Many people work hard to build up savings for retirement. But retiring with a nice-sized nest egg is only half the battle. It’s equally important to make sure that money doesn’t run out on you. And so to that end, it’s essential to have a strategy for tapping your nest egg rather than simply withdraw funds randomly.

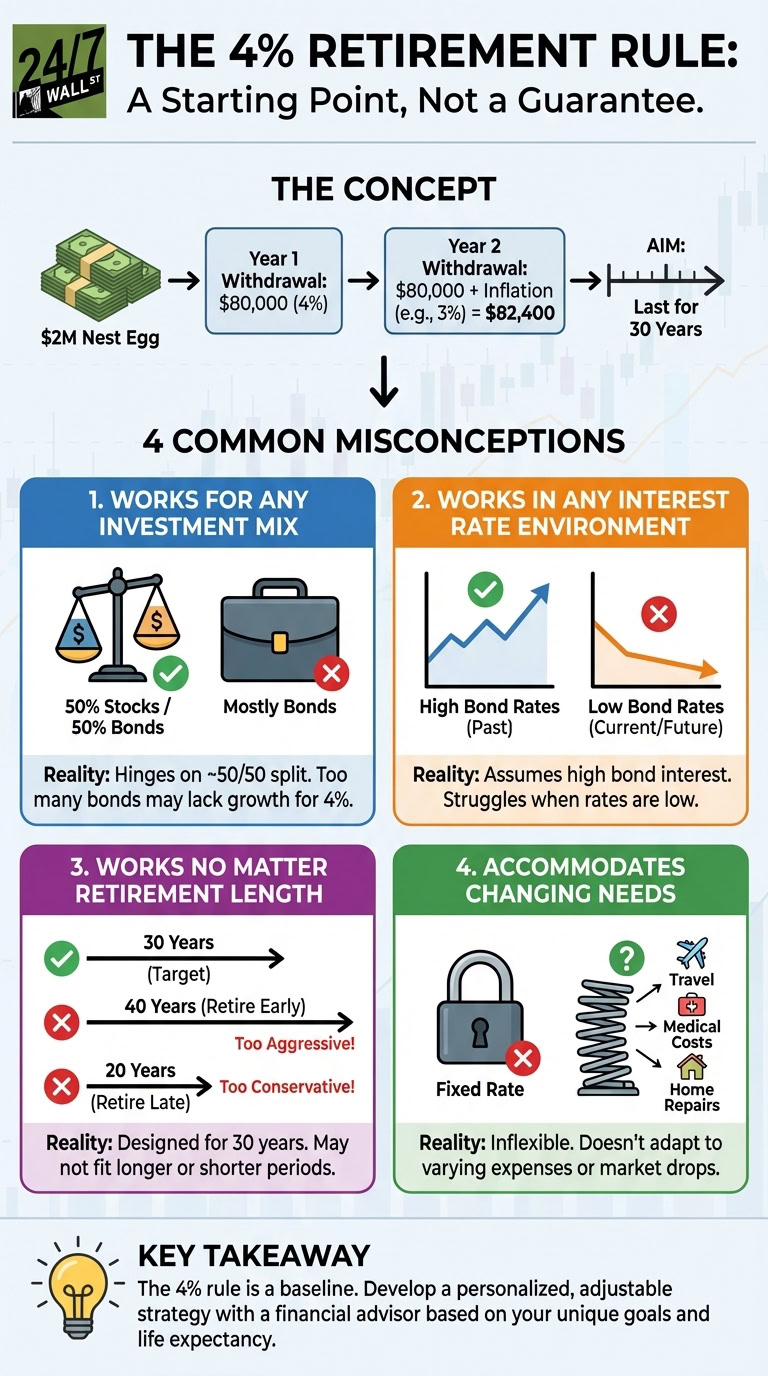

Since roughly the mid-1990s, financial experts have been fans of the 4% rule in the context of managing retirement savings. The 4% rule says that if you withdraw 4% of your savings balance your first year of retirement and adjust future withdrawals for inflation, your nest egg should last 30 years.

Here’s how it might work in theory. Let’s say John retires with $2 million. During his first year of retirement, he’d withdraw $80,000 from his savings. If inflation then rises 3% the following year, he’d withdraw $80,000 plus 3%, or $82,400. And so forth.

But while the 4% rule may work for some retirees, there’s a lot of misinformation about it. Here are four misconceptions about the 4% rule — and how they might impact your retirement finances.

1. It works for any investment mix

The 4% rule hinges on having a specific investment mix — a roughly 50/50 split between stocks and bonds. The thinking is that the bond portion of your portfolio won’t necessarily see a lot of growth but it should generate steady income, while the stock portion delivers gains and perhaps generates moderate income, depending on your specific investments.

Now to be fair, a 50/50 split between stocks and bonds is a reasonable asset mix for someone of retirement age. But that doesn’t mean everyone is invested in that manner. If your portfolio is mostly loaded with bonds, you may not see enough growth in it to support a 4% withdrawal rate during retirement.

2. It works in any interest rate environment

When the 4% rule was established, bond interest rates were high. But it’s not a given that bonds will be paying generously during your retirement, which is another big problem with the 4% rule.

In a lower interest rate environment, you may not get enough income out of the bond portion of your portfolio to support a 4% withdrawal rate. So you’ll need to assess how much interest bonds are paying at the time.

3. It works no matter how long your retirement is expected to be

The 4% rule is designed to make your savings last for 30 years. But depending on your retirement age, 30 years may not be enough time — or it may be too much time.

Say you decide to retire at age 55. If you’re in great health, you might live until 95. In that case, a 4% withdrawal rate suddenly becomes too aggressive, because you might need to stretch your savings for 40 years instead of 30.

And on the flipside, say you love what you do professionally and decide to keep working until you turn 75. You might, in that case, only need your savings to last 20 years, which would give you the flexibility to withdraw more than 4% of your balance each year in retirement.

4. It can accommodate changing financial needs

The 4% rule essentially locks you into a preset withdrawal rate throughout retirement, not accounting for inflation-related adjustments. But that won’t necessarily work for you.

You may have a year or two in retirement where your costs are higher — say, because your home needs repairs or you run into a series of medical issues. You might also want to withdraw from your savings at a higher rate during the early stage of retirement to do things like travel while your health is still good, and then scale back on spending later on. The 4% rule doesn’t really allow for any of this, and you might struggle with that lack of flexibility.

Know how to use the 4% rule

All told, the 4% rule is a great starting point for new retirees. And there’s an important lesson to be learned from it — to put thought into your withdrawals and have an actual plan.

However, the 4% rule isn’t guaranteed to make your savings last, and it’s also not suitable for everyone. So a better bet is to sit down with a financial advisor and come up with a strategy to manage your nest egg that’s based on your needs, goals, expenses, and life expectancy. It’s also important to revisit your withdrawal strategy periodically throughout retirement and make adjustments as necessary, such as to account for market fluctuations and changing needs and goals of yours.