A $2 million retirement portfolio sounds like financial freedom, yet many retirees with this nest egg experience persistent anxiety about running out of money. A recent Ramsey Show caller worried even $2.5 million wouldn’t suffice, while Reddit retirement forums regularly feature seven-figure savers questioning whether they can afford to stop working.

The disconnect stems from a harsh reality: the gap between what your portfolio can sustainably generate and what your lifestyle costs.

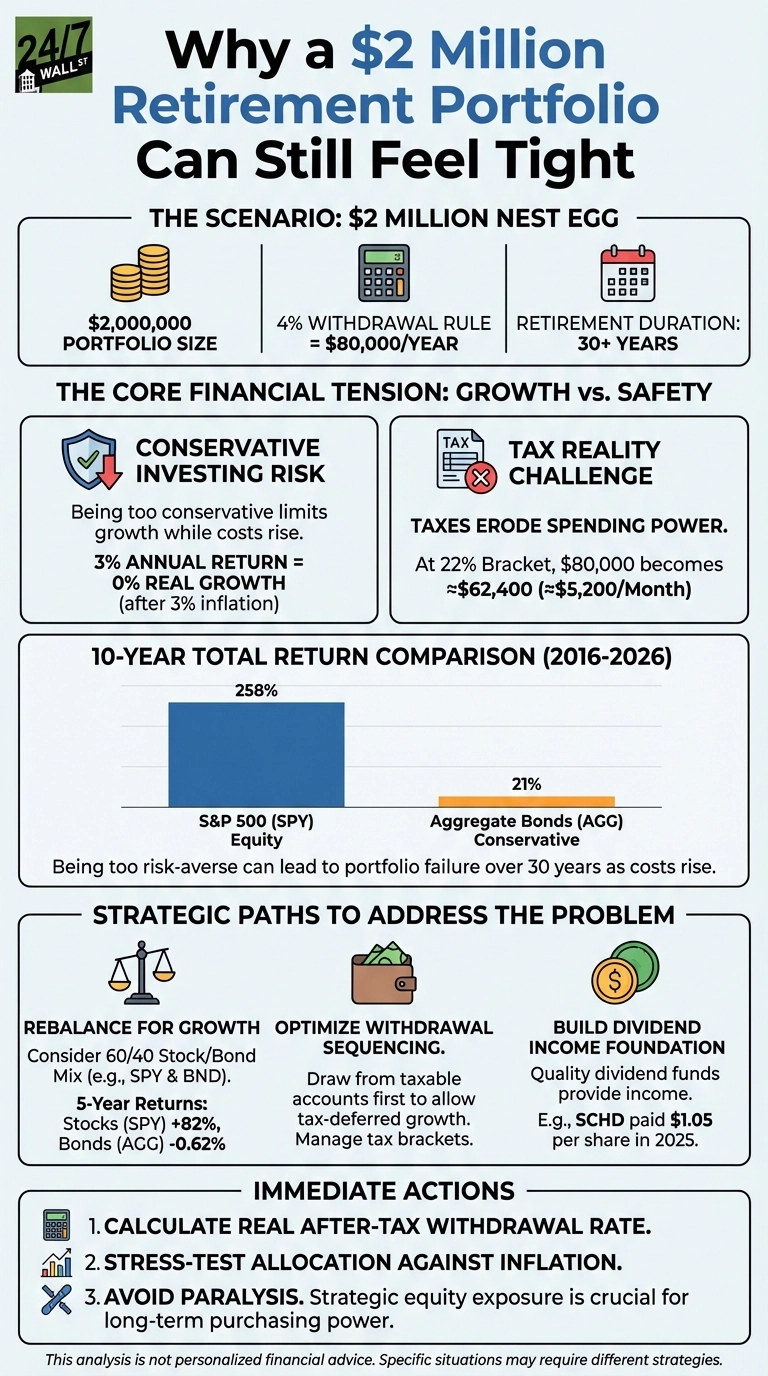

Key Scenario Elements

- Portfolio Size: $2 million in retirement savings

- Annual Need: $80,000 using the 4% withdrawal rule

- Primary Concern: Conservative investing limiting growth while costs rise

- Tax Reality: Withdrawals from traditional accounts face ordinary income tax

The Core Financial Tension: Growth vs. Safety

The 4% rule suggests $80,000 annual withdrawals, but taxes immediately erode this. At a 22% federal bracket, that becomes $62,400 after taxes, or $5,200 monthly. Add state taxes, and spending power shrinks further.

Conservative investing creates a hidden threat. Over the past decade, the S&P 500 (SPY) delivered 258% total returns—turning $2 million into over $7 million. Aggregate bond funds like AGG returned just 21%. A conservative portfolio earning 3% annually barely keeps pace with 3% inflation, producing zero real growth. Your $2 million stays $2 million nominally while losing purchasing power yearly.

This opportunity cost compounds dramatically. Being too conservative doesn’t just limit upside—it virtually guarantees your portfolio will fail to support rising expenses over 30 years. Healthcare costs typically increase faster than general inflation, while housing maintenance, insurance, and everyday goods continue climbing.

Strategic Paths That Address the Real Problem

Rebalance toward growth with guardrails. A 60/40 stock-bond allocation historically provides growth while managing volatility. Consider broad market exposure through SPY for equities and BND for bonds. This gives your portfolio a realistic chance to outpace inflation over decades. The past five years showed bonds (AGG) declining 0.62%, while stocks gained 82%.

Prioritize tax-efficient withdrawal sequencing. Draw from taxable accounts first, allowing tax-deferred accounts to compound longer. Save Roth assets for later years when required minimum distributions from traditional accounts push you into higher brackets. This sequencing can save tens of thousands in taxes.

Build a dividend income foundation. Quality dividend funds like SCHD paid $1.05 per share in 2025 across four quarterly distributions. On a $500,000 allocation, that generates roughly $19,000 annually in stable income, reducing the need to sell shares during downturns. Dividend growth provides a natural inflation hedge as companies increase payouts.

What to Do Right Now

Calculate your real withdrawal rate after taxes. Don’t assume the 4% rule gives you $80,000 to spend—factor in your actual tax situation. Many retirees discover they’re effectively living on 3% or less after taxes and healthcare costs.

Stress-test your allocation against inflation. If your portfolio earned 3% last year but inflation ran 3%, you made zero real progress. A portfolio that doesn’t grow faster than inflation will eventually fail.

Avoid the biggest mistake: paralysis. The fear driving excessive conservatism—losing money—ironically creates the outcome you’re trying to avoid. A $2 million portfolio that doesn’t grow becomes inadequate within 15 years of 3% inflation and 4% withdrawals. Strategic equity exposure, despite short-term volatility, is the only proven path to maintaining purchasing power across multi-decade retirement.

This analysis is intended to be helpful, but it is not personalized financial advice. Your specific situation may require different strategies based on your age, health, other income sources, and risk tolerance.