to abandon it, and should you listen to her and stop using it as a crutch? Here’s what you need to know.

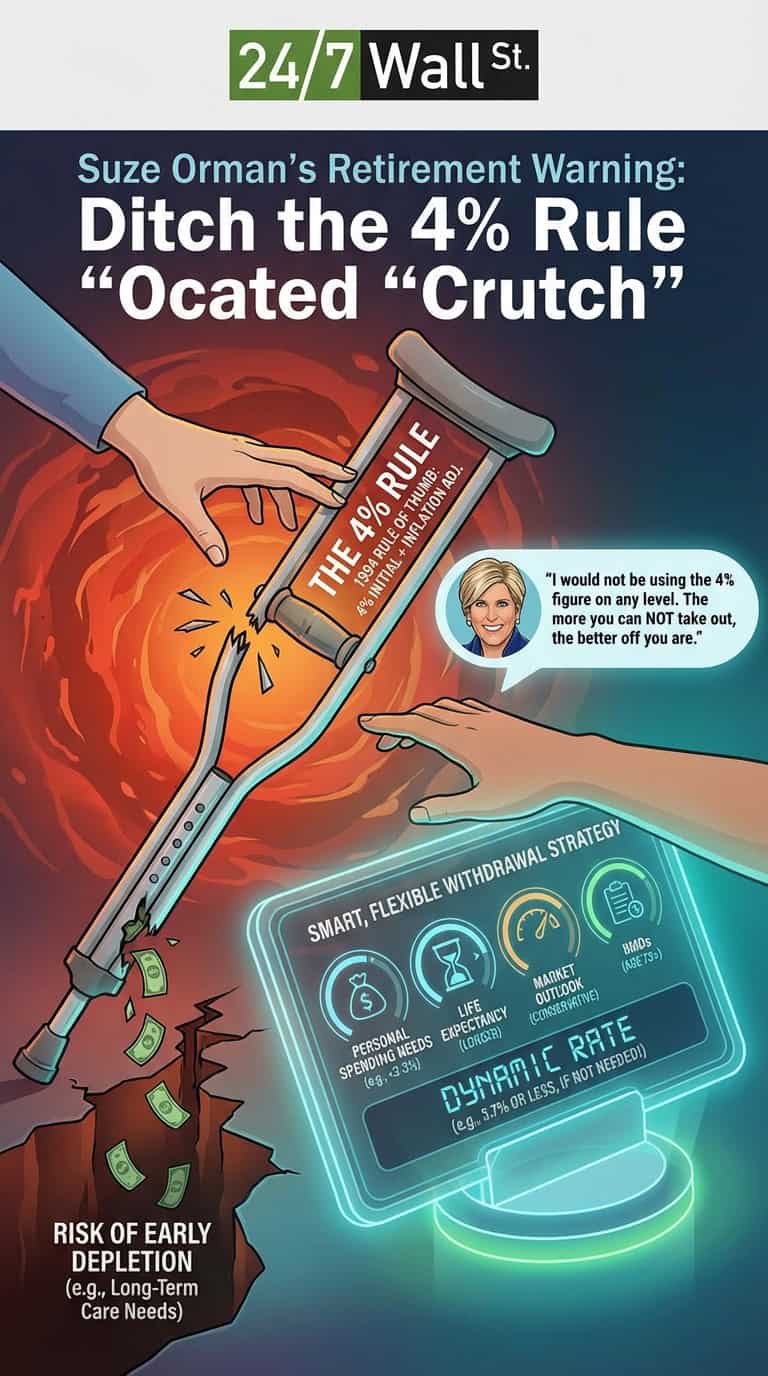

What is the 4% rule?

The 4% rule is a simple rule designed to help people choose a safe withdrawal rate for their retirement funds. According to the rule, if you take 4% out of your retirement accounts when you first retire and then adjust that amount each year to account for inflation, your money should last at least 30 years. So, if you had a $1 million nest egg, you would take $40,000 out of your retirement plan in year one of retirement.

The rule was developed in 1994 by a financial advisor named William Bergen to help simplify the process of deciding how much money you could withdraw without risking draining your account too fast and going broke.

What’s Orman’s problem with the 4% rule?

Orman does not believe you should follow the 4% rule because she believes that this rule sets you up to take money out of an account when you may not need it, leaving you at risk if you do need it in the future.

“Maybe you were taking out 4% and 4% even though you didn’t need it,” she said. Then one day, you may need long-term care that’s very expensive but you won’t have enough in your retirement accounts to afford it because you took withdrawals out earlier just to follow the 4% rule, even if your spending needs were lower.

“The more you can not take out of a retirement account, the better off you are,” Orman said.

Is Orman right?

Orman is right that you should not simply follow the 4% rule, especially if you don’t need the money. If you can live comfortably on 2% or 3% of your retirement nest egg, withdrawing more just because of a default rule would be a shortsighted choice as preserving your savings is usually better than spending.

There are also other problems with the 4% rule, beyond Orman’s fear that it could lead you to larger withdrawals than necessary. The biggest issue is that with lengthening life spans and more pessimistic future return projections, experts now believe that you should limit withdrawals to 3.7% — not 4%. Adopting this more conservative approach would likely be the right choice for most retirees as the consequences of running short of money later in retirement are too grave to take the risk of using up your money too fast.

The reality is that there are a lot of factors that determine how much you should withdraw including the total size of your portfolio, your risk tolerance, your life expectancy, and whether you are subject to Required Minimum Distributions which mandate that you take a certain percentage out of tax-advantaged retirement plans each year after turning 73. Following a basic rule of thumb that doesn’t take these specifics into account could leave you with regrets if you take out too much — or even if you take out too little and don’t enjoy life as a retiree because of it.

Working with a financial advisor to decide on the ideal withdrawal rate for you could be the smartest move you make, and you should seriously consider following Orman’s advice to forget the 4% rule and instead choose how much income your investments can produce for you based on your financial situation.