Social Security is a program that millions of older Americans rely on today. And without those monthly benefits, many would find it a struggle to cover their basic costs.

But Social Security is facing two major problems that lawmakers keep failing to address. Here’s what those problems are, and what potential solutions exist for them.

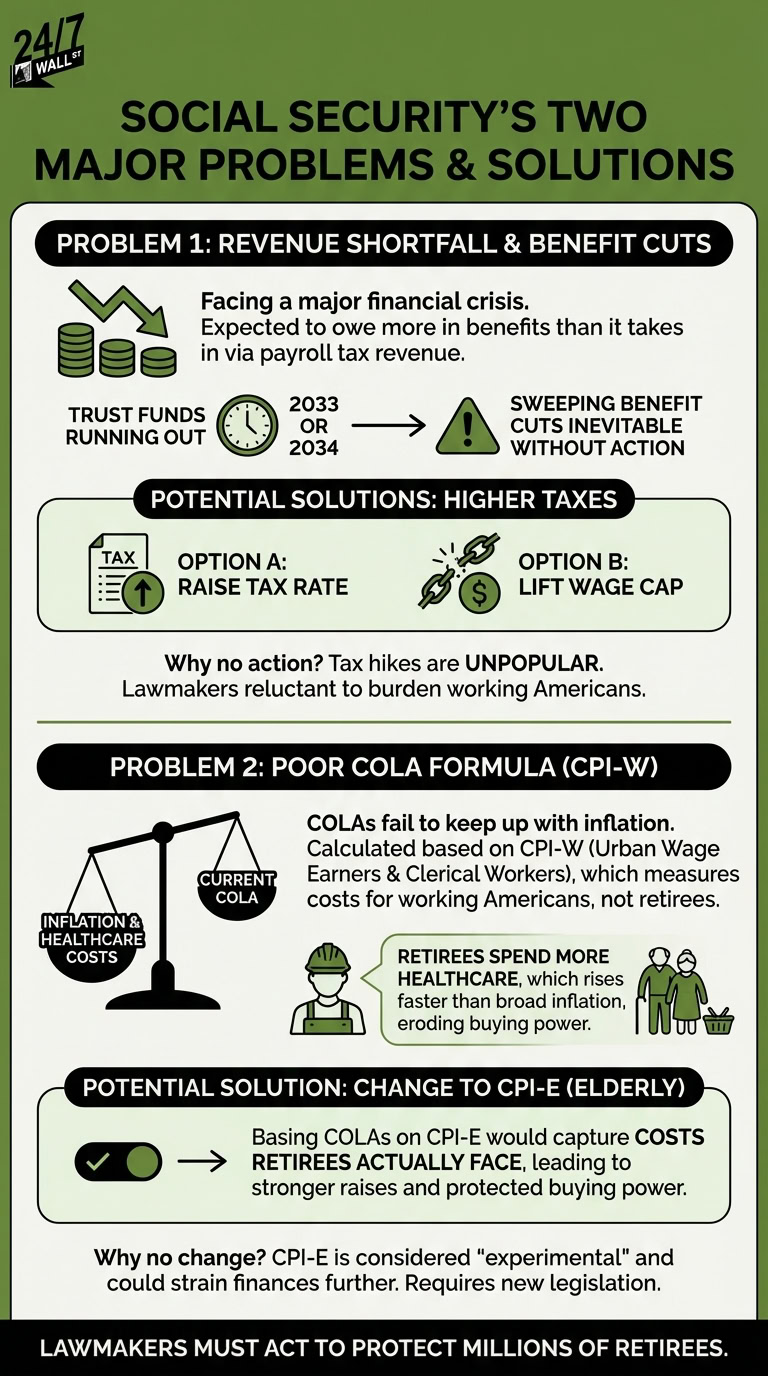

A revenue shortfall that could lead to broad benefit cuts

Social Security is facing a major financial crisis. In the coming years, the program is expected to owe more money in benefits than it takes in via payroll tax revenue.

The program can dip into its trust funds as needed to keep up with benefits for a limited period of time. Once those trust funds run out of money, benefit cuts may be inevitable.

Social Security’s Trustees reported earlier this year that benefit cuts could be on the table in either 2033 or 2034, depending on whether lawmakers agree to combine the program’s two trust funds. But either way, the writing is on the wall — Social Security needs a major revenue boost to avoid sweeping cuts.

There’s a solution lawmakers can implement — higher taxes. They could either raise the current Social Security tax rate, or they can lift the wage cap that limits the amount of earnings that are subject to Social Security taxes each year.

Why haven’t lawmakers taken action yet? It’s simple. Tax hikes are unpopular. Who wants to be the president who goes down in history for raising taxes and burdening working Americans in the process?

The problem, though, is that each year that ticks by brings Social Security one step closer to insolvency. Lawmakers need to think through tax changes and other potential solutions to prevent Social Security from slashing benefits broadly. If cuts aren’t prevented, millions of retirees could be plunged into poverty.

A poor COLA formula that leaves seniors scrambling to keep up

Social Security benefits are eligible for a cost-of-living adjustment, or COLA, every year. The purpose of COLAs is to help recipients maintain buying power as inflation pushes costs higher.

The problem is that Social Security COLAs have long failed to keep up with inflation in practice. That’s due to a disconnect in the way they’re calculated.

Social Security COLAs are based on changes to the Consumer Price Index for Urban Wage Earners and Clerical Workers, or CPI-W. But the CPI-W measures cost changes for working Americans, not retirees on Social Security.

Social Security recipients tend to spend a lot of their income on healthcare expenses. And in recent years, healthcare costs have risen at a faster pace than broad inflation, thereby causing COLAs to fall behind.

Lawmakers could change the COLA calculation formula to the Consumer Price Index for the Elderly, or CPI-E. Measuring COLAs based on an index that actually captures the costs retirees face could lead to stronger raises that give Social Security recipients more buying power from year to year.

So why hasn’t this change happened? It may be a matter of other priorities. Changing the COLA formula is unlikely to be met with the same level of backlash as raising taxes to boost Social Security’s revenue.

Still, a change like this requires all new legislation. And some lawmakers may feel that the CPI-E is a less reliable index that could ultimately strain Social Security’s finances at a time when the program is clearly desperate for money.

In fairness, the CPI-E is more of an experimental index, as opposed to the CPI-W, which is well established. But it’s clear that lawmakers need to do something to prevent seniors on Social Security from consistently losing buying power year after year.